Summary Of Jesse Livermore's "Upside Down Markets"

🙃

Summary Of Jesse Livermore's "Upside Down Markets"

👌

Introduction

Why I summarized this paper

Hi everyone

I read a lot of finance literature both as a hobby and professionally. In 2020, the best paper I read was Jesse_Livermore's Upside Down Markets. The paper is a beast. It's 40k words, heavily researched and footnoted. It's basically a book.

Many people won't read a 40k word paper. I encourage everyone to read this one. While it's a dense exploration of timely macroeconomics ideas, Jesse's rare ability to tackle the complexity in an approachable, step-by-step progression is an amazing opportunity to learn.

Having said that, I realize many people still won't read the paper. So I decided to try my hand at creating this explainer. I've refactored the paper a bit to fit this format and while it hits all the highlights there's no substitute for a firsthand reading of the paper.

With all that said let me start with Jesse Livermore himself. It's actually a pseudonym for my favorite financial writer. His site is philosophicaleconomics.com. The beauty of all his writing, not just this paper, is how he does not take ideas for granted. He builds them up from first principles. He gets into the weeds of accounting. Even if the subject of the paper doesn't stir you, his approach will teach you how economics works. This is especially impressive since Jesse is not an economist or even a finance guy (I don't know what his day job is but you are welcome to listen to his interview on Invest Like the Best and speculate yourself). I'm not the only one who's noticed how talented of researcher Jesse is. This particular post is a collaboration with O'Shaughnessy Asset Management (OSAM).

You are going to want to see how he breaks the economy down into understandable parts without actually dumbing it down.

Read the original paper here: Upside Down Markets(you can also read a version with my highlights here).

Ok, let's set the scene.

The context of the paper: covid and stimulus

Since the housing bust in 2008 and the ensuing financial crisis, policy makers have leaned heavily on monetary stimulus to support economic growth.

In 2020, Covid forced a shutdown of wide swaths of the economy. This hit large segments of the service sector including restaurants and travel esp hard. Given the urgency, a large stimulus bill known as CAREs was fast-tracked with broad political support. If the market and policymakers found this to be a success, we should expect fiscal stimulus to be easier to pass in the future.

Now remember, for more than a decade investors have become accustomed to monetary intervention. Investors are used to that regime. Switching to a fiscal playbook is a new world for markets.

So here you are, staring at the dashboard of an unfamiliar fiscal intervention spacecraft. This paper is a guide to the knobs and sliders on that ship.

Jesse starts with a tour of how the economy works. He explains how govt spending influences the rest of the economy. He explains the risks and constraints of this spending. Then he moves on to what you really want to know...how markets may respond in various scenarios.

What is an "upside-down market"?

An upside-down market is a market in which good news functions as bad news and bad news functions as good news.

How does this happen?

Policy. The market expects intervention that offsets the news and possibly more. You are already used to this in a monetary policy context. Bad news invites lower interest rates which ends up boosting asset prices. This effect however only goes so far and the impact on fundamentals is even weaker.

Fiscal policy, however, is a different animal. If leaned into hard enough it can achieve any level of nominal growth that it wants. It has the potential to create truly upside down markets.

To be clear, currently policy makers target a desired inflation rate. A new game-changing fiscal regime would require policy makers to target not inflation exactly but nominal growth. I'll repeat that. The sign that the game is truly changing is when policy makers start targeting specific levels of nominal GDP as opposed to inflation rates.

While they currently don't do this, Jesse suggests the tide might be turning. I quote:

People on both sides of the aisle are increasingly coming to realize that fiscal policy is the "cheat code" of economics. If you're willing to tolerate inflation risk, you can use it to achieve any nominal outcome that you want. As people become more aware of this fact, they're going to increasingly challenge traditional approaches, demanding that fiscal policy be used to safeguard expansions and eliminate downturns. Upside-down markets will then become the norm.

The $7.5 trillion Covid stimulus over 2 years (35% of GNP) is a step towards the recognition of this "cheat code".

As fiscal intervention becomes part of the standard playbook, you will want to understand how it can lead to upside-down markets in 3 specific areas:

Corporate Profits

Inflation

Equity Market Valuation

A basic understanding of the economy

3 segments of the economy

One of the first things you learn in macroeconomics is there are 3 segments of the domestic economy:

household

govt

corporate sectors.

Let's recall what can they do when they receive income.

Let's do this from a household's point of view. There are 2 things a household can do with income:

consume

save/invest which we will call saving. Saving and investing are the same. In macroeconomics we that "S=I".

(This makes sense. If you put your cash in a savings account you're technically investing. It's just that Citibank is lending out the funds you've deposited. Your savings are effectively being invested. The bank is an intermediary arbitraging a cheap source of funds from you to finance a borrower who is looking to build a business or maybe just buy a house.)

💡

Drilling downSavings

So we agree saving is investing. But we need to unpack that.

You can invest in primary or secondary markets. What's the distinction?

Secondary market investing is already familiar to you. It's buying real estate, stocks and bonds. It is an important function and can lower the cost of capital by raising the values of businesses that people are vouching support for. However, secondary market investing only re-shuffles risk between buyers and sellers.

Secondary market investing is the bulk of how we save via investing.

In contrast, primary investing is when we exchange cash for the creation of a brand new asset. For example construction by investing in building a house or factory from scratch. We can seed new companies or open a new restaurant. These primary investments require novel economic activity such as hiring people that are currently not employed. Quoting Jesse:

It means the creation of a new asset, something with lasting economic value. In funding the creation of that asset, they spend the income that they're seeking to save, transferring it to other entities in the economy. In this way, they're able to grow their accumulated wealth while also supporting the income and wealth of others.

Why do we care so much about the distinction between primary and secondary market investing?

Because primary investing is the only form of saving in which we are actually generating new non-zero sum spending.

Jesse writes:

To sustain the flow of income through the system, households need to save their income in a way that also entails spending that income —> primary investment

So to keep track of the distinction we re-brand saving.

When a household saves by investing in secondary markets that is now known as withholding.

We reserve the word investing to the idea of applying to savings to primary markets. Again, like building a business or house from scratch.

So we know households can consume and they can save. And we now understand that savings can be decomposed into withholding and investment.

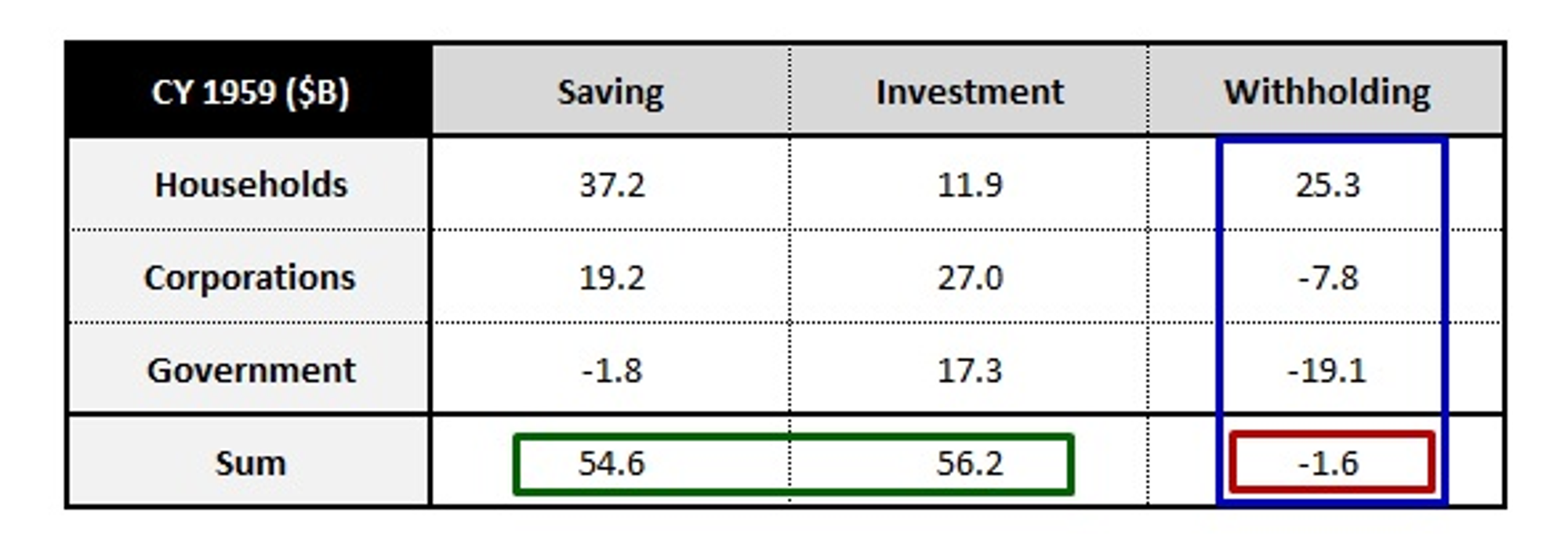

Here's a key point. Withholding is a zero-sum game. The total withholding across household, corporate and govt sectors sums to 0. In the US, households are net withholders while the govt and corps run deficits (ie they are net borrowers..they spend more than they save). This deficit spending is funded by the issuance of money and debt securities which in aggregate are held by the household sector as savings. Specifically the witholding type...secondary market liabilities of corporations and the govt.

Jesse shows data highlighting how it is quite typical historically and today that households are net withholders while govts and corps are net borrowers or deficit spenders.

This chart is from 1959 but it's still directionally correct in modern times.

(Btw, this idea alone is a good example of why thinking the govt can go bankrupt is incorrect. You can't think of a govt like a household. Some sector has to run a deficit for another sector to be a net saver or withholder. Withholding is zero-sum.)

So if you go back to macro econ 101 again where S=I we can see that investment does indeed increase wealth over time. It's just that it's primary investment that does this. If an economy's saving only took the form of withholding, it will run into a dead-end.

The flow of wealth and multiplication

Now we need to relate savings to how wealth flows thru the system

Let's define 2 terms.

Wealth Injection: Deficit spending on the part of a given entity injects financial wealth into the rest of the system.

Wealth Removal: Withholding on the part of a given entity removes financial wealth from the rest of the system.

Logically, whatever is injected by one entity has to be removed (i.e., received) by another.

What we care about is how and how much these flows multiply further injections or removals.

when a given entity injects financial wealth into the rest of the system through deficit spending, how much additional spending does the injection generate? You know these as Keynesian multiplers

The same question can be posed in reverse: when a given entity removes financial wealth from the rest of the system through withholding, how much existing spending will be destroyed before someone finally deficit-spends to make up the difference?

This last part is negative multiplication. Many will recognize that it sits at the core of the Paradox of Thrift. For an individual, saving is prudent, but in the aggregate, withholding leads to a death spiral.

We have now identified:

the segments of the economy (govt, household, corps)

the components of saving (investing vs withholding)

and flows (injections and removals)

...we can move on to the impact of “upside-down” markets on 3 variables starting with corporate profits

This paper is significant because it understands the regime change

Monetary policy, which was conducted in the name of expediency in the aftermath of the GFC, is now giving way to a greater comfortability with fiscal stimulus.

Fiscal has been traditionally harder to implement since it requires Congress and therefore bipartisan agreement in a system that is typically checked and balanced. An unintended consequence of our preference for expediency has been a strongly regressive economic policy for the past decade which has favored asset inflation.

Fiscal stimulus is more re-distributive and progressive. This changes the nature of its effect on profits, inflation, and valuation.

Covid may have removed the mental obstacles to increased deficit spending. This can mean new upside down effects that the past decade of reliance on monetary have not prepared us for.

Favorite aspects of the paper

Accounting identity framework via Kalecki-Levy. I should add that one of the brightest investor friends I have has embraced this approach and pointed to the supreme work of China-focused economist Michael Pettis.

Learning how spending power via fiscal policy differs from monetary policy and why monetary policy loses effectiveness as the credit channel becomes neutered (the real constraint is worthwhile projects to underwrite)

Historical contexts for stimulus esp WWII. The idea that credit expansion drove increases in spending power since the 1960s and growth in M2 was substituted for credit expansion since the GFC (in fact I wonder if these must counterbalance as the growth of M2 is tied to lower interest rates which make credit expansion too risky to undertake)

The discussion of inflation mechanics.

In particular:

How M2 and total credit (ie liabilities of the banking system) are the proper indicators of spending power not just M2

The focus on wealth velocity and the understanding of how wealth inequality causes an inflation heat sink by siphoning income back to the rich where it is not spent, short-circuiting multiplier effects. This dynamic suggest we need much larger injections of wealth to spur inflation since wealth velocity falls as wealth increases. It's an interesting idea that we might not be able to spur inflation without redistribution and even then, if most dollars flow back to the rich, it is possible that this top-heavy dynamic is a black hole. The danger in this realization is policy makers may relax fiscal discipline seeing the risk of inflation as perpetually small.

Asset inflation as the logical outcome of increasing wealth demanding to be withheld and recycled thru secondary markets rather than being spent and possibly creating inflation in goods and services.

Jesse's methodical treatment of complex topics and the ability to break things down and bring the reader around slowly without excessive hand-waving. It would be tedious if he wasn't such a careful and engaging writer.