This post will help you understand the Black-Scholes equation in a conceptual way. No calculus or mathematical derivations.

It assumes you are somewhat familiar with it as a model to price options.

Why did I Write This?

I watched a video that combined with my prior understanding of the model to yield a more satisfying grasp of the intuition than the one I used to carry with me. Maybe my current grasp will resonate with readers in ways that extend their own intuition.

Here’s the video that prompted the post:

📌

Conceptual Overview

Nobody takes the model seriously as way to compute the absolute value of an option. It is used more as a thermometer to measure what the market might be saying about implied volatility. In that sense, it’s useful for comparison.

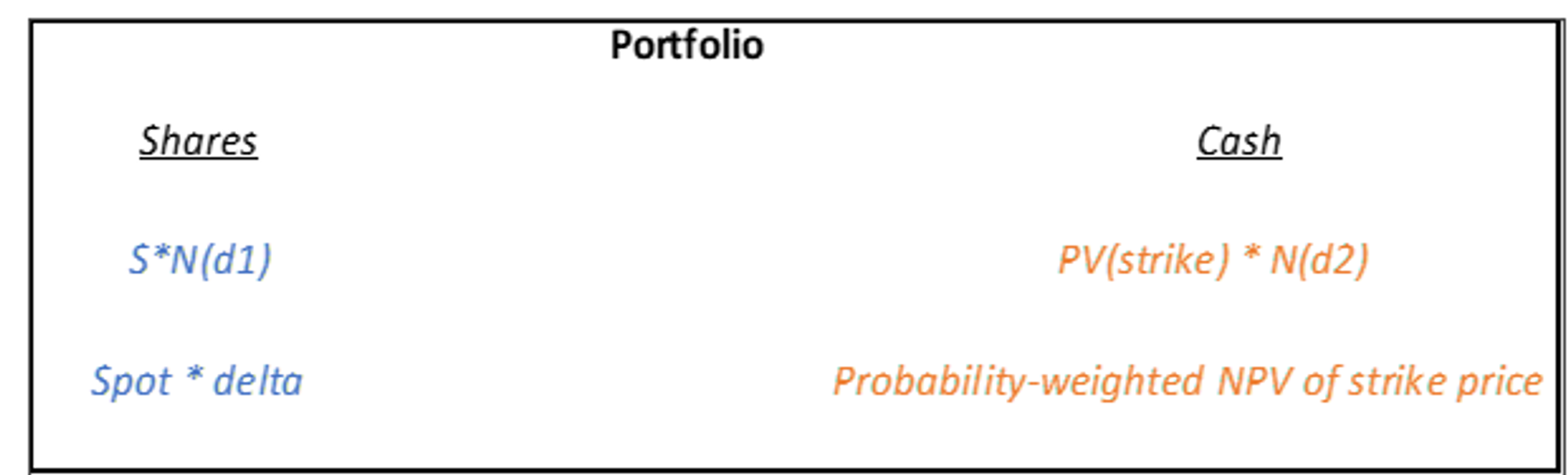

But the intuition is a great demonstration of the replication approach that characterizes arbitrage pricing techniques. The gist of the approach rests on a simple idea:

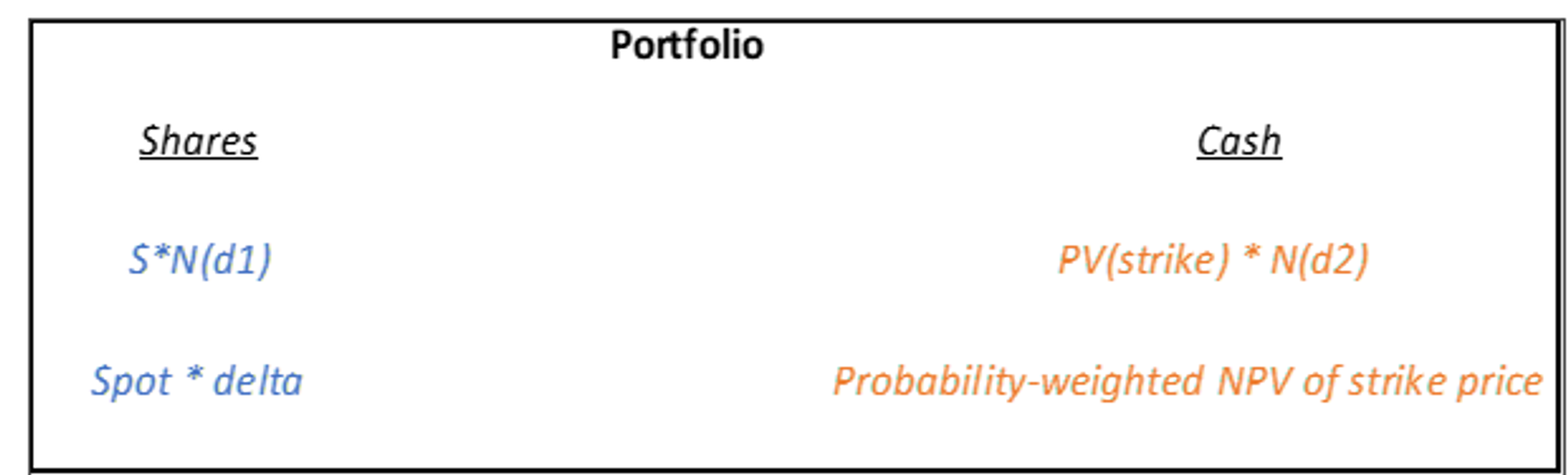

If you can replicate the cash flow of an asset with a strategy then the price of the asset should equal the cost of executing the strategy.

If the strategy and the asset have the same cash flows, then a portfolio that is short the asset and long the strategy has no risk.

If the asset trades for a higher price than the cost to execute the strategy, then:

short the asset and execute the strategy to capture the excess cash flow

This would be a riskless profit. Since the competition for riskless profits is ruthless we can infer that the price of asset would trade in line with replication costs.

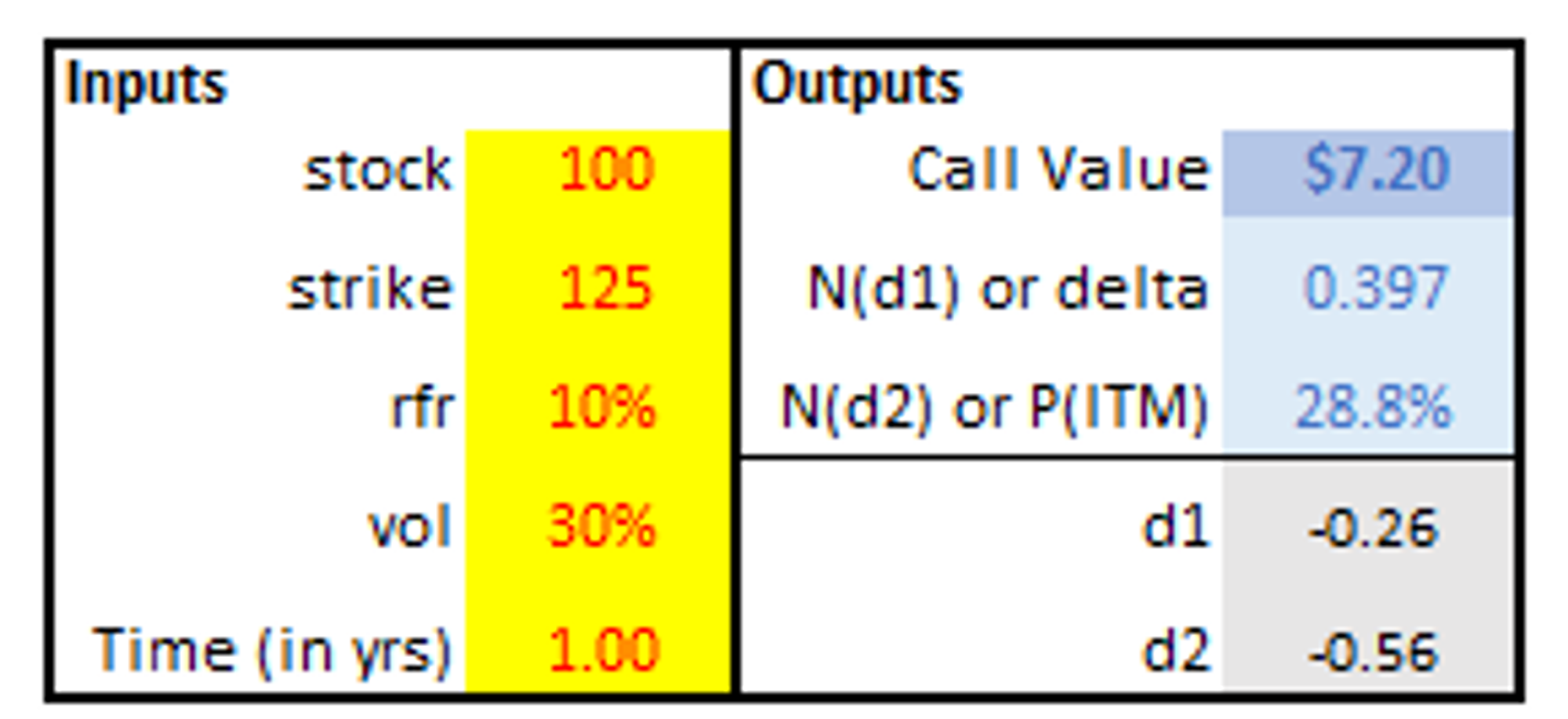

To bring this to life, let’s set up an example to refer to.

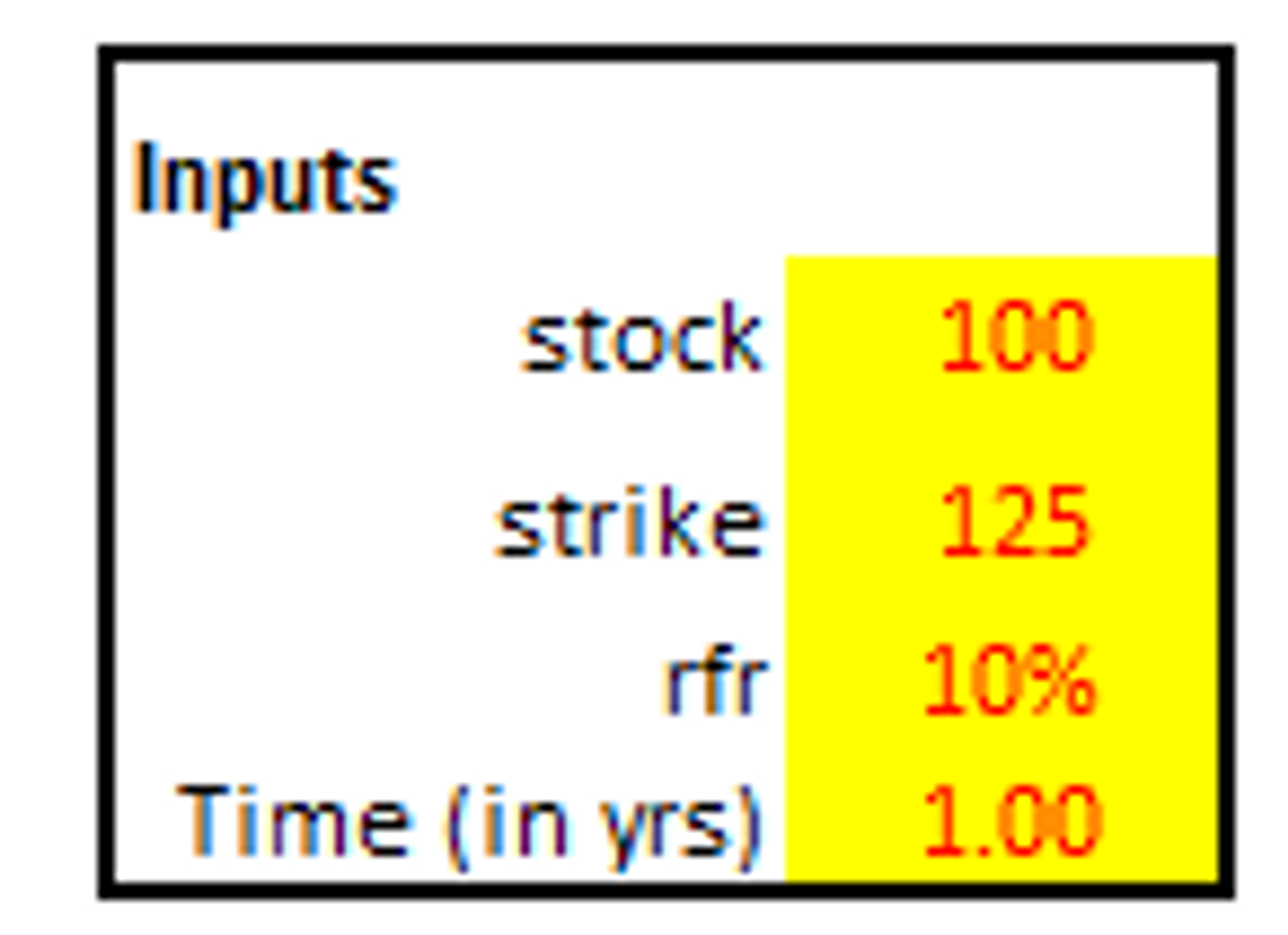

Pricing a European-style call option with the following terms:

1 year to maturity

Spot price = $100

Strike price = 125

Risk-free rate = 10%

Volatility = 30%

You can solve the formula with an online calculator, programming it into Excel or the language of your choice. Back in 2000, I programmed it into one of these:

Ok, here’s the output:

The call option is worth $7.20

It has about a .40 delta

It has about a 29% chance of expiring in-the-money

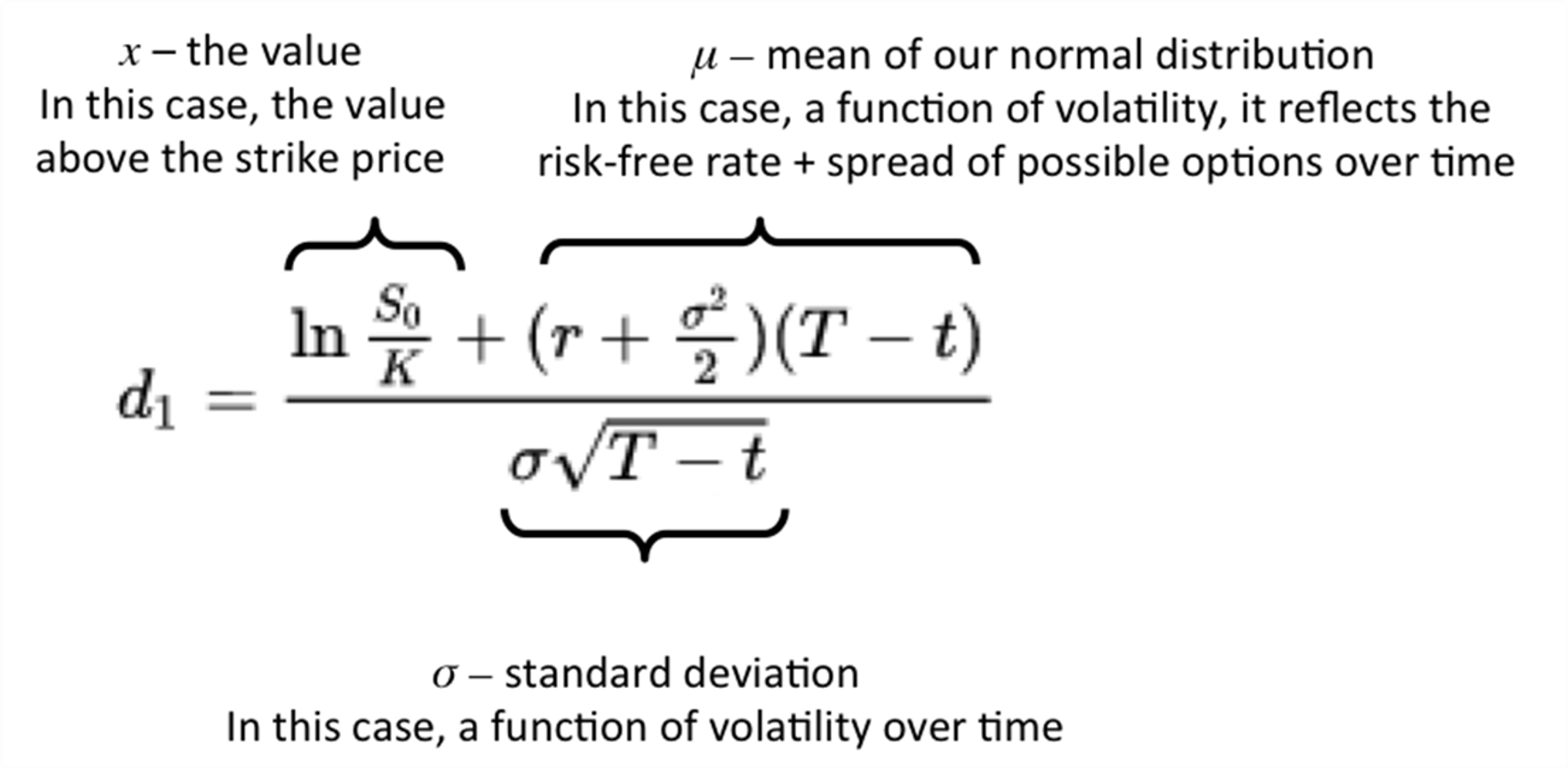

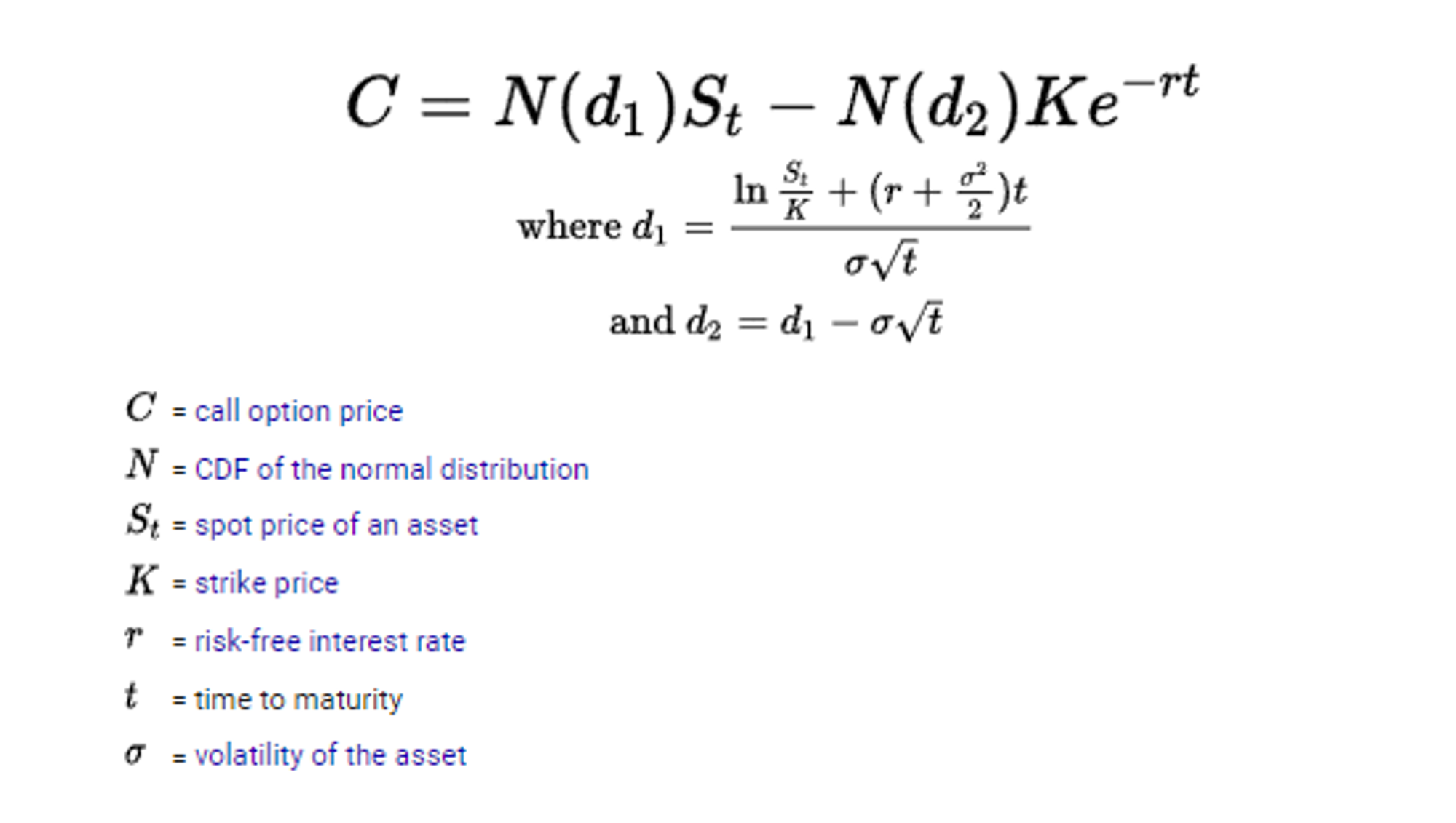

increases N(d1) otherwise known as the hedge ratio or delta.

This is because the “drift” or forward price is mechanically higher.

increases N(d2) which is a positive function of N(d1)

Simple intuition agrees. If you increase the forward price of the asset, then any fixed strike price is mechanically more in-the-money or less out-of-the-money.

However…

The value of the call option will increase overall as you raise the risk-free rate.

Why?

The higher the risk-free rate, the less proceeds you earn on the sale of the t-bill. It trades at a larger discount to face value.

The net effect:

The first term: S*N(d1) grows larger as N(d1) grows larger

The second term: PV(strike) * N(d2) does not grow as quickly because while N(d2) grows PV(strike) shrinks

Therefore the call option which is the number of shares you need minus the amount of shares you can actually afford to finance expands in value.

It costs more to finance the replicating portfolio!

This is why call options have a positive rho, the greek for sensitivity to interest rates.

Put options have a negative rho and increase in value as the risk-free rate falls.

The impact of volatility on delta and probability of expiring in-the-money

Let’s look at our option again. We’ll keep all the inputs the same except the volatility to see how it affects a few key parameters.

We’ll work from obvious to less obvious.

📌

Pinned for reference

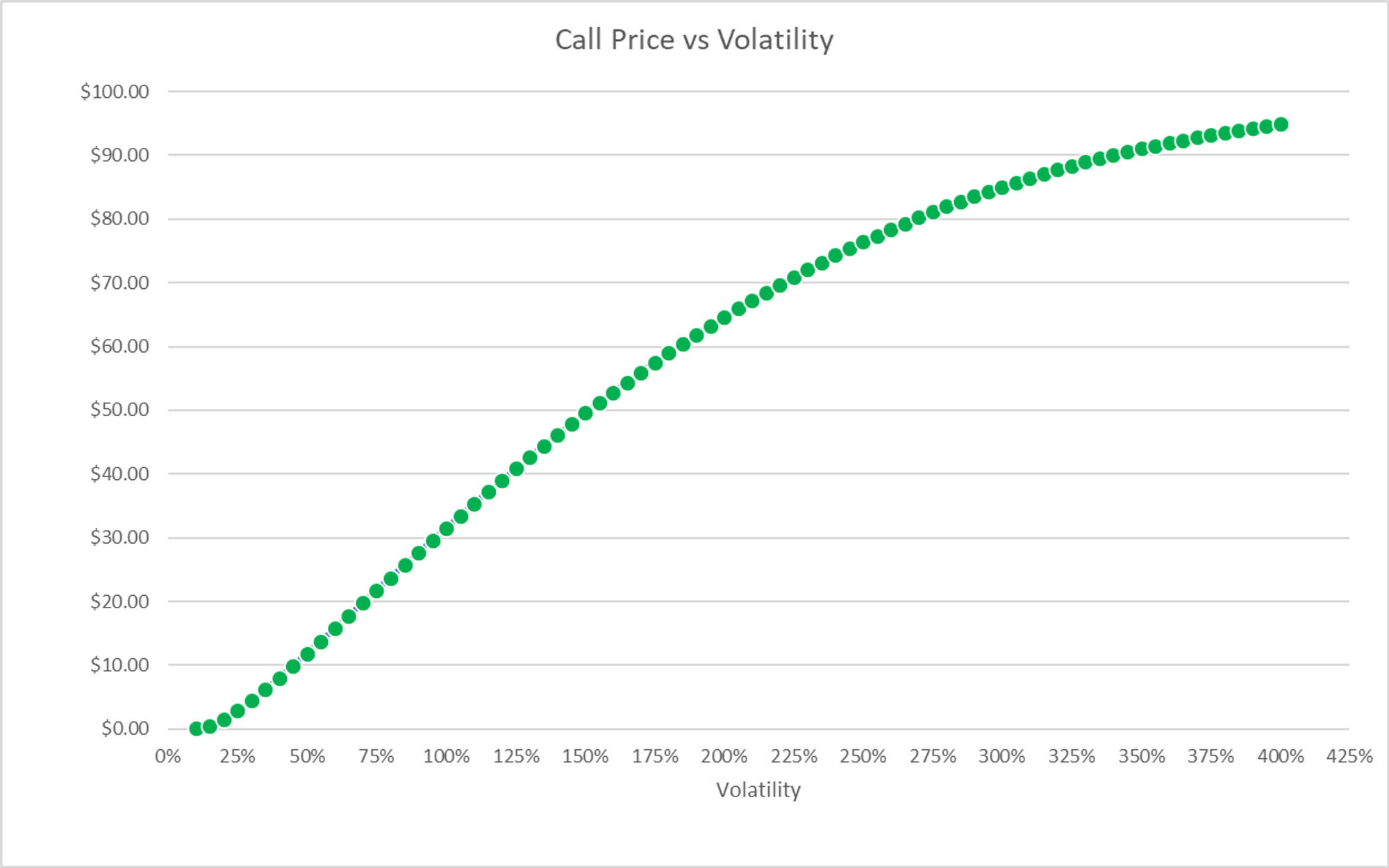

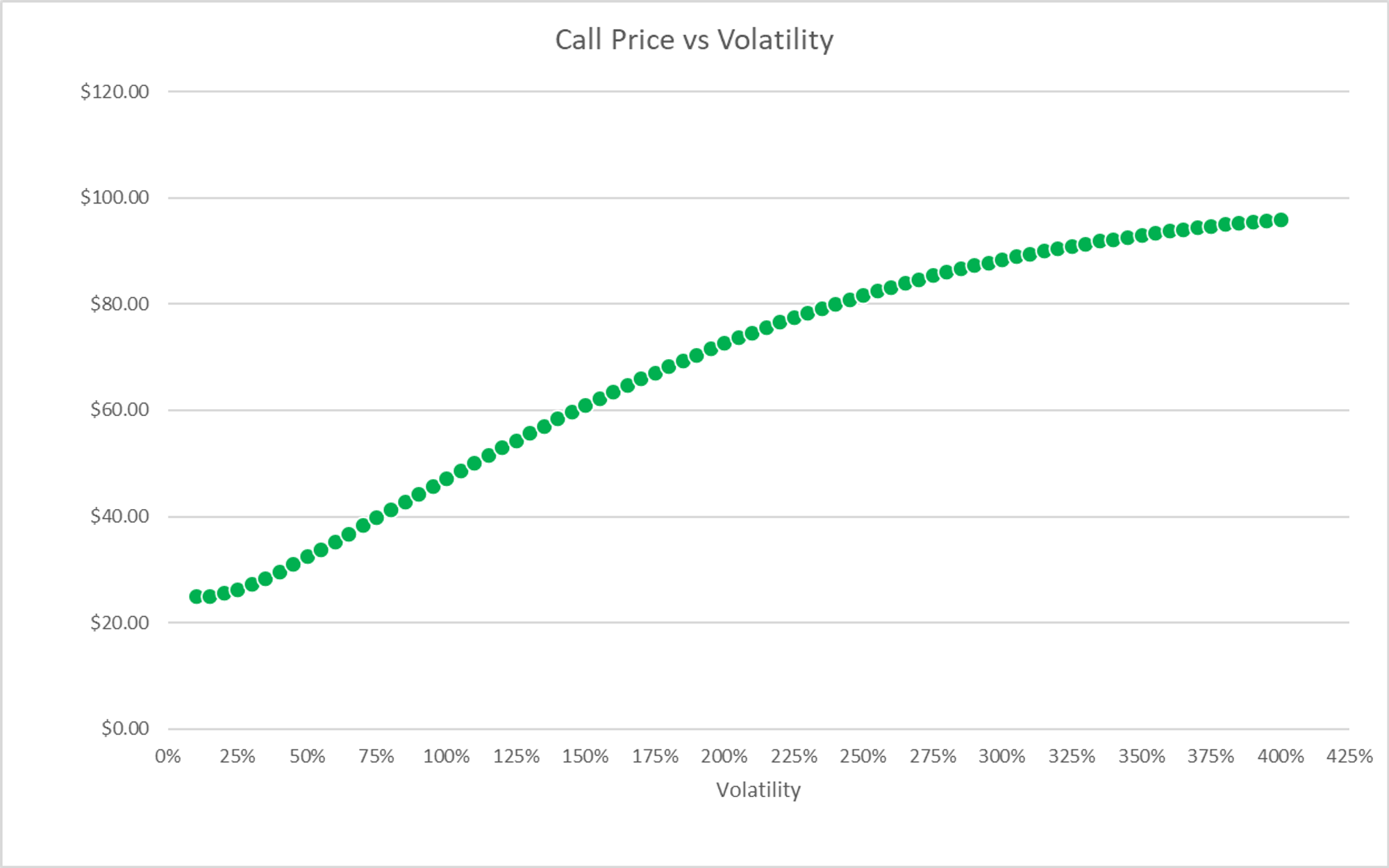

How Volatility Impacts The Call Price

Higher volatility increases the value of all options.

The maximum a call can be worth is the stock price itself. Here we can see that an annual volatility of 400% makes the 125-strike call nearly worth the spot price of $100!

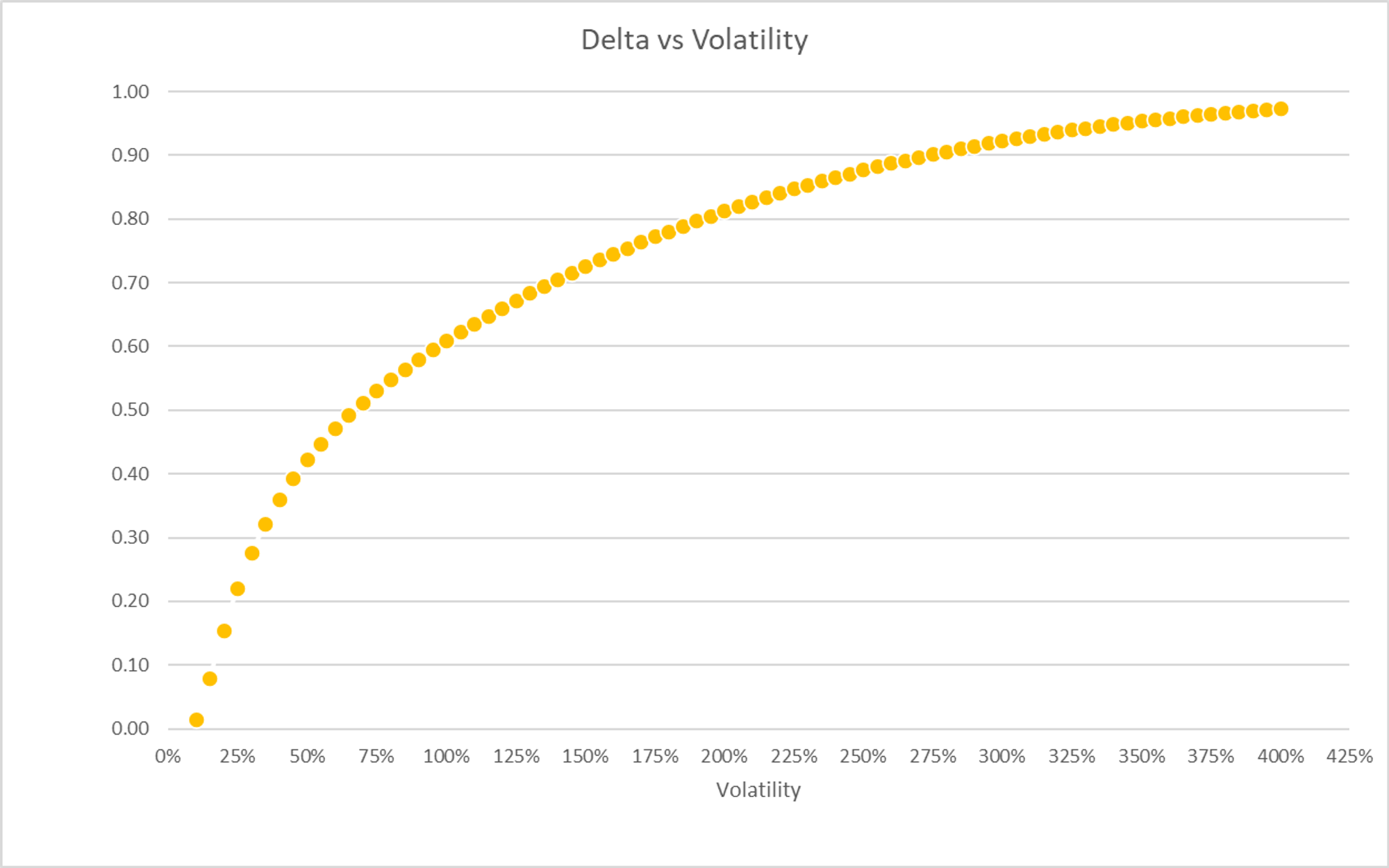

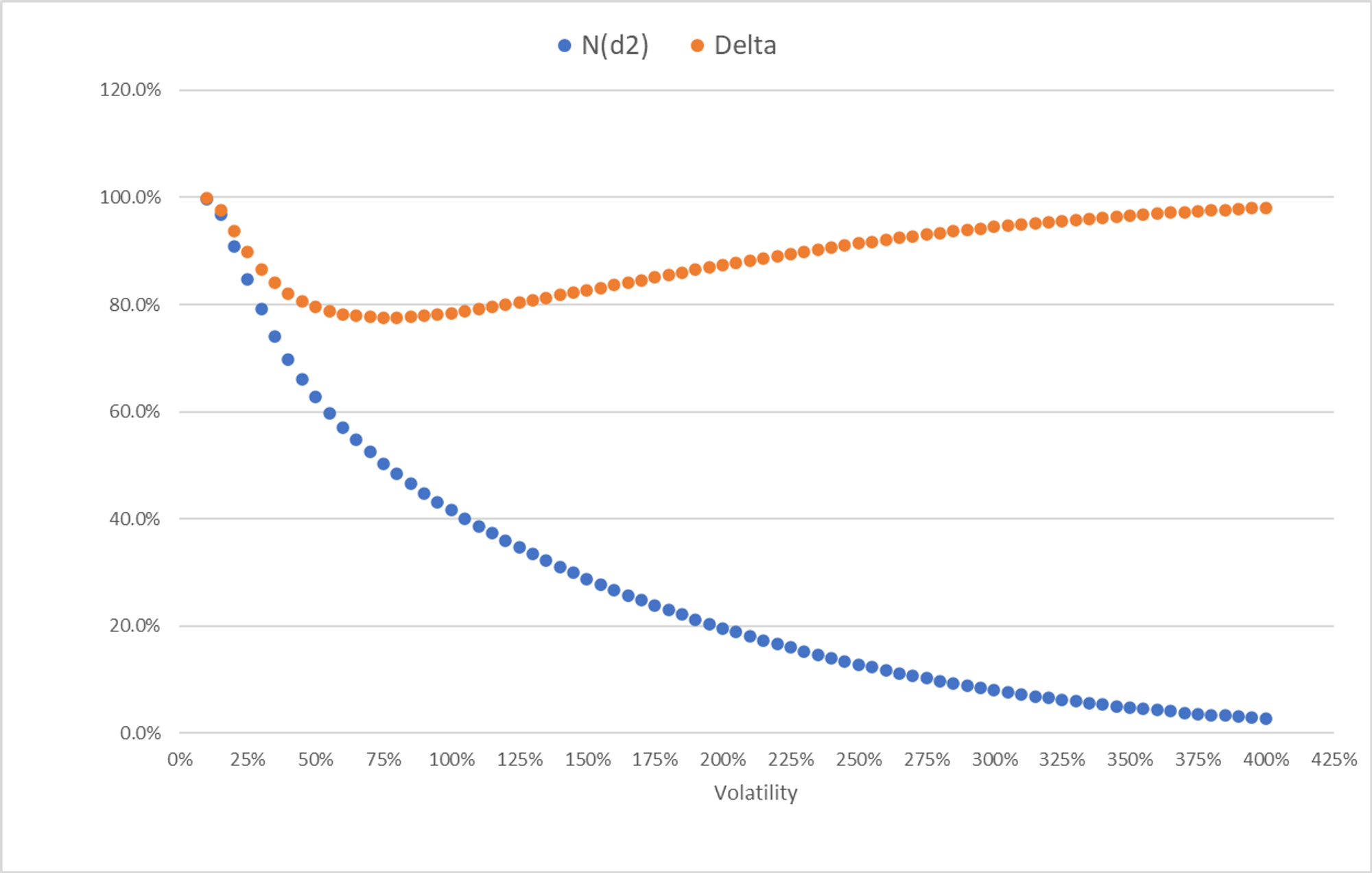

How Volatility Impacts N(d1) aka delta

Higher volatility pushes the deltas of out-of-the-money options towards 1.00

Intuitively, if you increase volatility to the maximum, the option price asymptotically approaches the spot price. Once the volatility is so high the option is simply worth the spot price. Which means it will move dollar for dollar with the spot price. If spot goes to $105, the option value will also go to $105.

The hedge ratio or delta is clearly 1.00 at that point.

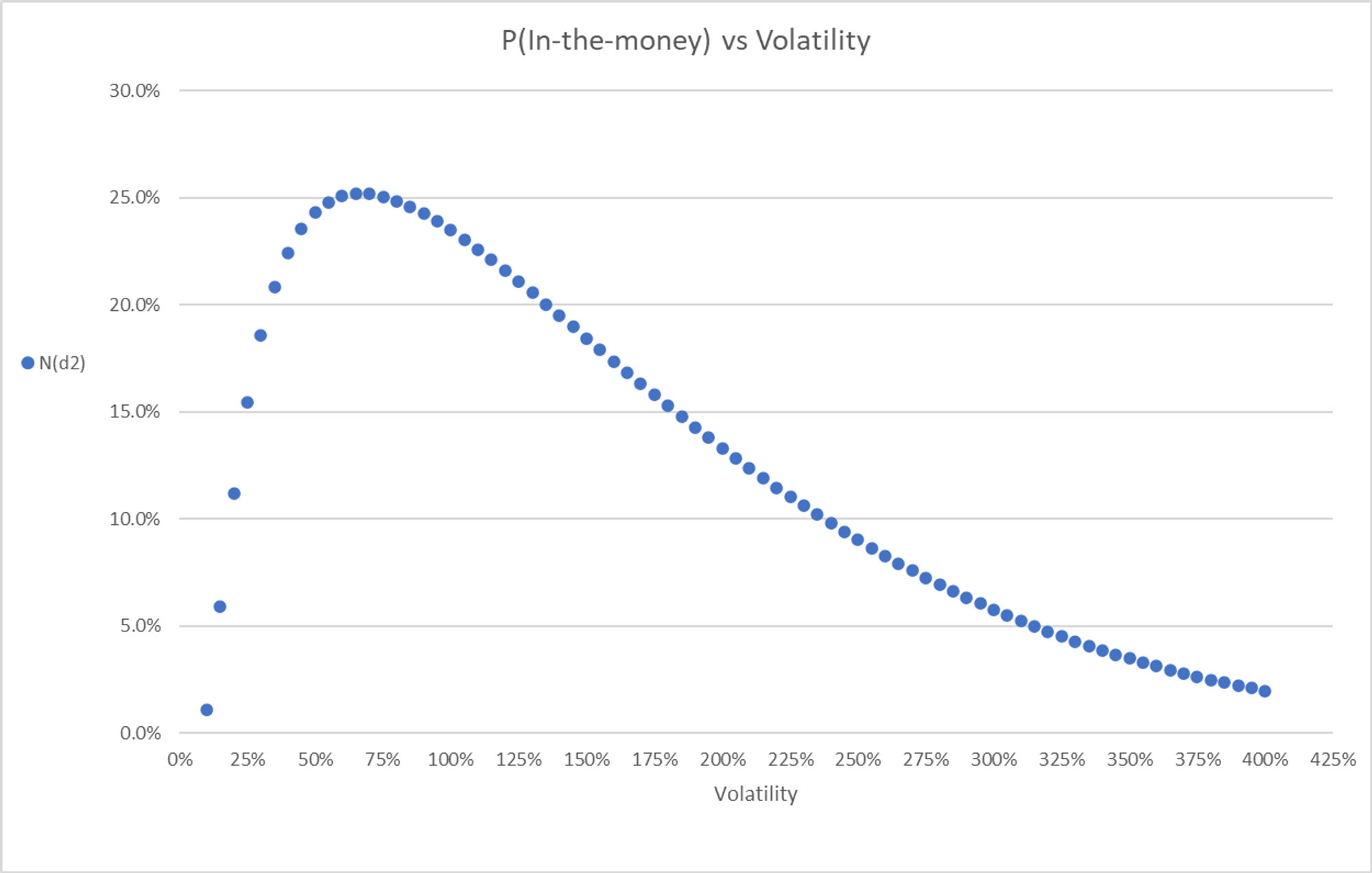

How Volatility Impacts N(d2) aka probability of expiring in-the-money

Higher volatility has an ambiguous effect on N(d2)

For “reasonable” increases in the level of volatility the 125 call is more likely to finish in the money. At a 75% volatility, the call has about a 25% chance of expiring in-the-money.

If the volatility was merely 5% the 125-strike would be several standard deviations away and highly unlikely to expire in-the-money.

But at higher levels of volatility, N(d2) shrinks again. The 125-call has about a 5% chance of expiring in-the-money with volatility at 15% or 300%!

What’s happening?

Increasing volatility starts to raise the probability that an out-of-the-money call will be in-the-money at expiration…but at some point, the increased volatility squeezes the mass of the lognormal distribution so far to the left that the distributional effect overpowers the higher volatility effect.

Remember as volatility increases, the Gaussian shape gets smushed with a median outcome closer to zero while being counter-balanced by a long, skinny right tail.

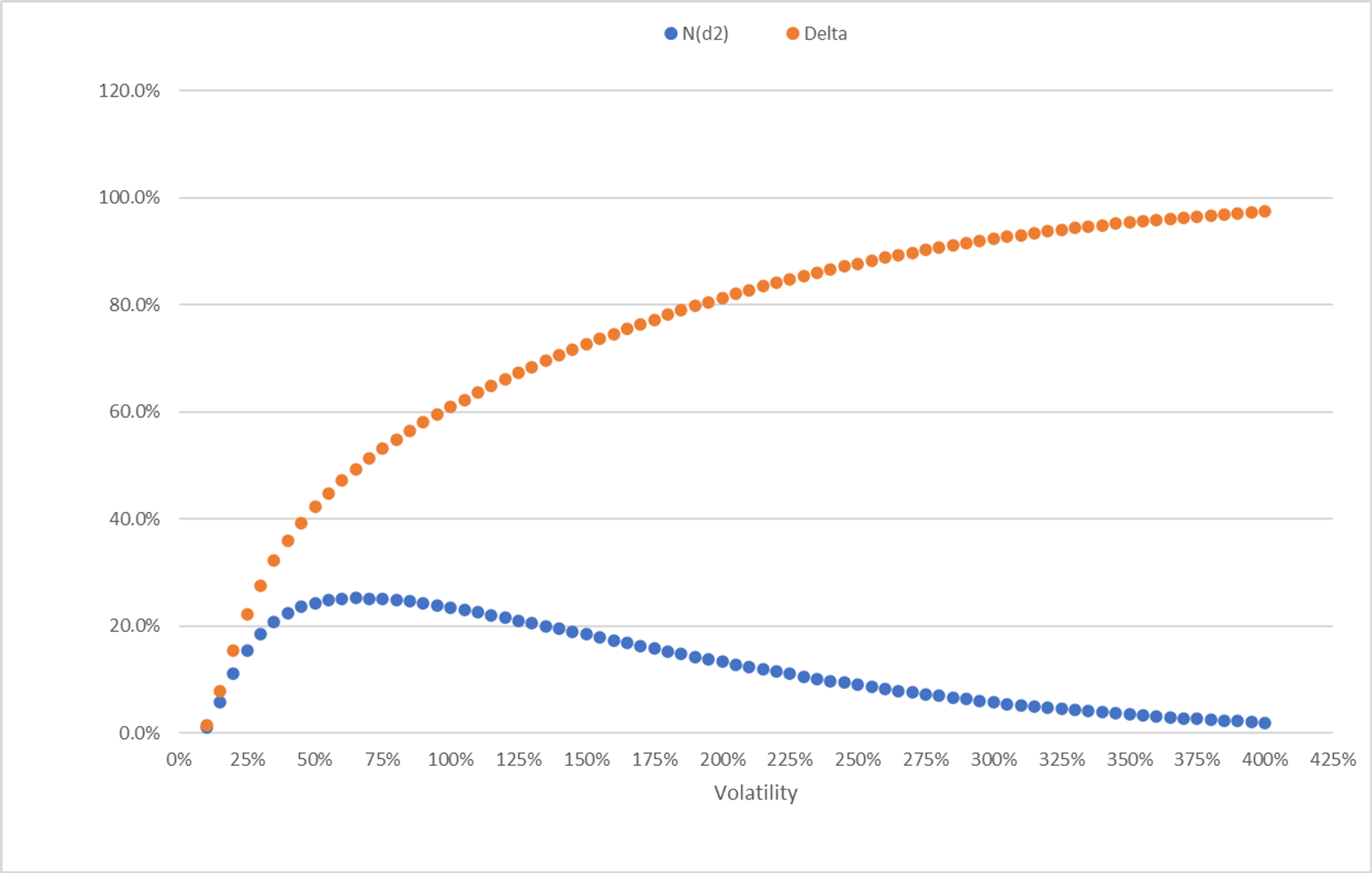

Conflicting Forces

Divergence between N(d1) and N(d2) on the call price

At sufficiently higher levels of volatility the delta, which keeps increasing, and the probability of expiring in-the-money diverge:

Let’s walk through the impact of the divergence by re-visiting the

The quantity of shares you need to own to hedge the short call keeps increasing with the delta. At extremely high levels of volatile you need to own shares in a 1 to 1 ratio against the short call.

At extremely high level of volatility, N(d2) approaches zero as the stock, despite its long right tail, has a most likely scenario of losing most of its value. Since the present value of the strike is weighted by a near zero probability, you don't expect to sell any stock at expiration to the counterparty who owns the call. There's no future expected cash flow from a sale to borrow cash against. In other words, you cannot finance the 100% delta worth of shares you need to buy to hedge.

The upshot: the replicating portfolio simply requires you to buy the shares and there's no way to finance them. So the call option is just worth the share price itself!

Delta of in-the-money options as you vary vol

Let’s switch the strike from 125 to 75. The rest of the inputs are unchanged, we are just looking at the call that’s in-the-money by $25 instead of out-of-the-money by $25

We’ll cut right to the chart.

Notice that the call starts at 100% delta and nearly 100% chance of expiring in-the-money. But as we start raising volatility:

N(d2) just continues to fall throughout the vol increase. Unlike the OTM call which saw an initial increase in N(d2) before the lognormal effect overpowered it, the ITM call just becomes less likely to expire ITM.

This is intuitive. If volatility is low a call so deep ITM is very likely to find itself ITM at expiration. But if you raise volatility, well, that probability has nowhere to go but down since increasing the spread of possible returns introduces the possibility that it will not be ITM by expiration.

The lognormal distribution getting “smushed” to the left as vol increases reinforces this effect on N(d2) for the ITM option.

It’s the delta that now sees an inflecting curve. Initially, the delta of the call drops from 100% to about 80% as the increased spread of possible returns effectively makes the call feel less in-the-money. As we raise vol, that $25 of being in-the-money creeps more towards feeling at-the-money.

This is the idea behind the intuition you’ve probably heard — raising vol pushes ITM option deltas towards .50

But…as vol increases to “very high” levels, the slim but long right tail of possible stock returns starts to push the hedge ratio (the amount of shares you’d need to replicate the option) back up towards 100%!

The call price still increases towards the spot price of $100 as vol gets ridiculously high.

Dynamic hedging

If you run many Monte Carlo simulations according to the assumptions of the B-S model including the underlying distribution, on average, the call value would match the predicted model value.

If you worked through my game example The Snake Eyes Options you’ll recognize that this is the same thinking. It’s just expected value and conditionals. Black-Scholes just requires calculus to handle the continuous rather than discrete underlying distribution.

❓

Simpler versions: first round interview question I faced in 1999

You flip a single die and will paid $1 times the number that comes up. How much would you pay to play?

Suppose I let you take a mulligan on the roll. Now how much would you pay?

Congratulations, you just priced an option.

Of course, any one simulation will have massive noise in the option value compared to the Black Scholes value.

If you sell an option worth $7.00 at $7.20 you expect to make 20 cents on average. However, the standard deviation of the p/l will be massive. (We are even making the unrealistic assumption that the vagaries of the stock are drawn from the underlying lognormal distribution, mean, and volatility that we used to generate the model price).

If you hedge the delta of the option periodically, you are attempting to replicate it for the cost of $7.00 and pocket the difference. The more you hedge, the closer that replication value will approach $7.00.

Hedging itself is a cost that the model assumes to be free (no slippage or transaction costs).

Another thing you could do in this made-up world we are using for demonstrating principles — you could sell overpriced options across many names and not hedge at all. In theory, you should still earn that $.20 and diversification handles the variance instead of hedging.

Of course, delta risks will swamp option edge. If you sell that option contract at 31% vol when the underlying go on to realize 30% that will be invisible compared to the wild swings in p/l that come from where the stock eventually ends up.

In other words, isolating a trade where you think the asset is going to move 2% per day instead of 2.2% a day is not best expressed by just letting your deltas run. Your trade thesis hinged on mispriced volatility and that is not what you are betting on when you don’t hedge at all.

In the real world, hedging is discrete. It can be automated or discretionary. It is a rabbit hole of obsession amongst vol traders. The main point is that hedging reduces variance in exchange for a cost.

[Buy Financial Hacking for chapters worth of discussion on this topic. An especially useful bit from the author’s sims was how the reduction of risk is proportional to the square root of how often you hedge. For example, if you want to halve the variance of your trades from whatever it is now, hedge 4x as often].

Because replication (ie hedging) is costly, in practice it is a bit of an art depending on how diversified a portfolio is and how positions are sized.

For my extensive overview of hedging, in general, see: