This homework will help a student think about vertical spreads and probabilities in options.

Prerequisites:

basic probability including conditional probability (although you do not need Bayes Thereom, just logic. You will need to do a lot of reasoning the same way you need to turn any word problem into math statements)

Excel or your preferred computational tool

First, a self-indulgent remark…

I enjoy helping people learn about options. Not for instrumental reasons like the “world needs more options traders”. But in an appreciative sense — option theory is a rich toolbox for decision-making in investing and life in general. The word “decision” implies an option.

Notwithstanding, the typical person learning about options is thinking instrumentally — “how do I use these things to make money?” Of course, there’s no blog post or even book-sized answer to this question. As any craft goes, there’s basic vocabulary and principles, but these are necessary but insufficient conditions for success. You need years of trial and error to achieve competence.

Since trading/investing is a low signal-to-noise endeavor your epistemology requires strict discipline — the flip side of narrow bid-ask spreads and low-cost trading means your lack of edge can be masked for a long time. You know a loan shark is a bad deal, so you only visit Sleepy Sal as a last resort. But one broken kneecap and your LTV goes to zero. Brutal but honest. Everyone understands the deal.

Meanwhile, Robinhood administers the morphine of hidden fees to lengthen the duration of its most valuable asset — your overconfidence. Robinhood calls itself Robinhood without a hint of irony. They ate the whole wheel of cheese. I’m not even mad, I’m impressed.

Good news

At risk of pollyanna-posting, I’ll propose just getting smarter. If you have read this far you are totally capable of learning. Unsurprisingly, options discourse either tends to one of 2 poles:

Physics-esque math geekdom

Jargon-heavy complexity certainly has a place in finance but is best ignored as a small ecological niche.

The “option premiums are to be sold for passive income” grift

I’ve covered why this frame is nonsense ad nauseum here, here, here, and indirectly in almost all my writing.

There is a needle to be thread between these framings.

With no more than HS or even middle school math, you have enough tools to tinker and build intuition alongside your live experimentation. This homework is an example of what I’m talking about.

The purpose of this exercise

I get approached for help with options by retail traders frequently. On the one hand, it puts me in an uneasy situation — I’m not really a fan of people using their precious human capital on a machine that conspires to make you think it’s worth trying when base rates say otherwise. On the other hand, who the hell am I to discourage grown-ups who have read the disclaimers and proceed anyway. On balance, it’s a good thing that card-counting books are on the shelves even if most people who fancy themselves Ed Thorp are delusional about what it takes.

So it goes….my sympathies point to being helpful even if the occasional learner impales themselves. They probably would have anyway and there are more people that will be saved by either re-allocating their attention when they realize this is a grind or shed the misunderstandings that keep them plateaued.

All of this really cuts to the heart of Moontower’s approach to unlocking others: part Zen and The Art Of Options Trading, part shedding misunderstandings.

I can’t give you answers, but I can help rule out wrong answers. In that spirit, this exercise, despite its simplicity, will stimulate growth-inducing reflection.

The origin of this exercise

A reader approached me about a strategy they were exploring. It was familiar because it belonged to the class of strategies I’d describe as “harvesting”. Sell some variation of optionality (cash-secured puts, covered calls, iron condors, strangles, etc), earn steady profits.

This reader is selling downside butterflies on the SP500.

When someone has researched a strategy, they are mentally invested in confirming that it works. So right off the bat, I was heartened by the reader’s honest approach — “Kris, tell me what’s wrong with my strategy?”

It’s a fair question. But it’s not quite the right question.

I haven’t done the work so I’m not in the best position to say whether the strategy is good or bad but more importantly…

The “teach a man to fish” Socratic lesson is to demonstrate the implicit misunderstandings of the reader’s approach. That will lead them to higher-resolution questions that will scaffold their ability to answer the original question.

Let’s get to the exercise

Scenario Description

⚙️

Assumptions

A stock is trading for $100.

The risk-free rate and dividends are zero so we can ignore cost of carry or hurdle concerns.

Options on the stock expire after 20 periods. You can think of them as days or weeks or whatever.

How the stock moves

In each period the stock can only go up or down

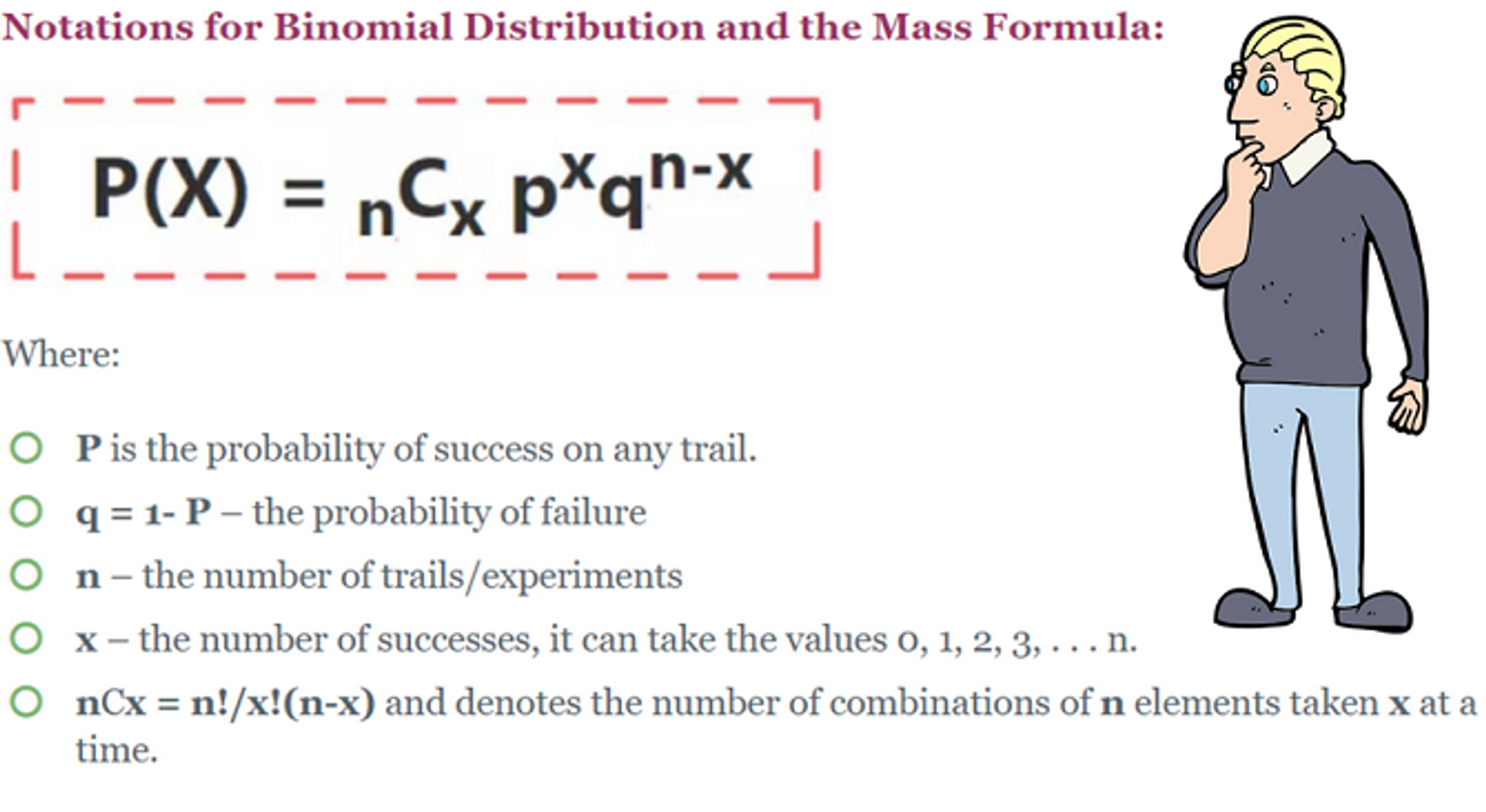

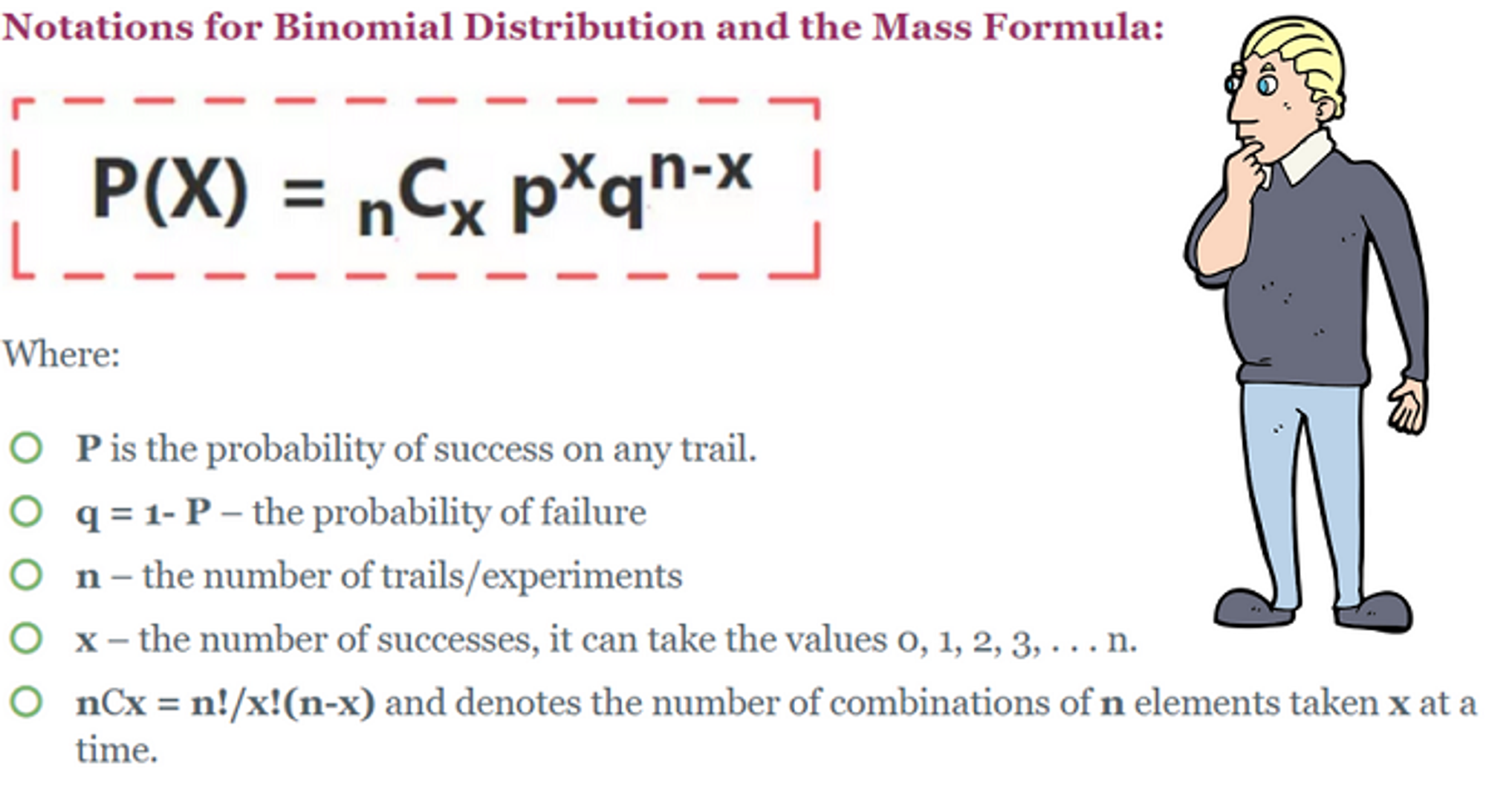

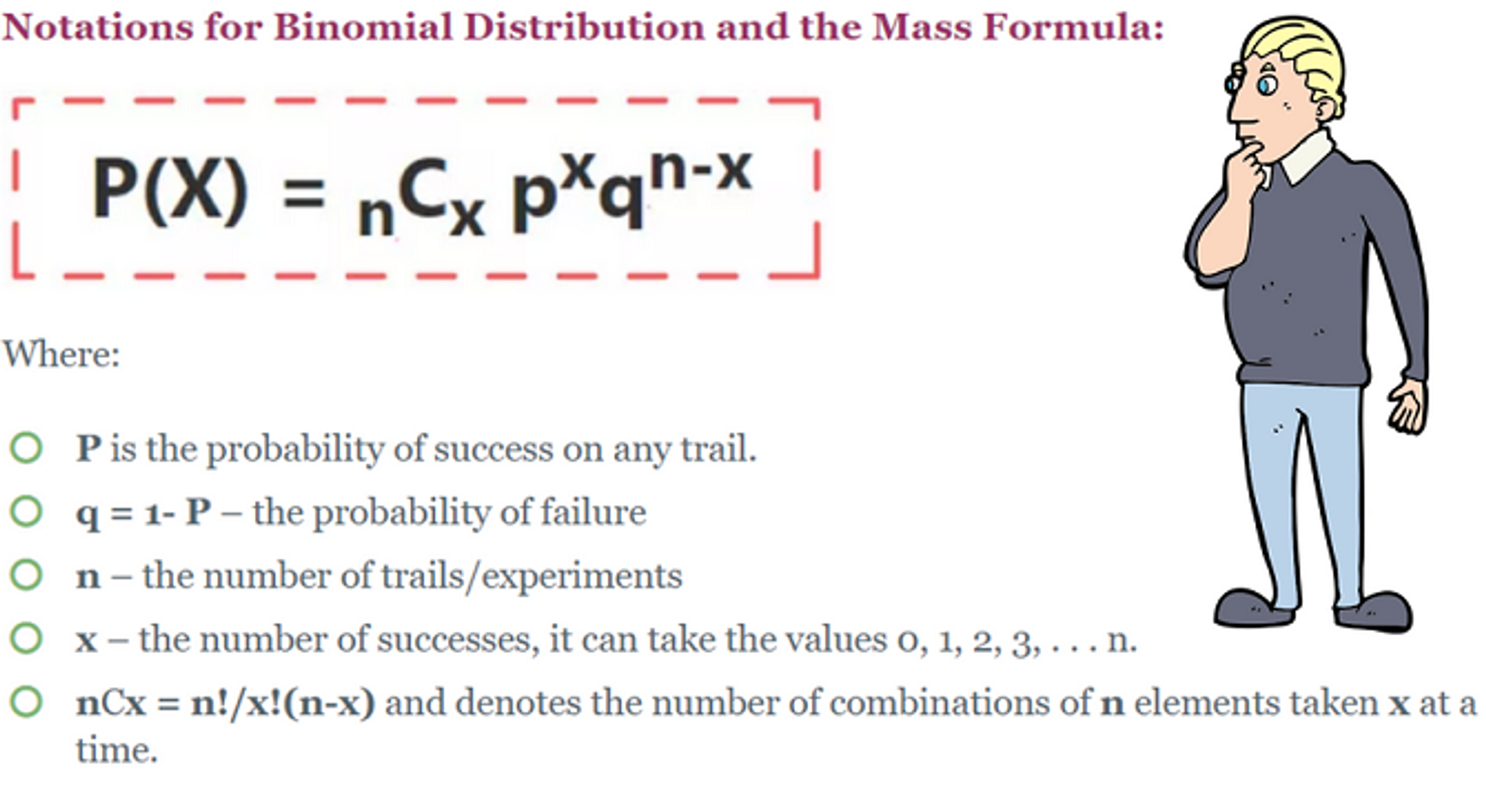

You may want to refresh yourself on coin flips or binomial distribution as encapsulated by this picture:

Probabilities and Magnitude

P(up) = probability stock increases in value = 52.5%

P(down) = 47.5%

Magnitude: The stock always moves $1.00

Part I: Set-up Computations

📊

Understanding the distribution

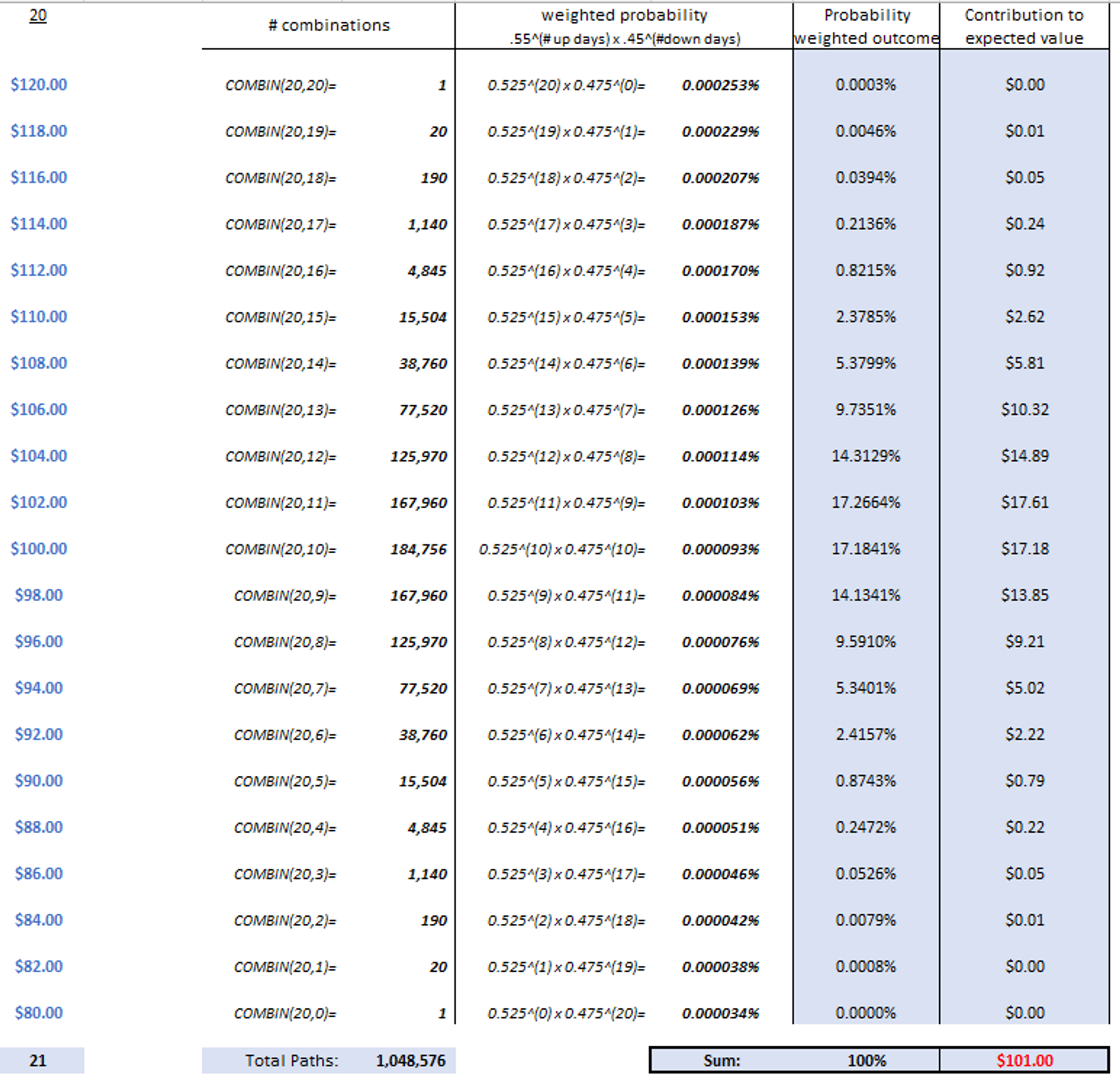

For any single period, the stock is 52.5% to go up $1 and 47.5% to go down $1. What’s the expected value of the stock after the first period? After 20 periods? The stock starts at $100

1 period

.525 x $1 + .475 x -$1 = $.05 so after the first period the expected value of the stock is $100.05

20 periods

= $100 + 20 * expected profit per trial

= $100 + 20 * $.05

= $101.00

After 20 periods, how many possible outcomes are there?

Hint

My favorite technique — do a simpler version of the problem first.

What’s the sample space after 1 period:

$101 or $99…2 possible outcomes

What’s the sample space after 2 periods:

3 possible outcomes:

Down 2x: $98

Up 2x: $102

Up, down or down, up: $100

Note there are 4 possible paths and 3 possible outcomes. after 2 periods

What’s the sample space after 3 periods:

4 possible outcomes:

$97

Down 3x

$103

Up 3x

$99

Up, down, down

Down, down, up

Down, up, down:

$101

Up, up, down

Down, up, up

Up, down, up

Note there are 8 possible paths and 4 possible outcomes. after 3 periods

Are you seeing a pattern?

Answer to the number of outcomes

Based on the hint you can see the pattern.

For n periods, there are n + 1 outcomes.

So for 20 periods, there are 21 possible price outcomes.

Answer to the number of paths

Based on the hint you can see the pattern.

For n periods, there are 2ⁿ paths:

1 period = 2 paths

2 periods = 4 paths

3 periods = 8 paths

So for 20 periods, there are 2²⁰ or1,048,576 possible price paths.

Visual answer

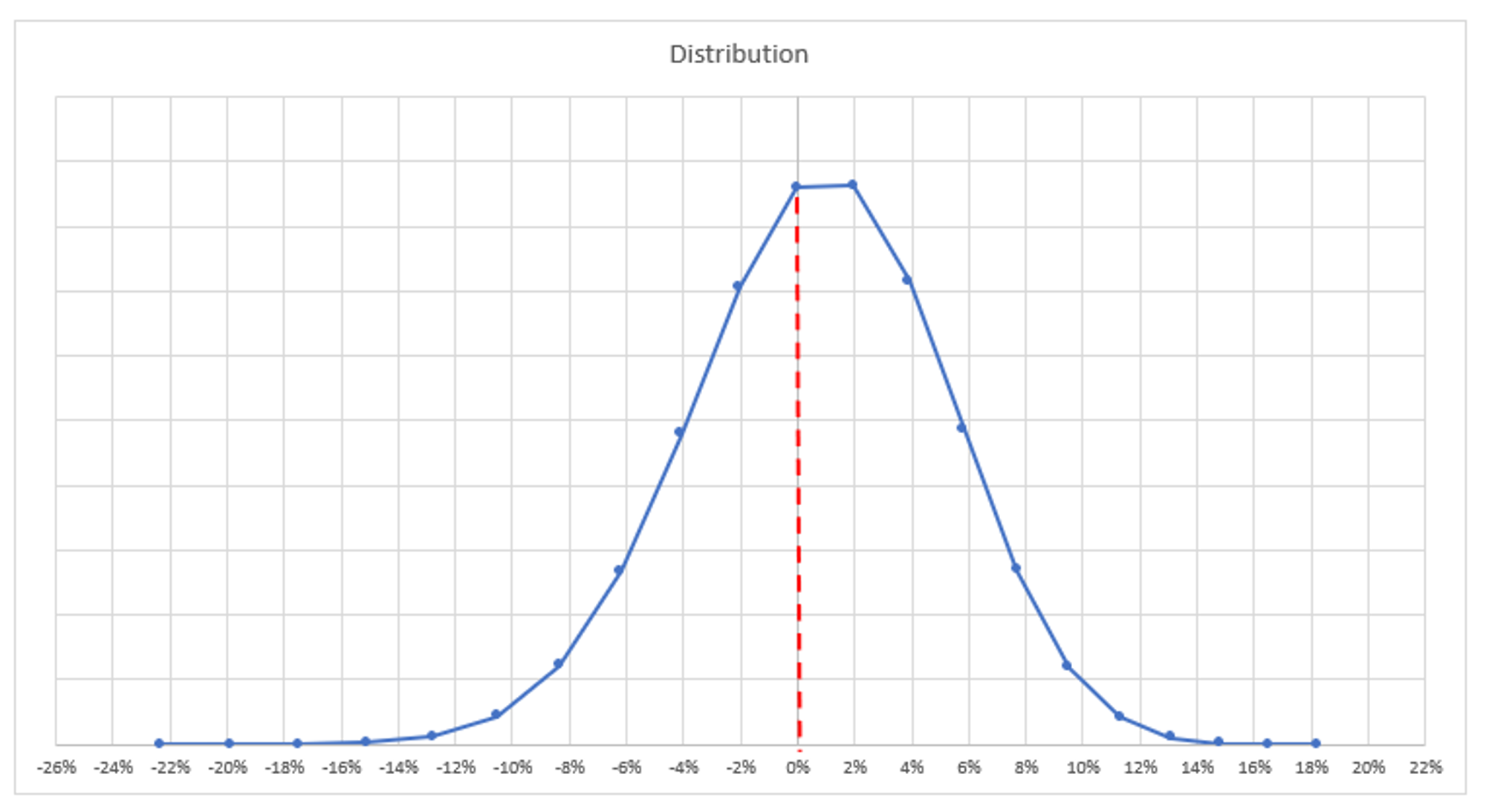

Just like coin flips, this simple up/down model conforms to the basic binomial distribution.

Again, this picture:

While we used 2²⁰ to find the total number of price paths, there are only 21 possible outcomes.

The binomial distibution is represented by a binomial tree. the ₙCₓ term is a coefficient that denotes how many combinations can generate a particular outcome.

A simple example is there is only combin(20,20) or “20 choose 20” ways to have 20 up moves in a row. In other words, only 1 path out of 1,048,576. This is true and symmetrical for 0 heads in a row for 20 straight trials.

A neat trick is you can use Pascal’s Triangle for n = 20 to see all the coefficients instead of computing them with a combination function.

We will come back to the return distribution in the conclusion as we relate this exercise to real life.

🏒

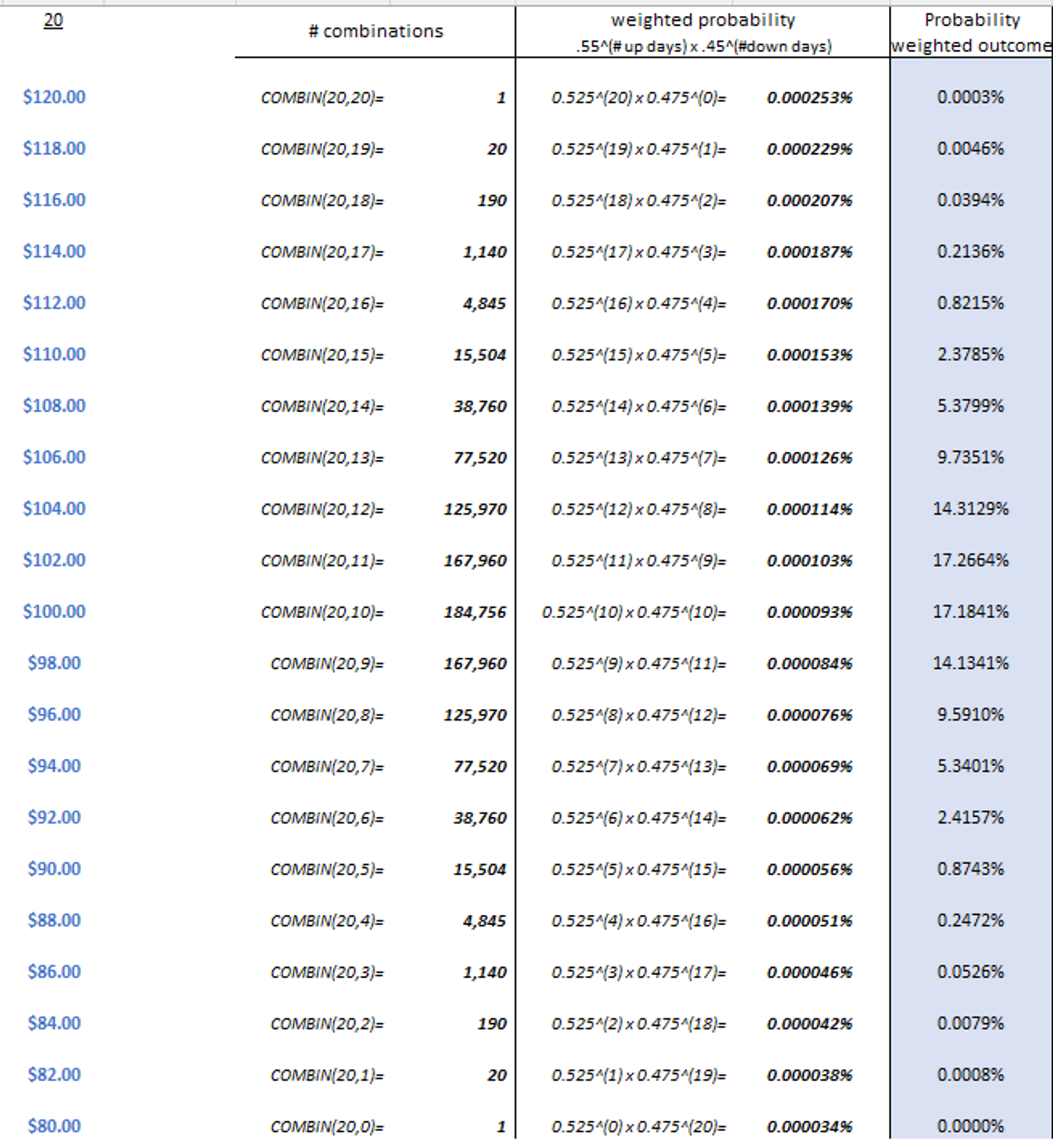

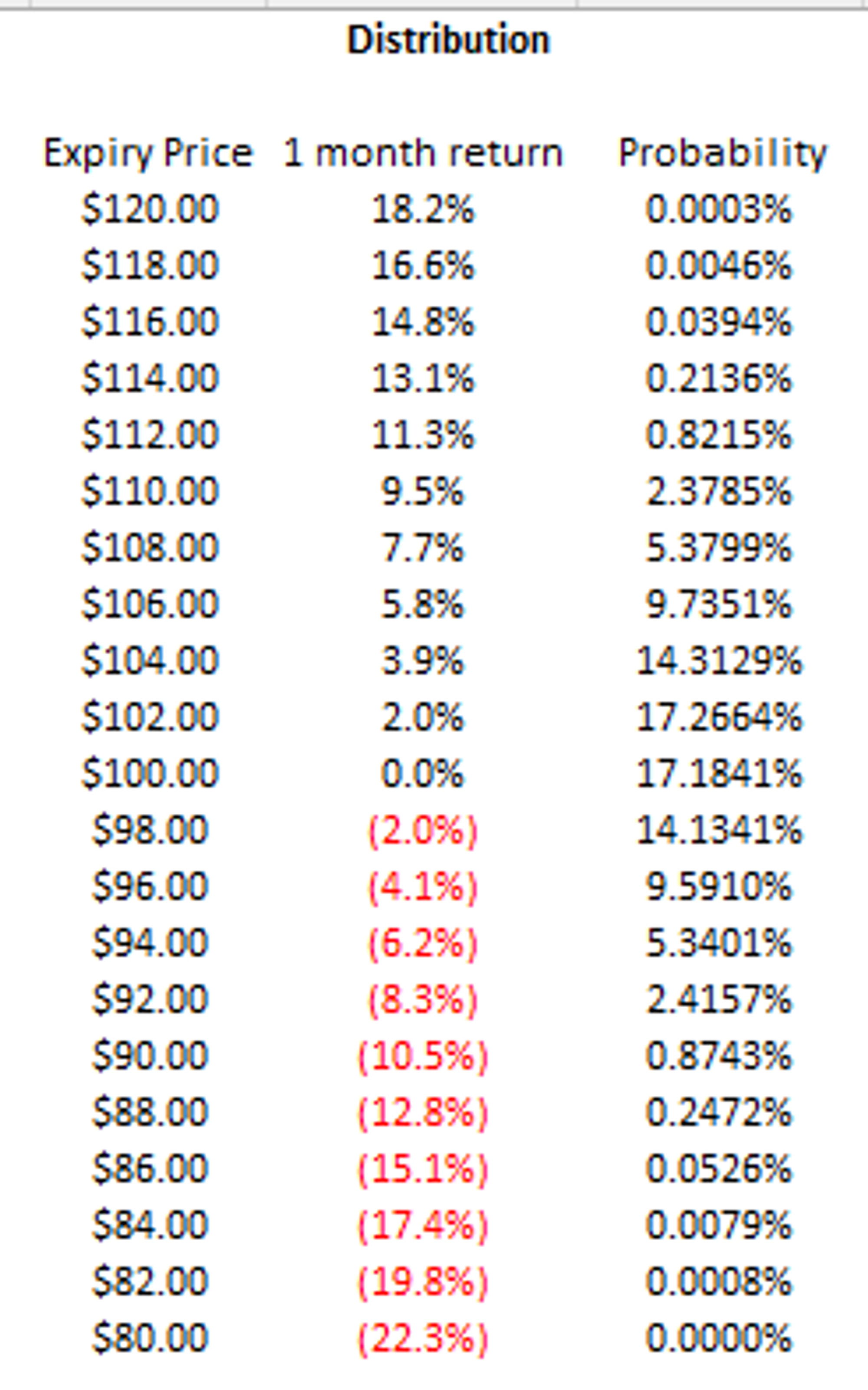

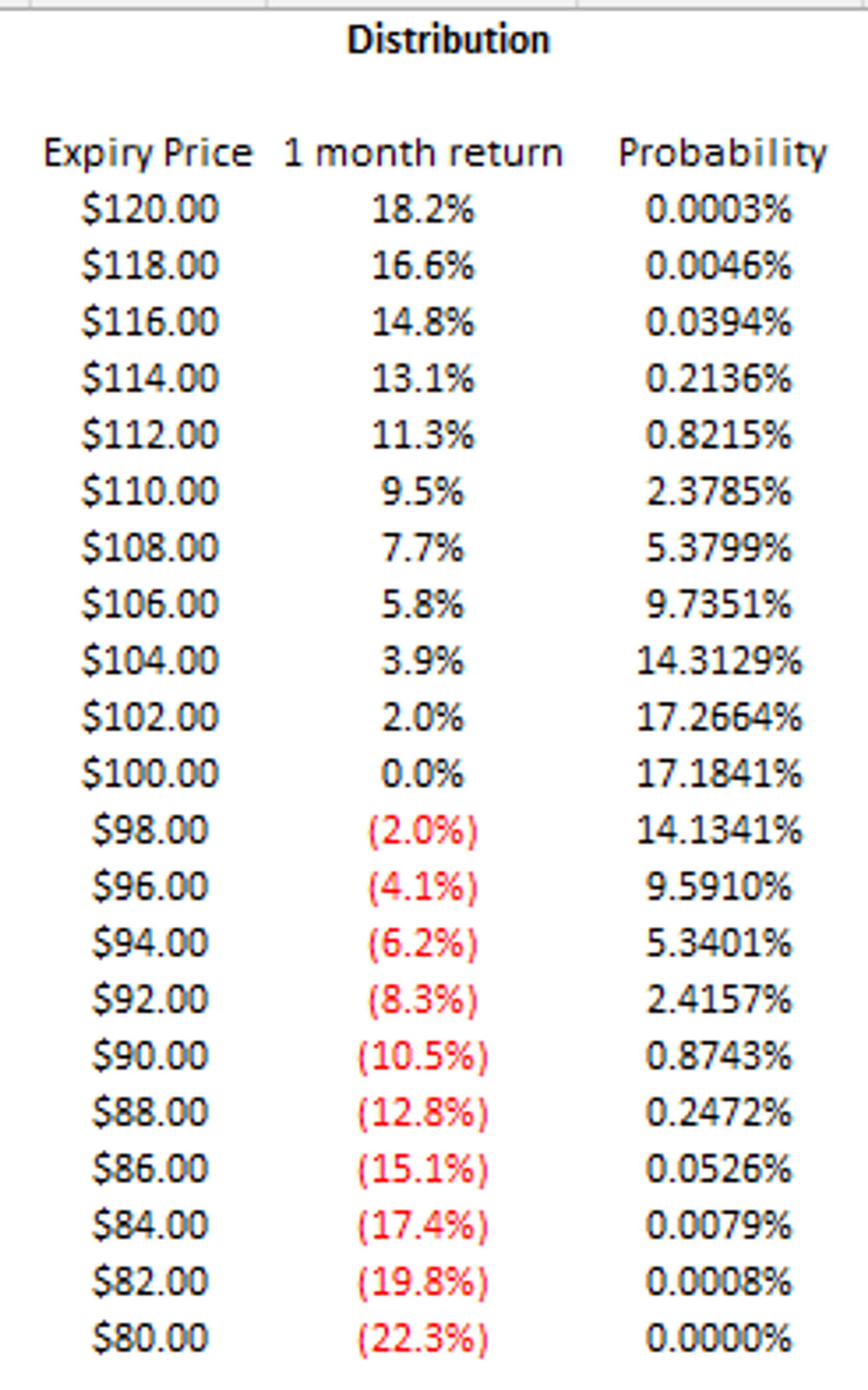

Pricing Options

In this discrete distribution, we know there are 21 possible terminal prices for the stock after 20 periods. By knowing all the possible expiration prices and their probabilities we can price an option for any strike by simply weighting all of the possible payoffs.

Let’s start by pricing a few options.

🔑

HelpGeneral hint

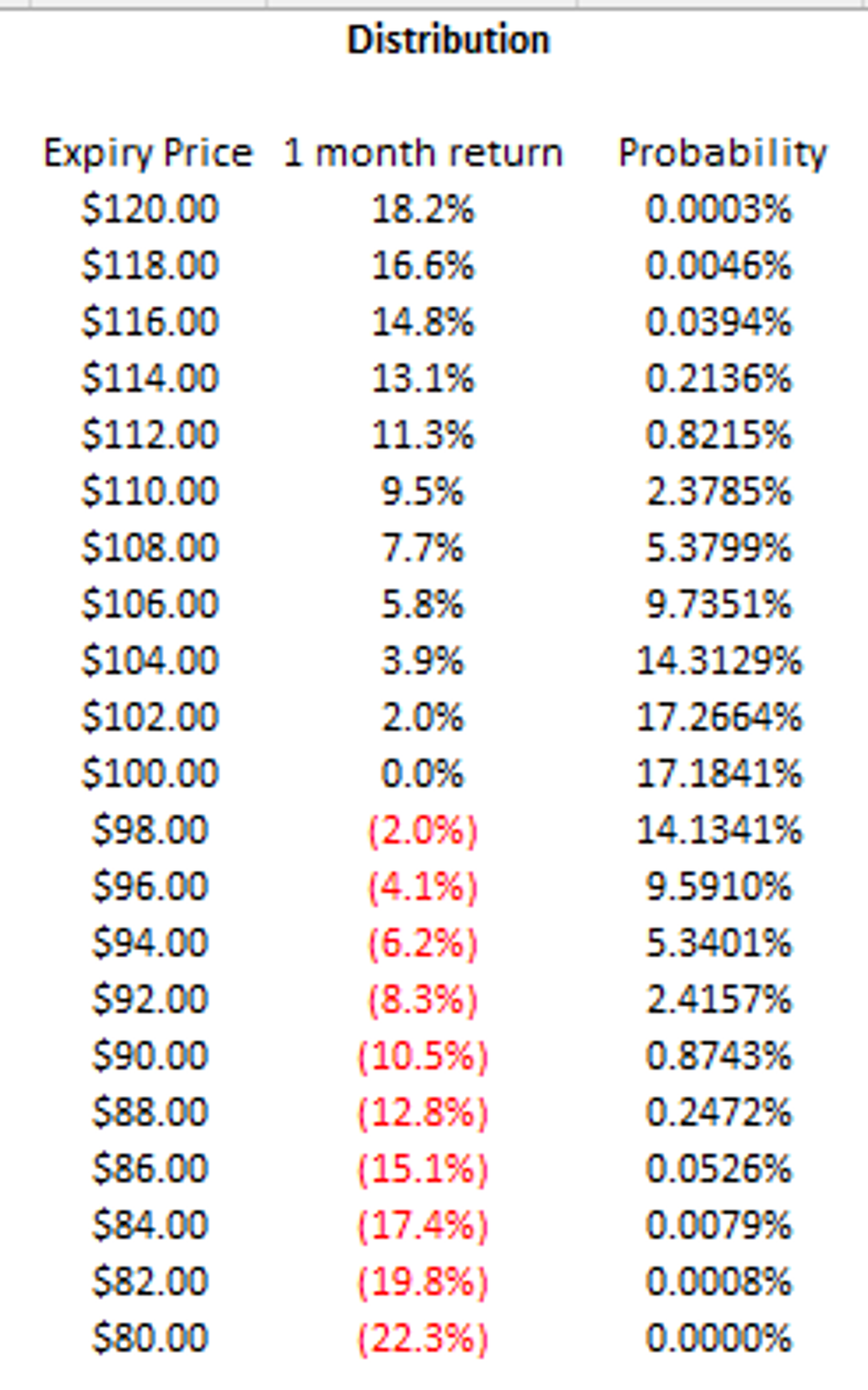

In case you need to refer to the distribution because you didn’t compute it yourself

What is the fair value of the 105-strike call at the beginning of the 20 periods when the stock is $100?

Answer

How about the 100-strike call?

Answer

The 95-strike call?

Answer

Price all the call options for every strike from $80 to $120 incrementing by $1. It’s the same process as the above examples.

Answer

Congratulations!

All the heavy computational lifting is complete.

From here we will use the above tables to compute spreads and reason about what it means to trade vertical spreads and butterflies

📣

A word on spread trading in general

Every trade is based on a model of how the world works, even if that model is as basic as “stocks go up on sunny days in Chicago”. Models by definition are simplified representations of how things work.

When we spread trade (buying one instrument and selling a related instrument) we cancel out some amount of model-risk. If our stock valuation model is based on interest rates, when we buy and sell related stocks we are sterilizing the assumptions of the model by letting them offset. Of course, not every stock is equally sensitive to interest rates or whatever parameters our model takes, but the principle of offsetting remains substantial.

In the work you did above, you priced options in an actuarial manner based on an easily computable distribution. In the real world, models such as Black Scholes allow us to price options with continuous distributions and with a set of assumptions about how prices evolve. Everyone knows the assumptions break down in real life but the model’s value is not in its accuracy in absolute terms but as a measure or ruler.

If you have a broken scale, it will not represent your weight accurately but it will still be useful for comparing your weight to mine. How we calibrate a function depends on the use case. Similarly, my guitar can be tuned to itself so that it can reproduce a song pleasantly. But as soon as I start playing with others we need to make sure the group is in tune.

💡

A word on spread trading in options

An early lesson for options traders is the value of spreads in risk management. I can offset option risks such as exposure to delta, vega, gamma and so on by taking an opposing position in a similar option.

Vertical spreads, where you buy and sell options of different strikes in the same maturity, are terrific examples of this. They allow us to sterilize the impact of bad assumptions in the model itself by reducing the risk to simply distribution. Distributional risks are benign, like over/under bets. The max loss is known and we are insulated from risks like bad interest rate or volatility assumptions.

The closer the strikes are to each other the more the risks offset. As they get further apart the risks increase. We become more vulnerable to discontinuities in our assumptions. Imagine a $100 stock. If I told you that Carl Icahn would make a cash takeover bid of $120 IF the stock dropped below $95 (suppose he knew the board would be far likelier to accept in that scenario) then a naively continuous model would not realize that the 117 strike and 123 strike don’t have a regular relationship to one another. The distribution is not smooth between these points.

The less 2 instruments (or strikes) are related the less insulation you get from model assumptions you get from hedging.

Generally speaking, when we trade narrow vertical spreads or butterflies (which are spreads of spreads — even more insulation) we can say our position is “model-free”. Your risks are more proportional to distributional probability than magnitude which is a more benign circumstance.

Part II: Understanding Vertical Spreads and Butterflies

Quick refresher on verticals

A vertical spread is a simple option structure where you buy and sell different strikes within the same expiry month. They can be used directionally to speculate or hedge and their pricing is not heavily dependant on your model because of the reasons stated above. The model “cancels” out.

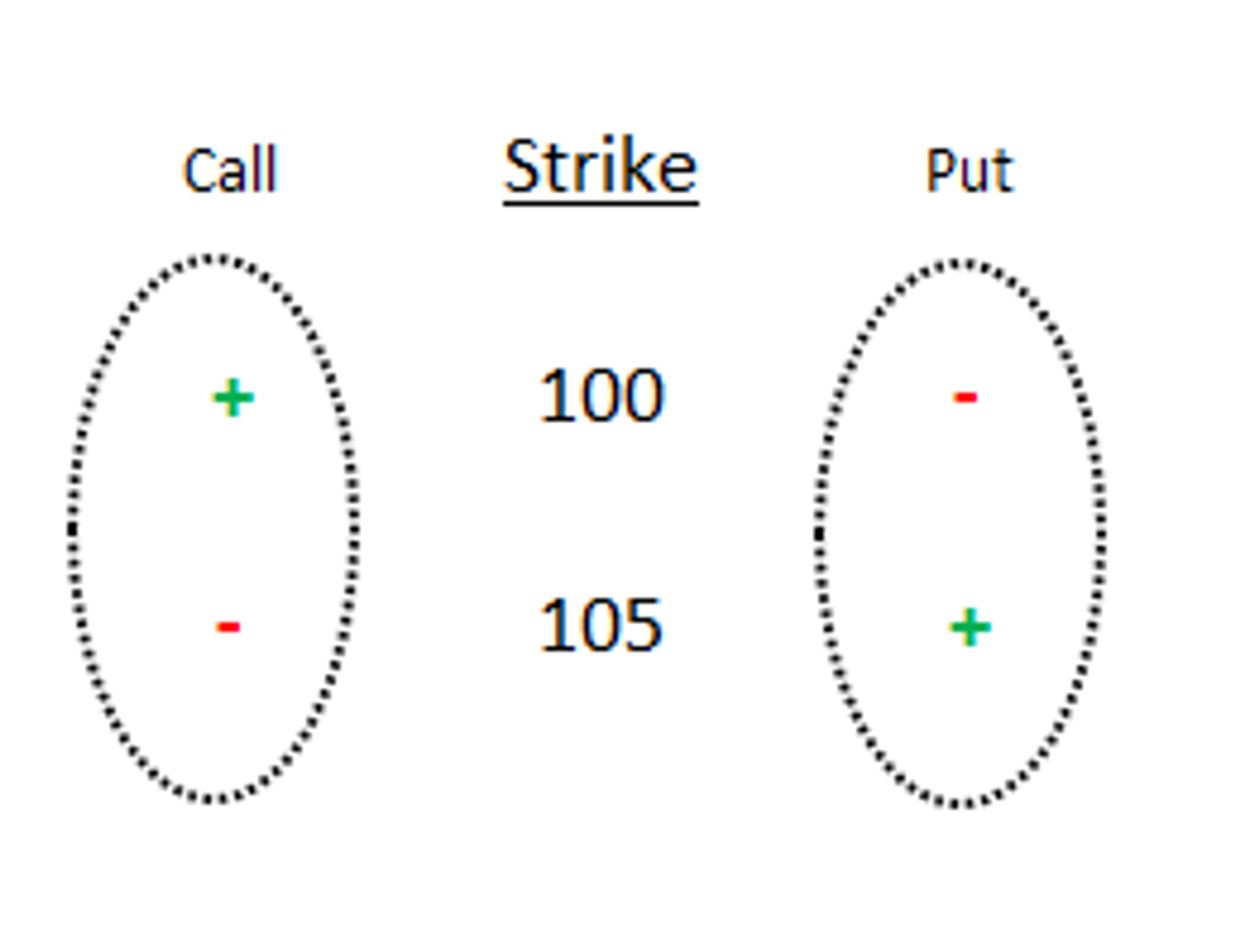

On credit/debit lingo

If I buy a lower strike call and sell a higher strike call, I say I’m long the call spread because I will pay a premium for this position. If I am long a higher strike put and short a lower strike put, I say I’m long the put spread. In general I’m long a spread if I paid a premium to own it regardless of whether its a bullish or bearish position. Retail lingo often calls this a debit spread because your account is debited the option premium. Pros usually just say whether they are long/short a call spread or put spread, with credit/debit lingo being more of a retail convention.

On advanced uses of verticals

Professional vol traders often trade vertical spreads, especially risk reversals that involve the purchase and sale of OTM calls and puts.

This means the strikes are typically far apart, and offset much less risk than tighter vertical structures. And that is often the point — the trader is speculating on the implied skew or spot-vol correlations. These are hairy, advanced trades.

I have done tons of these trades in my career, but I’ll admit — I kinda hate them. A non-exhaustive set of reasons:

“The skew knows” — the price of skew is reflection of risk premia and as I like to say “where the bodies are hidden”. Expensive skew tends to be self-fulfilling.

The position starts off vega-neutral but as the underlying moves towards (away) your long strike you will get longer (shorter) vega quickly.

You are nakedly exposed to cost of carry (rate/dividend) assumptions. Risk reversals do not offset those parameters. In fact, they doubly expose you to them.

In some, you are taking a bunch of risks that are hard to get paid enough to take given the range that skew parameters vary in. I usually got sucked into those trades because I was out of ideas, bored, or just stupid/masochistic in the vein of Tobias:

At expiration, an option is worth its intrinsic value if it expires in-the-money or zero if it expires out-of-the-money.

💡

The most a vertical spread can be worth is the difference between the strikes

Example

Today

I buy the 115 call for $2

I sell the 120 call at $.75

Net result: I paid $1.25 for the 115/120 call spread.

Expiration Scenarios

Stock expires at $135

The 115 call is worth $20

The 120 call is worth $15

Net Result: Call spread is worth $5. I make a profit of $3.75

Stock expires at $105

Both calls are worthless

Net Result: Call spread is $0. I lose my premium of $1.25

Stock expires at $118

The 115 call is worth $3

The 120 call is worth $0

Net Result: Call spread is worth $3. I make a profit of $1.75

🪙

Pricing vertical spreads

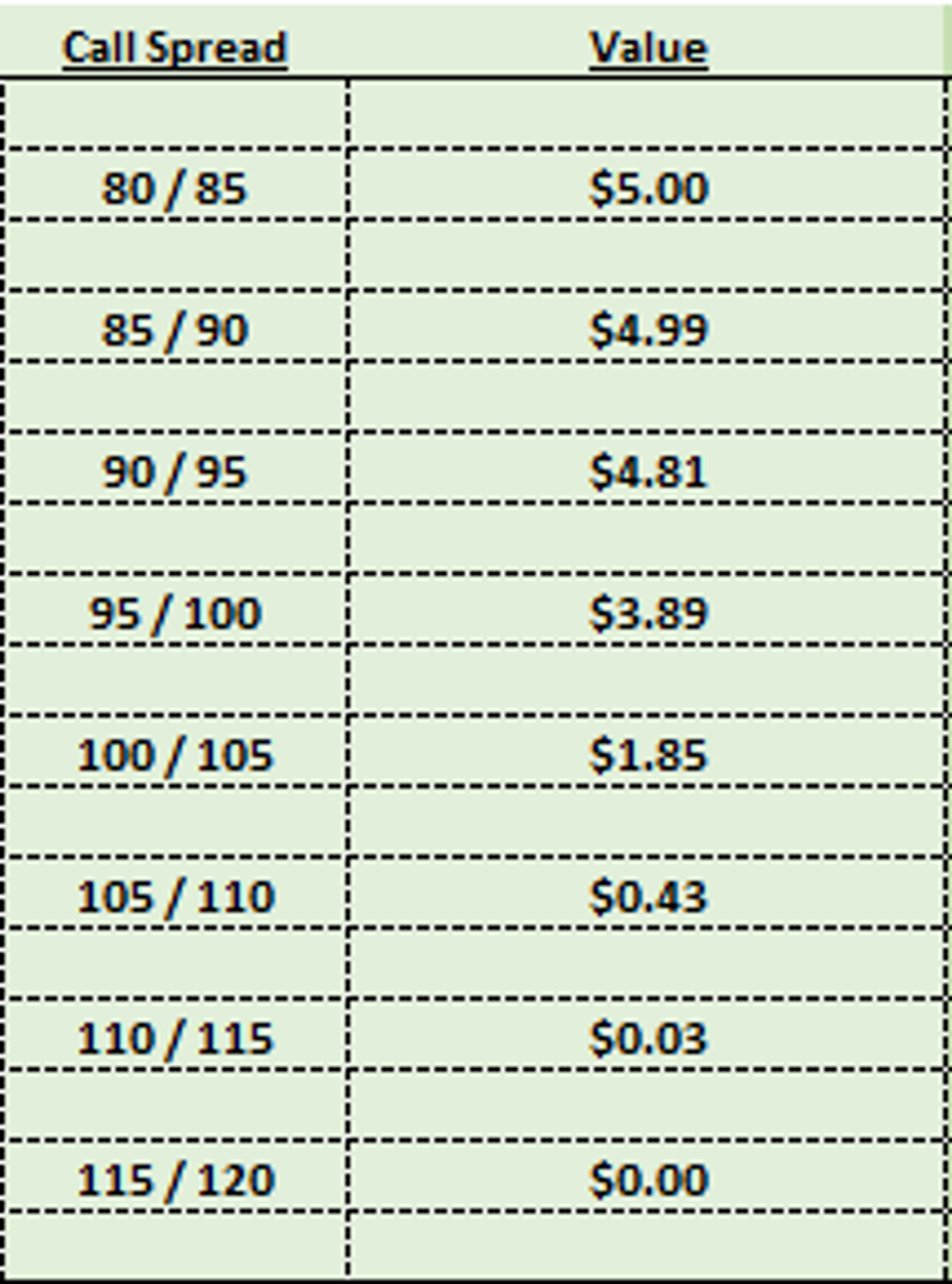

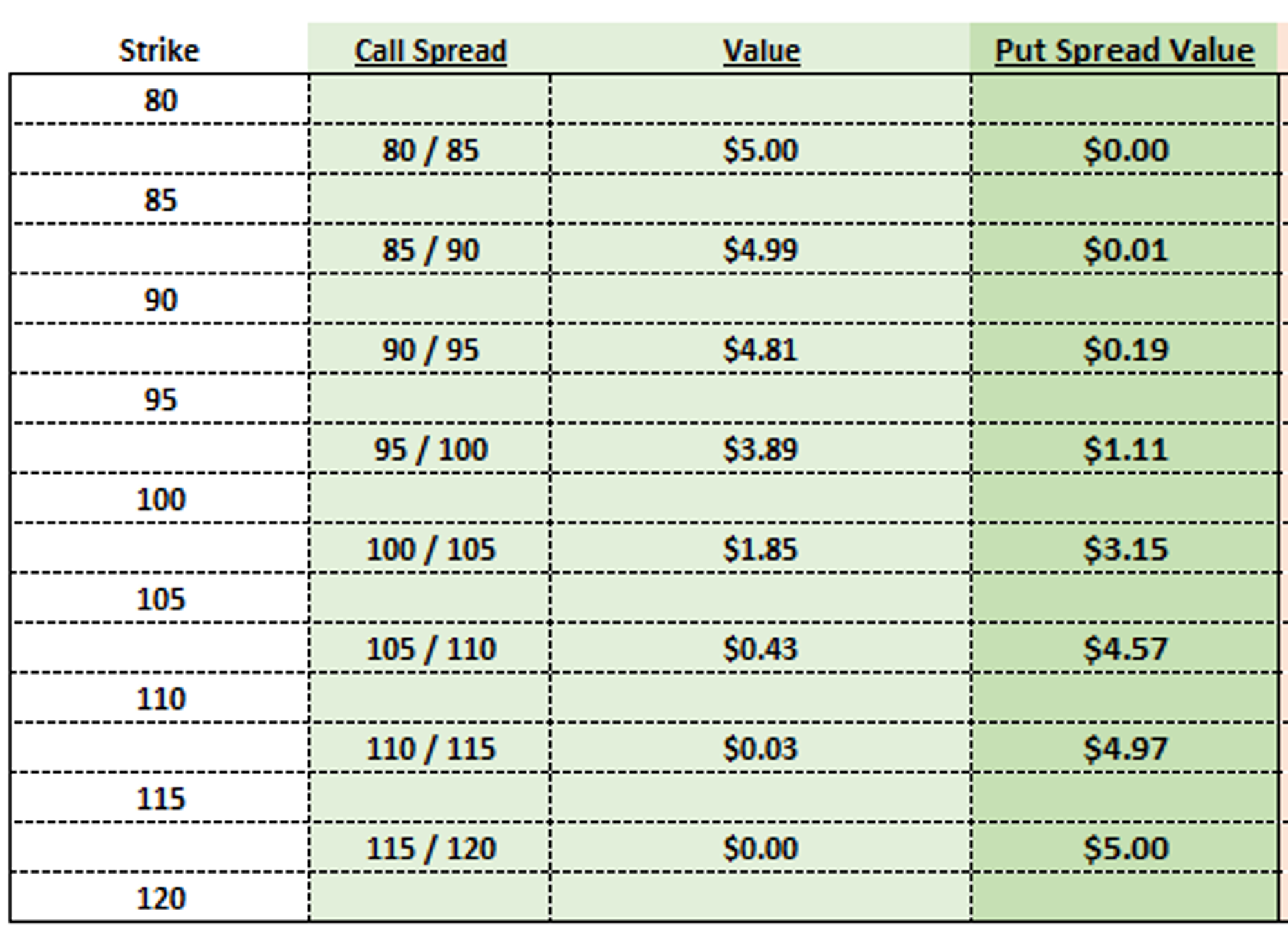

Using our option fair values from Part I, compute the value of the following call spreads:

80/85

85/90

90/95

95/100

100/105

105/110

110/115

115/120

Hint

Recall our option table:

So for example:

95 call = $6.19

100 call = $2.31

95/100 call spread = $3.89

Note that the most this call spread can be worth is $5 so the price implies that the stock will likely expire above $100. Which we know is true remember?

Answer

Without computing the values of the individual puts, price all the put spreads for the same strikes:

80/85

85/90

90/95

95/100

100/105

105/110

110/115

115/120

Hint

There’s a few ways to compute the value of the put spreads. You could compute the value of the puts numerically just as we did with the calls, but I said not to do that.

What else can you do?

You could use put-call parity to compute the value of the puts then compute the spreads.

But there’s an even faster way.

You can realize that the value of a put spread must be equal to:

The difference between the strikes - the value of the call spread

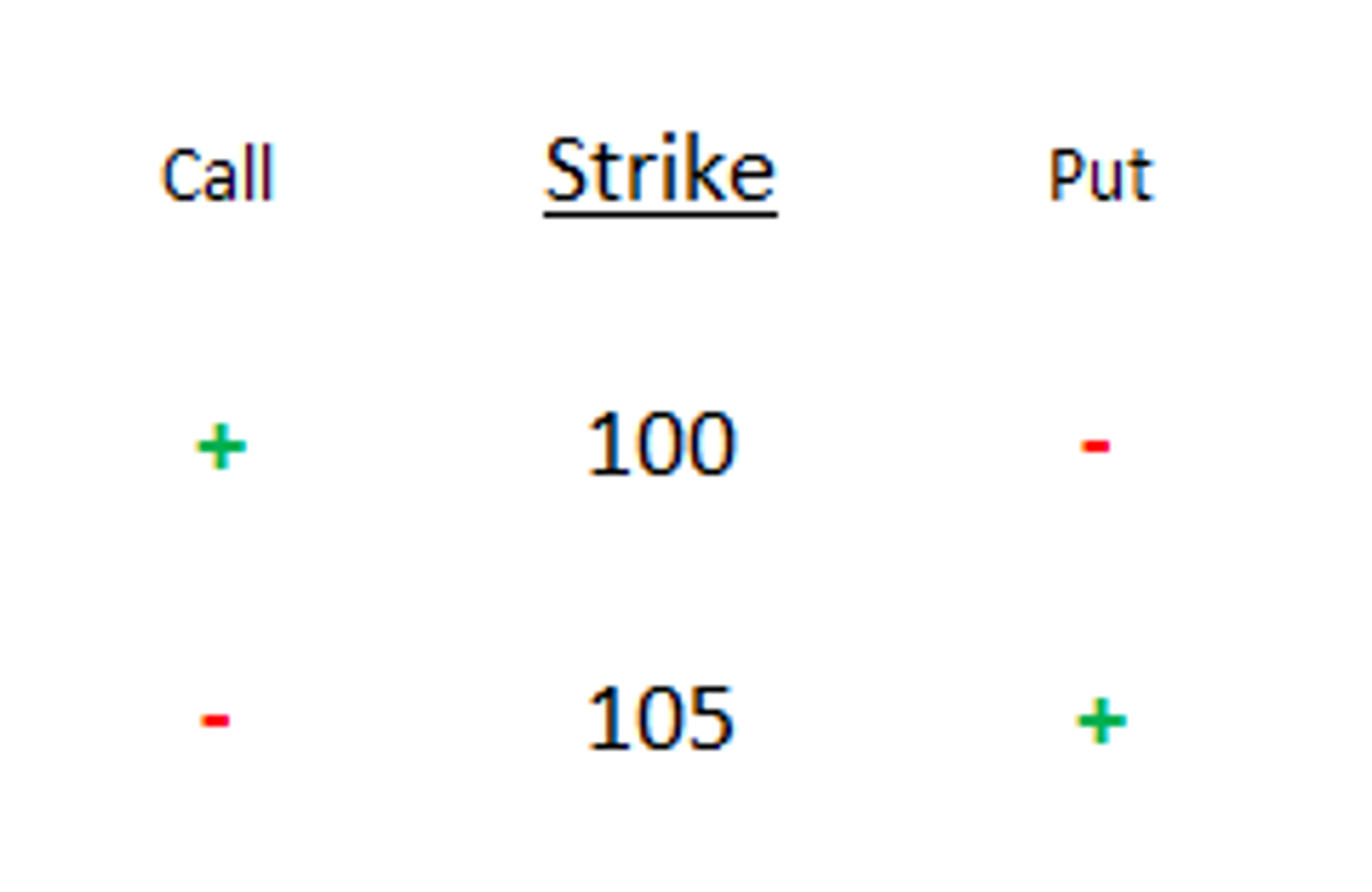

To see why, consider the following structures:

Long the 100 call, short the 100 put

No matter what happens at expiration, you will be buying the stock for $100.

If the stock expires above $100, you will exercise the call

If the stock expires below $100, you will be assigned on the put

This position acts exactly like a long stock position and in fact is often referred to as “synthetic stock” or “combo”.

Let’s consider the opposite position on another strike.

Short the 105 call, long the 105 put

This is short synthetic stock. No matter what happens, at expiry you will be short the stock at $105. You are short the 105 “combo”.

Ok, combining these ideas:

Long the 100 combo

Short the 105 combo

Net result: At expiry, you will buy the stock for $100 and sell it at $105.

This structure is known as a “box”

Of course, if you expect to make $5 profit on expiration, in a world where there is no free money, you can expect this structure to cost you the present value of $5 today.

A word on “boxes”

More advanced readers may have heard about SPX boxes as an alternative to T-bills.

Can you see why?

You are buying something for less than $5 that will be worth $5 on expiration. The discount implies an interest rate and in fact that rate will be closely tied to the Fed Funds rate.

Buying a box is like investing in a bond or lending money!

I can see you wondering “Kris, what the heck does this have to do with put spreads?”

Look at the picture again.

A box can be decomposed into:

Long the 100/105 call spread

+

Long the 105/100 put spread

The sum of these structures must equal the value of the box which equals the distance between the strikes!

Caveat

Technically the box is worth the present value of the difference between the strikes but we assumed zero carry costs.

This is only strictly true for European style options — American style options include early exercise premiums in their values and this can alter the price of boxes

Re-arranging: Box - Call Spread = Put Spread

In our example, the 100/105 call spread is worth $1.85.

Box - Call Spread = Put Spread

$5 - $1.85 = $3.15 = 105/100 put spread

You can use this identity to price all the put spreads simply from knowing the call spreads!

A word on arbitrage relationships

This material is standard curriculum in the first week at a option market0making outfit. It is an example of an arbitrage relationship.

When you buy a call spread, it is synthetically equivalent to selling the corresponding put spread. Just think of the cash flows.

If I buy the 100/105 call spread for $3.15 and the stock goes to $110, I will make a $1.85 profit because the call spread will expire worth $5.

If I sell the 105/100 put spread at $1.85, I will pocket the whole premium if the stock goes to $110.

My p/l is the same in both scenarios.

I’ll leave it to the interested reader to test the rest of the scenarios to their satisfaction.

Answer

Butterflies are usually defined in a confusing manner. For example:

Long 90 strike

Short 95 strike 2x

Long 100 strike

(The value of call butterflies and put butterflies are the same because of the box relationships derived in the prior hint)

But there’s an easier way to view butterflies: a spread of spreads.

It’s the lower call spread minus the higher call spread. If the 90/95 call spread is a bet on the stock expiring say above $92.5, the 90/95/100 butterfly, is like a bet that the stock will finish above $92.5 but below $97.5.

The maximum value of the butterfly occurs at $95 where the call spread you are long is worth $5 and 95/100 call spread you are short expires worth less. The butterfly’s maximum value is $5!

If the stock expires at $100, both call spreads are worth $5 and therefore the butterfly or spread of call spreads is worthless ($5 - $5 = $0).

If the stock expires at $90, both call spreads are worthless. $0 - $0 = $0. The butterfly is, again, worthless.

So a butterfly is just a bet on a narrow part of the distribution with well-tamed risk and reward.

On to the question:

Price the following butterflies:

80/85/90

85/90/95

90/95/100

95/100/105

100/105/110

105/110/115

11/115/120

You can use all call spreads or call put spreads but don’t mix and match.

Answer

Here’s the full table:

Part III: Reasoning About Strategies and Extraplolating To Decision-Making In General

This tutorial was a response to a reader who wanted to know if their butterfly selling strategy was sound.

We built a simple binomial stock model to underpin pricing for calls, puts and vertical spreads. Ideally this exercise, should have helped the reader to isolate what types of questions they to consider to hone in on their ultimate question: “Does selling butterflies make sense?”

If those questions remain hard to infer then hopefully the subsequent Socratic discussion will help. The flow of the questions should be helpful to anyone engaged in a repeated strategy.

✳️

The risk and reward of vertical spreads and butterflys

Refer to these table as needed:

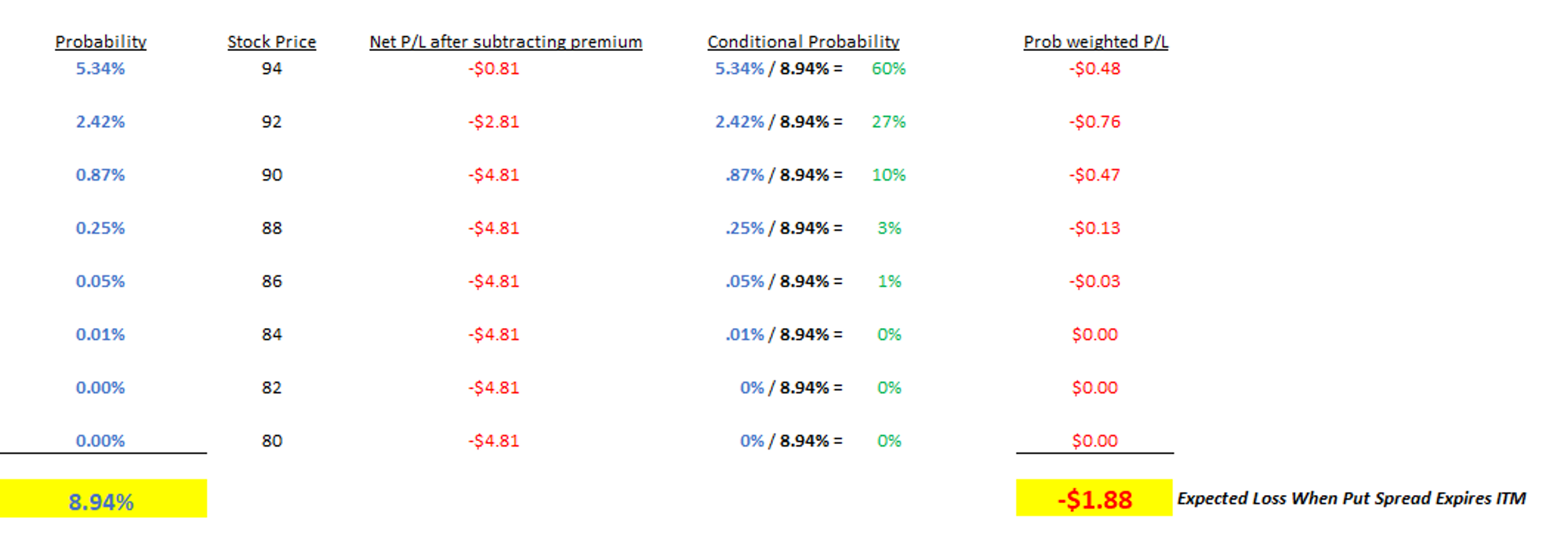

When you sell the 95/90 put spread, how often do you lose?

Answer

You collect $.19 in premium to sell that put spread.

It’s in-the-money when the stock expires below $95 so we can refer to our discrete distribution to see how often this occurs.

You lose about 9% of the time.

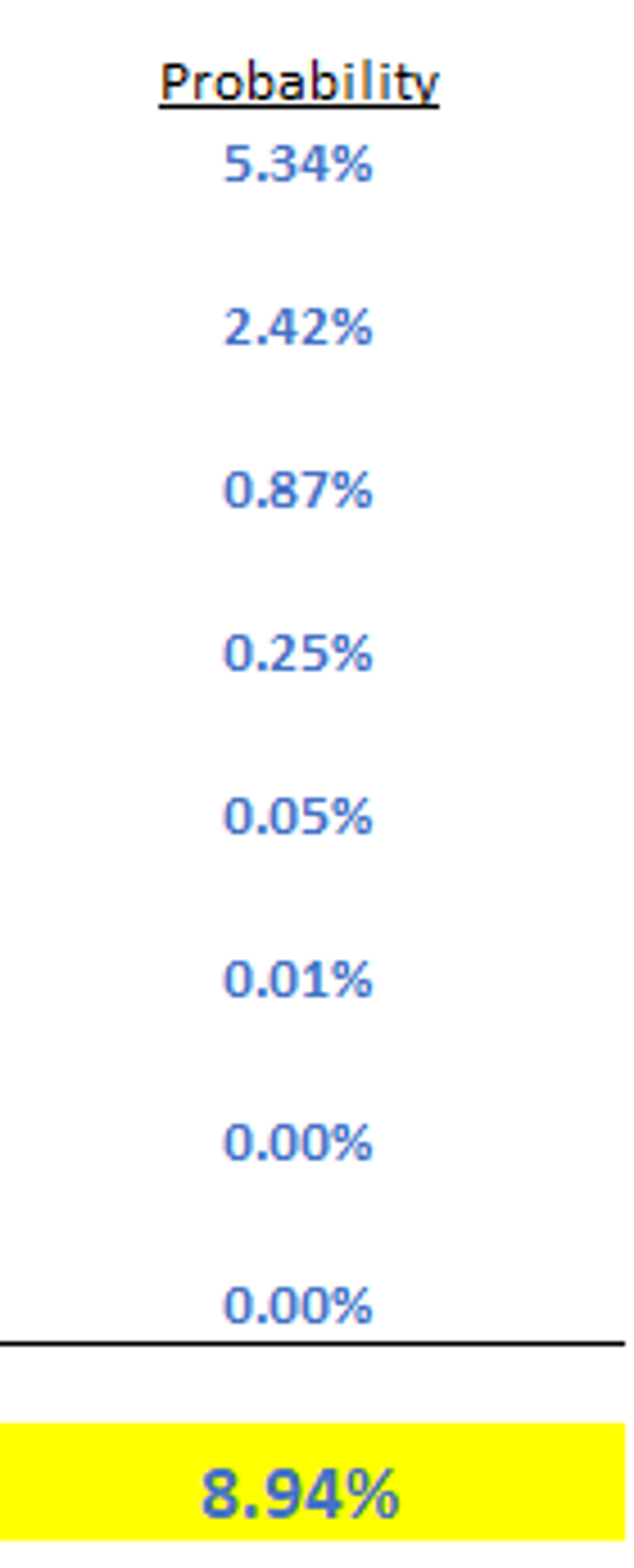

How much do you expect to lose when the put spread expires in-the-money?

Answer and discussion

This is a conditional probability questions and can be solved as such:

On average when you lose, you expect to lose $1.88

Or about 10x the premium you collect when you win.

🗨️

Discussion

Note this is a fair proposition. You expect to win 9% of the time or 10 out of 11 trades. When you lose, you expect to lose 10x the premium.

You are laying 10-1 which is the fair odds for this proposition.

Another framing:

If you trade at fair value, a full year’s profit will be wiped out by one month. And this is what you should expect.

Observations and questions you should notice:

Why you should resist the seduction of high hit rate strategies

If a strategy has a high hit rate, it is operating on a highly skewed trade.

Your high hit ratio tells you nothing about whether this strategy is profitable in the economic sense of the word. It takes a very long time/large sample to learn anything about how well you calibrated on low probability events.

If something you believe to be a 1% probability is actually a 2% probability you are wrong by 100%. That will be reflected in the payoff space -- something that you are accepting 50-1 odds for should demand 100-1 odds.

If you insist on conflating positive expectancy with hit rates you could save yourself the headache and just run a martingale strategy in a casino. You'll have negative edge but you'll probably win and at least you'll get some free drinks and a hotel room.

I’m not arguing that you have negative expectancy on your skewed strategy, but the burden of proof is on you to prove otherwise and the point is that the more skewed the payoff of the strategy is the worse the epistemological foundation for your conclusions.

Which means you can never really push. And if you know today, that you are building a strategy you can’t push too hard, then the question is it worth pursuing in the first place (it’s a bit meta but it feels like another tree with conditional probabilities at the nodes).

Compare the 100/95 put spread to the 100/105 call spread. What are your impressions?

Discussion

The 100/95 put spread is worth $1.11

The 100/105 call spread is worth $1.85

Observations

The stock is trading $100 but the call spread that optically appears to be equidistant to the put spread is worth 66% more. We understand why — the stock’s expected value at expiration is $101.

But the fact that option prices don’t “look right” is a clue that dissonant intuition should lead you to ask “What does the market understand that I don’t?”

In this case, the extra premium in the 100/105 call spread relative to the optically equal 100/95 put spread is not edge?

The fact that options have premiums is not necessarily an edge — the question you need to ask is if the premium is fair, high or low. Premiums imply a distribution, you need to ask why the implied distribution is wrong.

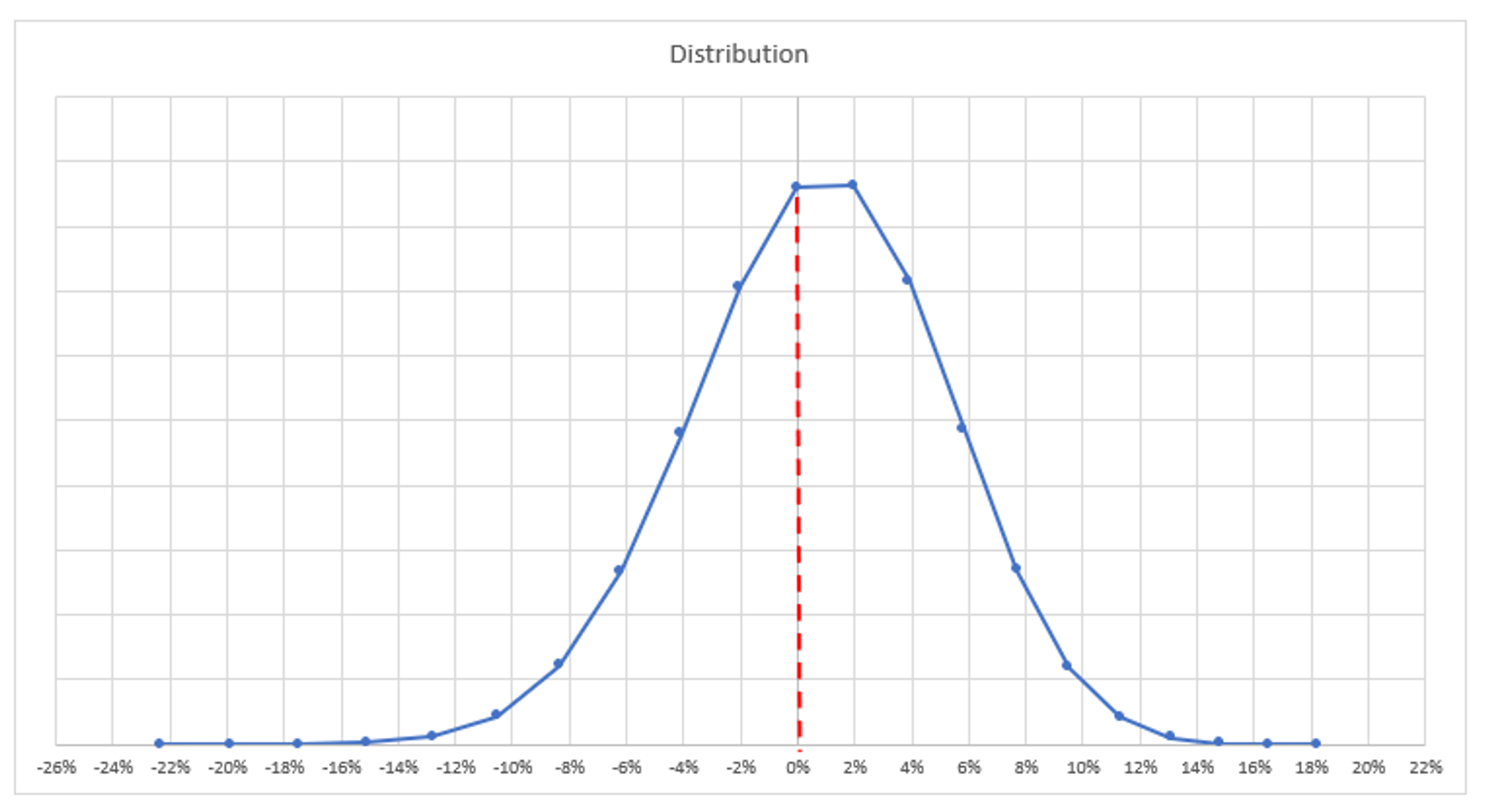

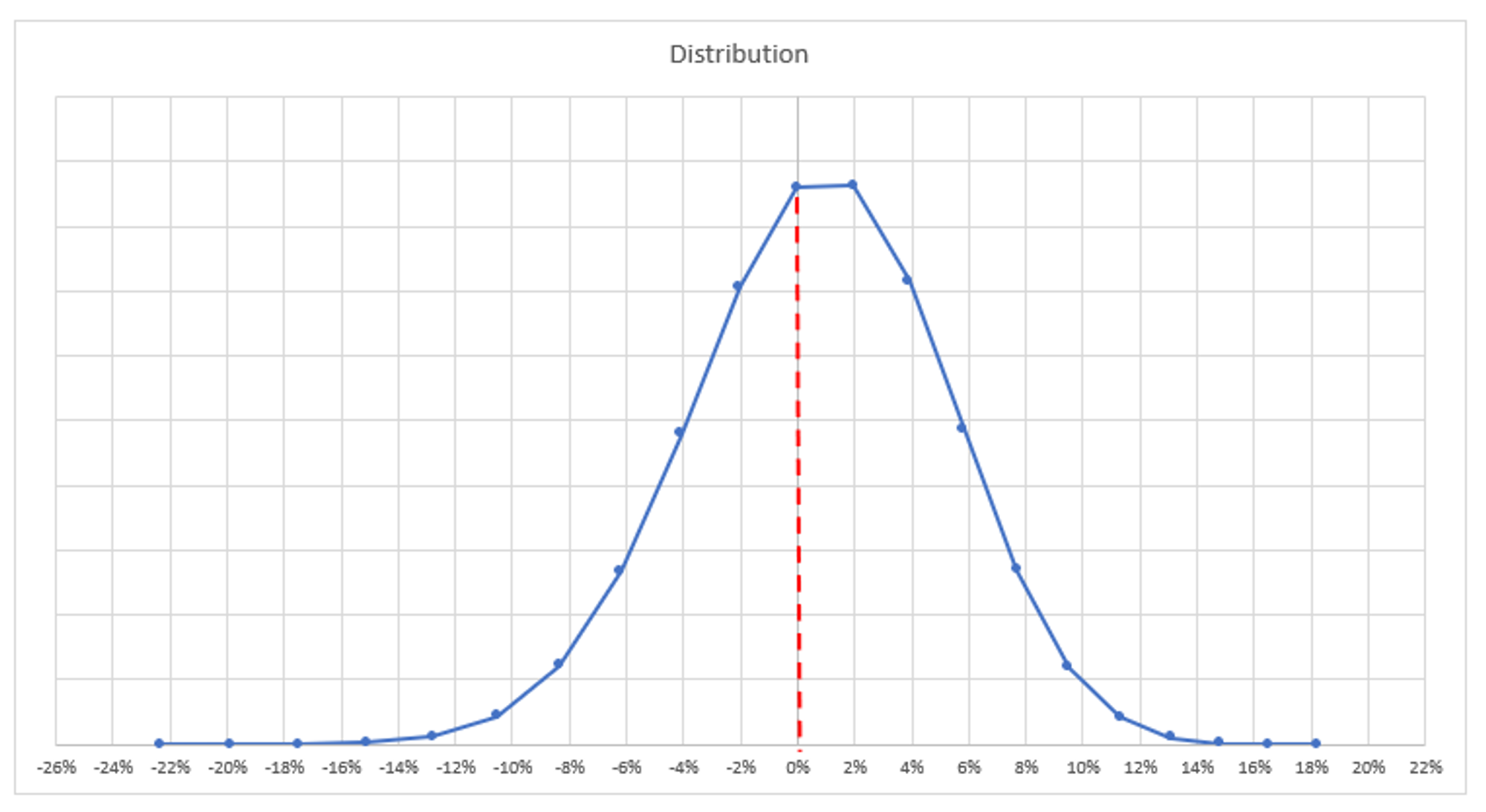

I did something subtle or jarring depending how much experience you have with thinking about stock distributions. Instead of specifying how much percent the stock moves per day (ie volatility), I had the stock move a fixed dollar amount.

This has the effect of making the stock have a higher volatility as it falls and lower volatility as it rallies. In other words, it creates real-world looking skew when viewed in log return space.

The skew can be seen in this histogram — the peak is shifted to the right and the left tails has more mass than the right tail.

I added this feature because the reader who reached out to me used the:

”I’m selling downside because the market drifts upwards”

By having this exercise mimic this idea by biasing the coin probability to the upside then pricing the spreads we can see that the market is already assigning a lower probability to the downside

In real-life Implied skew makes the put spreads worth less; this exercise kluges that. So when you sell those put spreads using “markets go up” logic you are doing the same thing as someone bets on the Nuggets because they’ll probably win — brah, it’s already in the price. Your job is to find out why the price is wrong.

If you use options to hedge or invest, check out themoontower.ai option trading analytics platform