The size of the risk premium in an asset is proportional to the divergence between the risk-neutral embedded in the price and the real-world probability.

It follows then that this lens can help you reason about whether an asset is cheap or expensive!

If risk premiums imply risk-neutral probabilities that do not align with real-world probabilities then:

The business of trading is arbing risk-neutral probabilities that disagree

Risk-neutral probabilities are the fair (not real-world) probabilities. They are fair because they are the probabilities implied by a well-priced game for which there is no excess return per unit of risk.

Traders measure what’s implied in markets by comparing normalized prices. They find disagreements in what’s implied and construct portfolios that offset these disagreements in ways such that their profits converge to the difference between the disagreements regardless of what actually happens in the real-world.

This is a business

Trading positions are not investments. They are the outputs a business process. Trading is a business in the same sense as Dunkin’ opening early every morning to make the donuts.

[While the trades themselves are not a business, one could invest in the business of trading just as one can invest in the abstraction known as a donut shop]

Speculation is disagreeing with the probabilities on an absolute basis

The distinction between trading and speculation can sometimes be blurred. A trader is a bookie trying to balance bets around a fair betting line. A speculator is the bookie who maintains an unbalanced line because they find actuarial value in opposing one side of the proposition with their own capital.

🌙

Personal example of the blurry distinction

I used to do relative value arbitrage between options on ETFs vs futures… but i also had signals.

Even though a price of X was “market fair”, i might be a buyer for X because it had edge to my proprietary signal — if someone paid more than X, I’d sell a small amount because there was an arbitrage profit, but I’d try to keep my exposure or position targets leaning in the direction of my signal.

My opinion of price X also had a Bayesian component.

Suppose I’m accumulating a position at price X and now someone was now paying more than X AND I thought this was a “liquidity clearing level” — meaning they had size to buy.

[They are also likely to be vol smart in the sense that they are seeing what my signal saw…this is more common than you think — if you are in a seat that sees lots of activity you will have a better sense of fair value than others. Your assessment of a good trade is going to correlate strongly with other traders who pay close attention to flows. Large market makers usually agree.]

At that point I probably wouldn’t sell this new buyer anything as I now believe that market fair is going higher, closer to my “signal fair”, and the old X will be the new bid. I might gain conviction, try to increase my long position because I got confirmation that I’m right and now it’s time to step on the gas.

I’m speculating within the context of a trading business.

We will focus on the speculator/investor.

As a speculator, ask yourself:

How much capital is willing to absorb the idiosyncratic risks of a particular investment?

This requires understanding:

the properties of the investment itself

Some of the concerns include:

how correlated it is to other assets?

what are its return possibilities?

how accessible /transparent is it?

the structural supply of available capital

Some of the concerns include:

are particular investments in/out of favor creating too much or too little risk dollars willing to underwrite the idiosyncratic risks

how much capital has ESG concerns?

is there a vanity bonus for owning the asset?

Think sports teams. The highest bidder is the one who gets the most psychic benefits — the return math should not pencil out on an ex-ante basis.

⚽

A side note

The owners of MLS team Inter Miami understood the value of bringing Lionel Messi in as an owner. Buying into the franchise (in the form of forgone wages) allowed Messi to be a higher strategic bidder than any possible partner because of how much value he could idiosyncratically bring to the franchise

Or something more relatable — angel investing. Byrne Hobart points to Alex Danco’s conjecture that angel investing is mostly about bragging rights. this only needs to be partially true, to destroy the risk-adjusted returns for early investors.

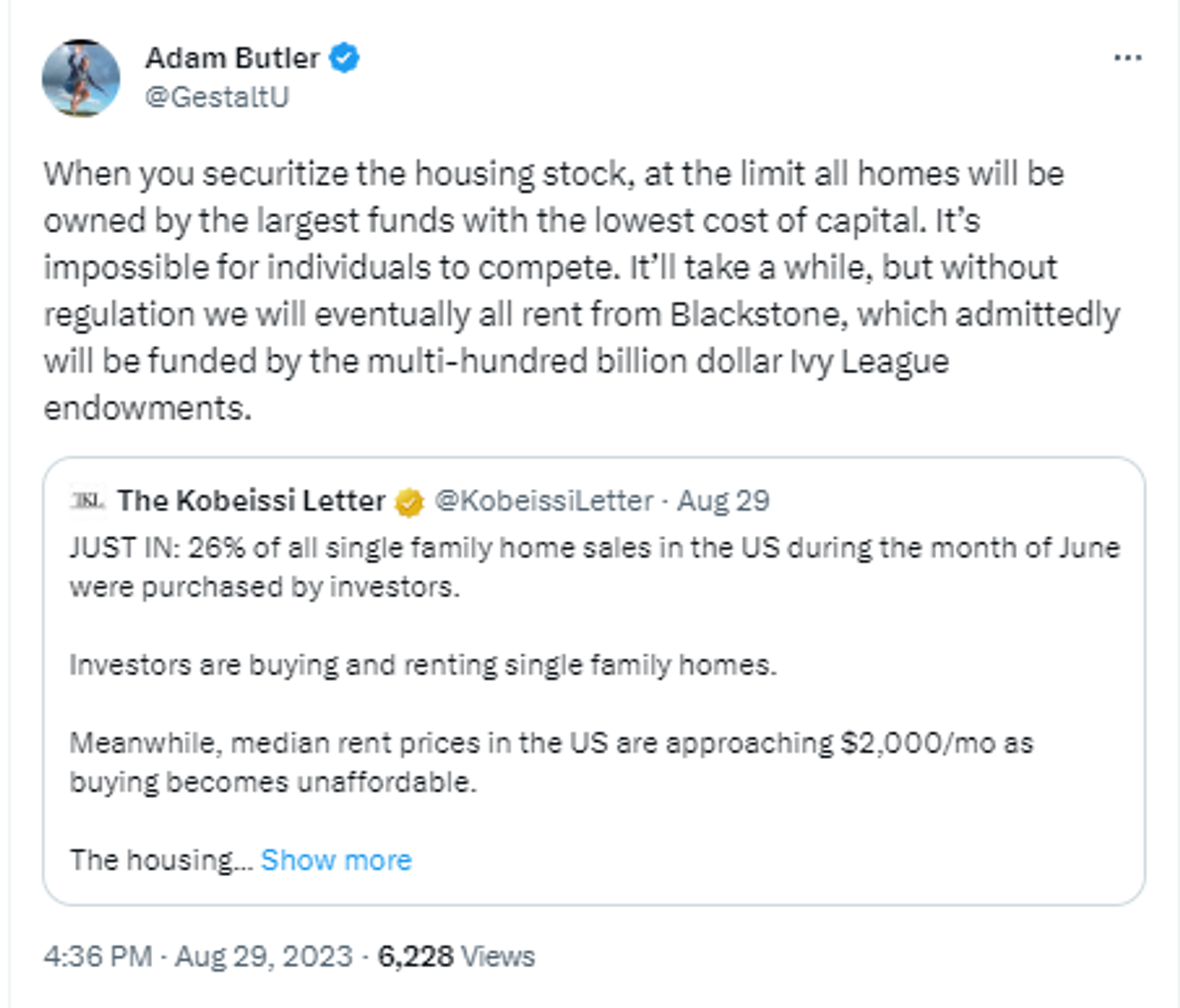

Large bankrolls and diversification are both risk absorption mechanisms that boost asset prices in turn boosting risk-neutral probabilities, sometimes independent of the real-world probabilities. In other words, idiosyncratic risks are underwritten by lower required rates of return than you might expect.

The more risk you can absorb, the closer your bid approaches the risk-neutral price. You are forced to accept the proposition that the most optimistic bid is willing to accept. But since you have a different set of constraints (time horizon, cost of capital, next best alternative, emotional barometer, risk tolerance, tax status, and return on investing on yourself) then your personal efficient frontier is probably more conservative than the market’s consensus for assets that are widely accessible.

This suggests a low yield on extra effort to squeeze more out of investments you don’t have some privileged access to (and that access needs to be for a good reason that is usually strategic. “If you don’t know who the fish at the table is, then it’s you” would be useful admonition here but just like how everyone thinks they are an above-average driver, your level of self-awareness will vary how much mileage you get from the trope.

Implication

The vast majority of your time is best spent on skilling up your human capital. The flip side of lower required rates of return is a lower cost of capital for entrepreneurs!

When we bring these ideas together, we should default to the understanding that idiosyncratic risks that are:

easily diversified

easy to understand (like a coin flip) & derisked by bet sizing

do not offer much hope for superior risk-adjusted returns.

Buying rental properties off MLS, which everyone can see, and anyone can understand just looks like a poor use of time for someone simply interested in financial returns.

⚕️

Prescriptions For What You Should Do Based On This Knowledge

The Diversification Imperative

If you are not diversifying you need an argument for why you think you are paid for idiosyncratic risk. Otherwise, you're paying 50 cents for the coin flip game when you think your paying 33.

VCs diversify

They’ll be okay as long as they are sampling from a power-distributed return stream (narrator: most of them are probably not). When you play VC with your $5k check, you are paying the 50 cents or more and hoping. This is not an iron law but serves as a null hypothesis. You need a good argument as to why the null is wrong “this time”.

[The “tuition” rationalization might work for you if you want to ease back from the financial thesis]

Addressing “deworsification”

Someone always wants to bring up Buffet. Great. I can drink all the Gatorade I want, I’m not gonna be “like Mike”. There’s an astute observation that you concentrate to get rich and diversify to stay rich. Concentration is what you do every day with your life’s work. Your time is how you concentrate to get rich. Your savings/investments should be diversified.

Buffet’s life’s work is investing.

You’d be better off taking the advice of one his his most respected friends and early investors (and maybe the best risk-adjusted investor of all time) Ed Thorp. Ed strongly advocates diversification.

(Ed and Warren both recognized that the other is a genius when they had dinner in their late 30s.)

Diversification is the “you might not be a genius” hedge.

I could go on and on. Actually, I have.

Common heuristics

By understanding embedded distributions and probabilities you can reason about whether they are overpriced or not and why. Without necessarily quantifying these premiums you can find opportunities that fit your portfolio OR invite caution into what you used to suspect was an opportunity.

Who would you expect to be the best bid?

Builders and real estate developers require a financial margin to buy land and won’t pay as much as the individual whose bid comes wrapped with the mental image of her family sitting around their dream fireplace

For similar reasons, commercial real estate will trade at more attractive cap rates than single-family homes

Winners Curse

In options, when someone blows out their clearing firm auctions off the portfolio. The best bid for the portfolio will be the firm best suited to manage the risk. As such, before bidding on liquidation portfolios trading firms consider the competitive landscape to handicap: “how much edge did I get on this block trade conditional on winning the bid?”

Because everything has a price, and auction winners often overshoot it.

We live in a world on auction. Photographs have been auctioned for $5 million, watches for $25 million, cars for $50 million, and (thanks to the advent of non-fungible tokens) jpegs for $69 million. Google auctions off ads on search terms, the US government auctions off bands of the electromagnetic spectrum, and in 2017, a painting of Jesus crossing his fingers fetched $450 million at auction. Before we dub this the worst-ever use of half a billion dollars, remember two things: (1) The human race spent $528 million on tickets to The Boss Baby, and (2) it's a notorious truth about auctions that the winner often overpays.

Why does this winner's curse exist? After all, under the right conditions, we're pretty sharp at estimation. Case in point: In the early history of statistics, 787 people at a county fair attempted to guess the weight of an ox. These were not oxen experts. They were not master weight guessers. They were ordinary, fair going folks. Yet somehow their average guess (1,207 pounds) came within 1% of the truth (1,198 pounds). Impressive stuff. Did you catch the key word, though? Average. Individual guesses landed all over the map, some wildly high, some absurdly low. It took aggregating the data into a single numerical average to reveal the wisdom of the crowd.

[Kris: From Superforcasting]

How The Wisdom of Crowds Works

Bits of useful and useless information are distributed throughout a crowd. The useful information all points to a reasonably accurate consensus while the useless information sometimes overshoots and sometime undershoots but critically…cancels out.

Aggregation works best when the people making judgments have a lot of knowledge about many things.

Aggregations of aggregations or “polls of polls” can also yield impressive results. That's how foxes think. They pull together information from diverse sources. The metaphor Tetlock uses is they see with a multi-faceted dragonfly's eye.

Now, when you bid at an auction — specifically, on an item desired for its exchange value not for sentimental or personal reasons — you are in effect estimating its value. So is every other bidder. Thus, the true value ought to fall pretty close to the average bid.Here's the thing: Average bids don't win. Items go to the highest bidder, at a price of $1 more than whatever the second highest bidder was willing to pay. The second-highest bidder probably overbid, just as the second-highest guesser probably overestimated the ox's weight.

To be sure, not all winners are cursed. In many cases, your bid isn't an estimate of an unknown value but a declaration of the item's personal value to you. In that light, the winner is simply the one who values the item most highly. No curse there.

But other occasions come much closer to Caveat Emptor: The item has a single true value which no one knows precisely and everyone is trying to estimate.

[Kris: In Recipe For Overpaying I note investor Chris Schindler's intuitive explanation for why high volatility assets exhibit lower forward returns: a large dispersion of opinion leads to overpaying. He points to private markets where you cannot short a company. The most optimistic opinion of a company’s prospects will set the price.]

Line-Item Myopia

On a stand-alone basis you expect commodities to be overpriced. Why?

Because of their diversification value at the portfolio level.

The CFA did a comprehensive study of commodity returns and a key finding was:

Commodities do especially well during periods of inflation with the attribution due to spot returns. In fact, this is considered a potential reason why commodities offer lower expected returns than stocks. There is less compensation required because you are receiving a high inflation hedge.

In other words, the standalone benefits of investing in commodities are absent. Unless you are diversifying them with other investments you are losing. Likewise, someone investing in stocks can afford to pay more for them theoretically if they have diversifying exposures in commodities. (Unfortunately the source link to the study from my notes is dead)

This is a real-world example of the sun/rain principle.

Bonus for technically-minded investors: Difficulty with extraction

Extracting a risk-neutral probability from an option surface is not rocket surgery. But extracting probabilities from prices can is heavily laden with judgment when you start sharpening your pencil.

It’s like trying to shoot a moving bullseye while standing on a moving platform.

Examples:

Risk arbitrage

A stock is being taken over for $100 cash. The deal is expected to close in 1 year. The risk-free rate is 10%.

If it’s trading for $91.91 or $100/1.10 you might say it’s 100% to close. But what if there’s some expectation that another bidder will come in higher in the next week? What if the first deal breaks, how far do you expect the stock to fall? Back to the pre-announcement price or is the floor higher now that a higher bid has been shown? What if the deal broker because the bidder found something fishy in the “discovery” process?

And this is for a simple cash takeover.

There can be all kinds of complicated cash/stock hybrid deals where investors are electing to tender shares, pro-rata allocations, and so on. And the options markets allow you to extract increasingly fine-tuned statements about what the market is saying (if a cash takeover closes, all extrinsic option value above the deal strike goes to zero — what does a LEAP straddle value tell you about about the market’s consensus probabilities?)

This is not my wheelhouse (most of my career was in futures options) although I’ve been in the room with traders trying to parse what the prices mean.

So when I hear people’s opinions about deal stocks I’m often chuckling inside when I’m pretty confident they don’t understand what the point spreads are even implying.

Breakeven Inflation

The spread between inflation-adjusted and nominal bonds can be used to compute an “implied breakeven inflation”. But the TIPs market is small relative to the broader bond market. And inflation is a systemic risk that is notoriously difficult to hedge. This is a classic case of “I don’t expect the implied probability a remotely unbiased predictor of real-world probability”

This paper, which I have not read, does go into the extraction of breakevens.

Implied Correlation

If you are familiar with the option strategy of dispersion trading you know about implied correlations. You may also have a clue that the implied value is also not an unbiased predictor of realized correlations.

You should actually expect that it inherits a similar risk premium as SP500 puts which is the undiversifiable preference for not having a concave exposure to a large-scale risk-off drawdown.

Colin Bennet explains that implied correlation, which has a convex payoff, trades at a premium to linearly settled correlation swaps. It has to do with the fact that implied volatility is itself correlated to correlations.

[Narrator: there is much better ways to make money in life than options brain damage. If you are this deep into the dropdowns of this post I’ll leave virtual flowers on your LinkedIn grave when you retire]