In No Easy Trades Principle I explain how expected mean reversion in realized vols makes it difficult to find implied vol trades that carry well.

Bennett demonstrates that reality using "volatility cones" (this is also how visualized this effect in practice).

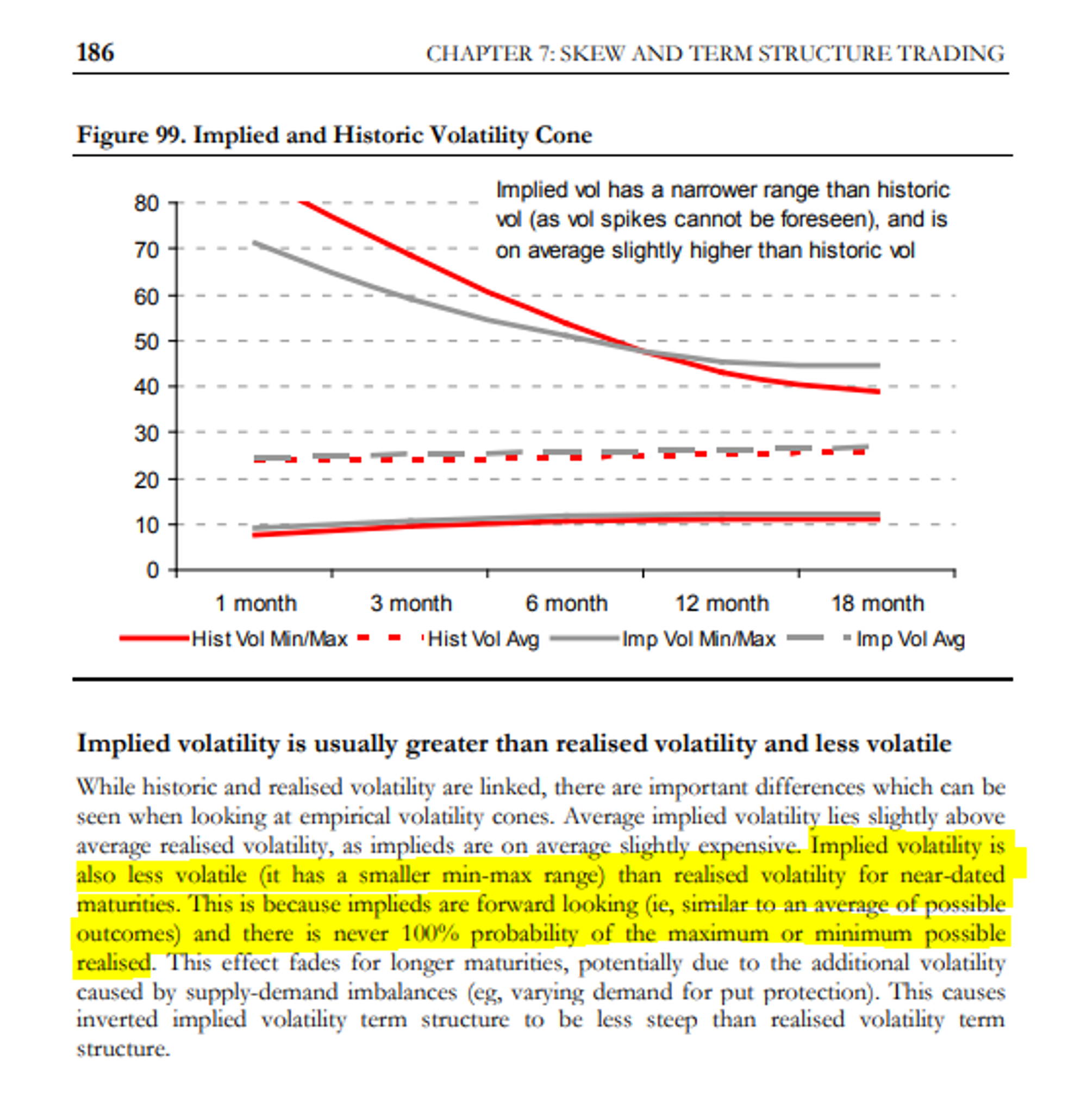

The range of realized vols is wider than implied vols. This effect fades as you look at further maturities.