This lesson will build an understanding of risk-neutral probability and why it’s such an important concept in reasoning about the value of investments.

Through a progression of questions, you will develop an intuition for the concept. From that base of understanding, you will be able to make novel interpretations of what asset prices imply.

This is a key skill in being able to identify assets that “disagree” with each other — a disconnect that may signal opportunity.

🧗🏾

A step-by-step progression

Imagine a game that pays:

$1 if a coin comes up heads

$0 if the coin comes up tails

The coin will be flipped immediately.

What is the expected value of the game?

Answer

(50% x $1) + (50% x $0) = $.50

On average the game pays out 50 cents.

How much would you pay to play this game?

Answer

While a range of answers is acceptable, unless you like losing money on average or are especially risk-seeking none of the answers should exceed $.50.

If you were willing to pay exactly $.50, you will gamble for zero expectancy. We could say you are risk-neutral.

If you want to make a profit, on average, you’d be willing to pay $.49 or less. How much less would depend on how risk-averse you are but since we are only talking about one dollar of risk, I suspect you’d be willing to pay pretty close to $.50.

Don’t dwell on this too much, we’re just establishing a basic vocabulary.

Let’s add an obstacle.

Suppose you have to pay to play today, but the coin won’t be flipped for a year. Your money will be held in escrow.

It helps to imagine that the amount of money is meaningful but if you lost it you’d be ok. Without peering into your soul, I’ll just pick something arbitrary. Let’s say you’re making $100k/yr of net income and heads pays out $1,000 and tails nothing.

3. How much would you pay to invest?

[Look at you noticing how we switched the word from “play” to “invest”.]

Answer

Like the last question, a range of answers is reasonable but for “homo economicus” acceptable answers need to be “less than $500”.

But the best answers will have an even lower ceiling than $500. (I’ll give you an extra second — phrases like “less than an even lower ceiling” don’t compile at the speed of sight).

The lower ceiling than $500 depends on a simple question:

Are you earning interest on the cash in escrow?

Suppose you are not.

Let’s suppose further that your FDIC-insured bank is offering a 10% CD.

What is the absolute most you’d pay to invest in this proposition that in 1 year pays $1000 if heads or $0 if tails?

Answer: $454.55

Why?

Because if you deposit $454.55 in the bank you’ll end up with $500 in a year without any risk.

Of course, you’d only pay $454.55 if you were risk-neutral.

Depending how risk-averse you are, your maximum bid would likely be less than $454.55

🏕️

Risk Neutral Probability

It may have felt like an easy stroll so far but I have great news — you’ve climbed to base camp. You’ve discovered a foundational investing concept called risk-neutral probability.

You might not recognize it just yet, but let’s recap what you’ve done:

You have discounted a future cash flow to establish a bogey or benchmark for what a riskless investment should return.

Let’s conjugate that statement differently to internalize an action that smart investors constantly do:

You discount possible outcomes to present value using a riskless rate.

Once you have discounted the outcomes to present value with the riskless rate, you are now able to back out the implied probabilities of those outcomes.

In other words — we are answering the previous questions in reverse! By observing the price being paid today relative to the present value of the outcomes, we are solving for the probability of getting heads.

This is important because most propositions we care about are not coin flips where we know the probabilities.

We need to listen to the probabilities that the prices whisper.

Practice

The best way to understand this idea is by example. Let’s do more questions.

Assumptions:

The US presidential election will settle in exactly 1 year

The risk-free rate is 0%

Futures contracts on PredictIt.org settle to $1 if true, $0 if false

If you buy a futures contract on PredictIt. org you post the full amount of the contract (ie no margin)

As I write this, PredictIt.org shows Trump trading for $.63 to be the Republican nominee. What’s the implied probability of Trump winning the Republican nomination?

Answer

This looks just like the coin flip example except someone is willing to pay $.63 to play the game.

The implied probability is simply 63%.

Because there’s no riskless opportunity cost for tying your money up at PredictIt.org this is also the risk-neutral probability.

Note, that this is not a real-world probability. That is, of course, unknowable.

Now assume the risk-free rate is 5%. We’ll repeat the question — $.63 implies what probability of Trump winning the Republican nomination?

Answer

The key difference is we need to discount the payoffs to present value by the risk-free rate.

Discounted win payoff = $1.00/1.05% = $.9524

Discounted loss payoff = $0/1.05% = $0

We can now think of this in present value terms.

The coin is paying $95.24 when Trump wins and $0 when he loses.

The market is paying $.63 in dollars for this proposition.

[Note how all the dollars are now being compared in present values.]

$.63 /$.9524 = 66.2%

The implied probability is 66.2%.

Because this incorporates the riskless opportunity cost we can also say this is the implied risk-neutral probability.

Again, not a real-world probability.

If it’s confusing why the probability went up, you can mechanically see that it must once we discount the payoffs to present value.

But, this might be unsatisfying.

An easier way to see it is to think of an extreme case — imagine the risk-free rate is 50%

In that world, you can simply deposit $.666 in the bank and get back $1 in a year.

So for you to pay $.63 for the Trump contract means you are super confident he wins the nomination.

[.63/.666 = 94.5% is the implied probability in this case]

As I write, empirestakes.com shows Trump to have a 31% chance of winning the presidential election.

Let’s revert to the 0% risk-free rate world.

If Trump is 63% to win the Republican nomination and 31% to win the presidential election, what is the implied probability he beats the Democratic nominee providing he’s won the Republican nomination?

Answer

Trump's 31% chance to win the presidential election is the joint probability that he:

a) wins the Republican nomination

b) beats the Democratic or 3rd party nominee

First, we can ignore a 3rd party nominee since the implied probability of that is 0%.

A joint probability means both events must happen so we multiply the probabilities together.

The key insight

Risk-neutral probabilities are the probabilities that imply no arbitrage

🧠

Advanced Topic: Replication

You might recognize the topic of risk-neutral probability from the options pricing world. It is a load-bearing concept underpinning replication.

Replication is the foundation of no-arbitrage derivatives pricing.

A comprehensive walk-through of option replication and Black-Scholes is out of scope for this post (and also not playing to my strengths as a teacher here). However, you are about to learn:

A common misunderstanding even amongst derivatives traders

An asset price is like a star being viewed from 2 parallel worlds — a risk-neutral one and a real-world one. The one you are viewing from determines your probabilities and ultimately your sense of value. This creates opportunities to trade. That’s what makes a market.

If you ventured into the advanced replication topics, you learned a neat bit of financial theory:

If there is an arbitrage that allows you to risklessly replicate another asset or derivative, then you should not expect to earn more than the risk-free rate. If you could then someone would buy the mispriced asset, offset its risk via replication, and earn more than the risk-free rate for a portfolio that is neutralized from risk.

That idea is an instance of a broader principle:

A proposition that has no risk, should not earn more than the risk-free rate.

Replication is not the only way to de-risk. There are 2 major ways that you are already familiar with.

We can demonstrate them by staying with simple examples.

Ways to absorb risk

Keeping your bet sizes small relative to your capital

Go back to the $1 coin game. If I offered you a chance to play it for $.49 you’d probably take it. You don’t need a lot of edge to risk 49 cents.

However, if I required you to play for $1mm, you might not pay $490k to play unless you are Ken Griffin.

But if you had $10mm, you would play for say $250k. You’d have a 50% chance of turning $250k into $1mm.

[Note: You’re getting 3-1 odds implying a 25% chance of victory for something we know has a 50% chance of victory]

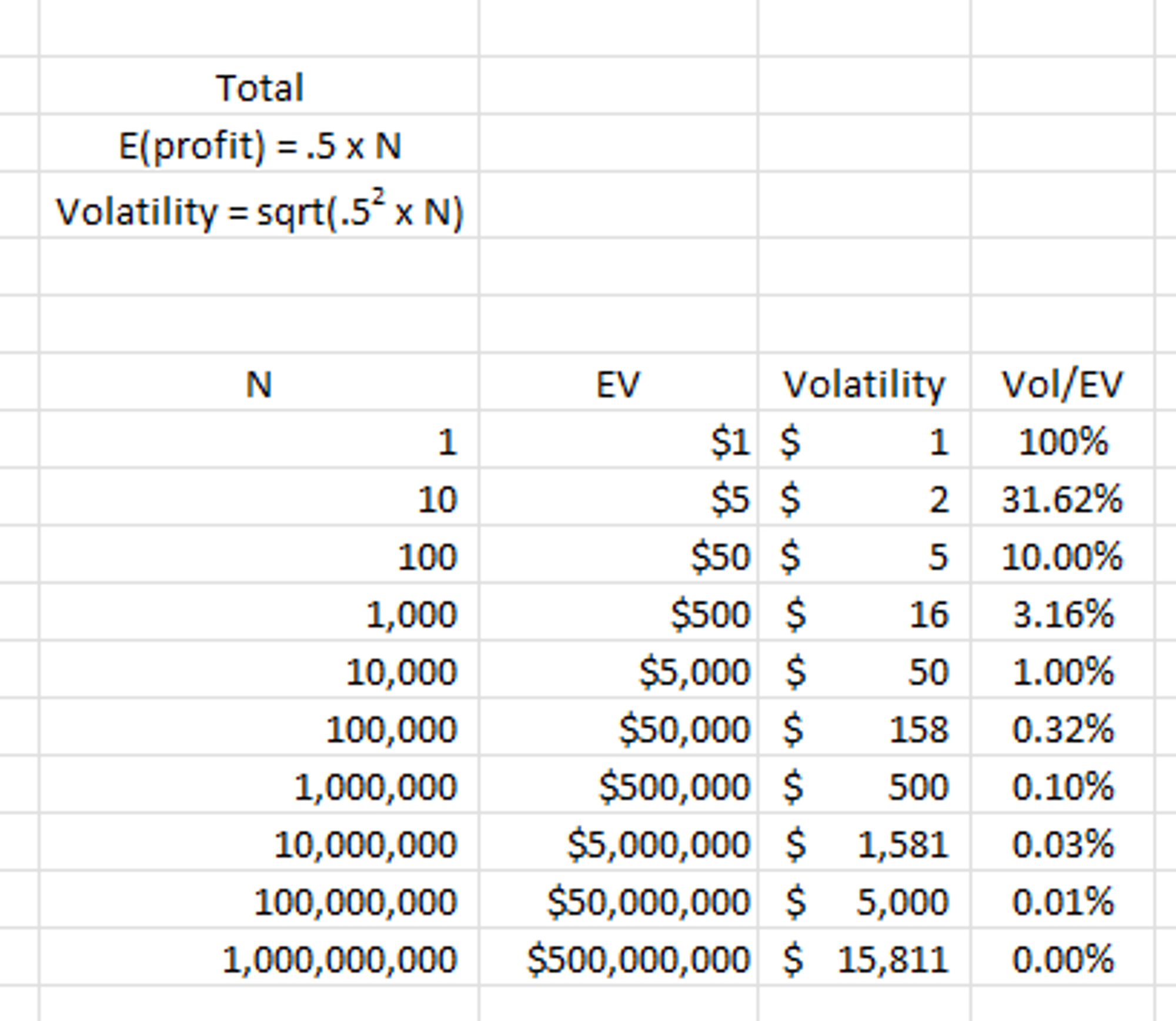

Let’s suppose this game was available to the whole world to play. What price do you think it would clear at?

My guess

Pretty damn close to its fair price discounted to present value. If the risk-free rate is 0% and the payoff is settled 1 year into the future I think it would trade extremely close to $.50

If you played the game 1 billion times in a row (assume it takes no effort to play), there would be nearly 0 deviation from breaking even in expectancy.

In the presence of a risk-free rate, I’d expect the game to trade at the same discount as a T-bill of the same duration.

Why?

Because if you play enough times the game is nearly riskless, so as long as someone out there has a giant bankroll, they would be happy to swoop in to play if it traded any cheaper than a T-bill.

The largest bankroll is able to absorb the most variance. This in turn allows them to be the best bid.

☀️Sunblock stock (SUN) makes 10% in sunny year. Loses 2% in rainy year.

☂️Umbrella stock (RAIN) loses 2% in sunny year. Makes 2% in rainy year.

Assume:

The year is 50% to be sunny.

The risk-free rate is 0%

Is this possible?

If these were true statements and everyone could access these investments, then:

No.

This is an arbitrage.

You can put 50% into each stock and earn 4% in sunny years and 0% in rainy years for an EV of +2% on the portfolio

The source of the arbitrage is the -1 correlation between 2 assets that both have positive expected returns.

You should expect this portfolio to be bid up until the expected return of the portfolio is equal yield of the risk-free rate (in this case zero).

The key takeaway:

The more risk you can absorb, the closer your bid approaches the risk-neutral (ie arbitrage-free) price.

🌐

Tying It Altogether: Applications to Investing

⏮️

Recap

Asset prices imply risk-neutral probabilities

A risk-neutral probability can be thought of as a “fair value” or “consensus” probability. Just like how the odds embedded in a betting line imply how often we expect the favorite or underdog to win.

The process for extracting those odds vary on technical details and assumptions but the general intuition can be seen from:

prediction market examples

basic derivatives replication (ie binomial trees to price options)

A risk-neutral probability is not the same as a real-world probability

Most of us would prefer a sure $100 over an expectation of $100. That’s just basic risk-aversion.

Someone who is “risk-neutral” would be indifferent to the fairly priced but uncertain return stream compared to the guaranteed return stream.

Idiosyncratic risks can be diversified by large numbers of trials or by combining them in portfolios that contain uncorrelated risks. These risks can be absorbed by proper bet sizing or portfolio diversification, leaving only assets dominated by systematic risk to command a true risk premium.

The size of the risk premium in an asset is proportional to the divergence between the risk-neutral embedded in the price and the real-world probability.

Discussion

🏗️

Why did we slowly build all this theoretical scaffolding?

The 2 broad categories I generally file reasons under:

Instrumental reasons

This is the practical purpose for doing something. You read to learn.

This is the aesthetic or impressionistic reason to do something. You read because it’s satisfying.

Game designer, programmer, and general artistic polymath Raph Koster sees game-playing as a way to train your “systems thinking”. In other words, you gain an appreciative sense of how systems work as a byproduct of fulfilling the requirements to win a game.

Finding real world systems and abstracting them or boiling them down to their essence isn’t actually a very common skill. Games can teach people how to do this. The idea involves setting constraints, modeling real systems, and allowing people to experience them within a game context to understand them deeply. It provides an opportunity for individuals to experiment with these systems, unlike in real life where, for example, you only get one shot at lifetime earnings. Playing a game that emulates this system offers lessons. This is applicable to various scenarios, such as political engagement. There should be games that allow players to experiment with political engagement methods, helping them discern more effective strategies. This principle holds true in many areas. (Link)

I’ve pointed out specific examples of this in games over the years

Quacks is a bit like a deck builder. It’s known as a bag builder but with a don’t-bust-press-your-luck mechanic. To most of you, that means nothing but for the remaining, you should know this an outstanding game. It’s fun, and while seasoned gamers won’t like this necessarily, it has enough luck to allow a first grader to compete with an adult. I found myself thinking quite a bit about the value of the “options” (they’re actually chips representing ingredients in a potion recipe) in the game and their respective costs. The concepts of theta, volatility, and vega would be visible to someone with a finance background if they looked past the game skin. An engineer would see this game as a very pure simulation (most likely AI) based problem especially since the game has no trading interactions.

We must identify second-order effects. In the options world, the “greeks” are sensitivities. Delta is the option’s sensitivity to the underlying. Gamma is a second-order sensitivity that describes how an option’s delta changes with respect to the underlying.

But this topic is everywhere. If a company sells more widgets it makes more profit. But second-order effects mean attracting more competition or saturating a market. Every satisfied customer is one less customer that needs satisfying. So if I build a model of profitability based on units sold, when does the function inflect? When does opportunity fade into unsold inventory?

A fun way to think about second-order sensitivities is playing “engine builder” boardgames like Dominion or Wingspan where synergies between your cards lower the marginal costs of later actions2. In essence, the cards have gamma based on how you stack them. Every time I use a card it might increase my odds of winning by X. That’s the delta or “benefit per use”. But the delta itself increases with synergy, so as the game progresses, you get more delta or benefit/use ratio, from the same card

One of the reasons I like boardgames is they are filled with greeks. There are underlying economic or mathematical sensitivities that are obscured by a theme. Chess has a thin veneer of a war theme stretched over its abstraction. Other games like Settlers of Catan or Bohnanza (a trading game hiding under a bean farming theme) have more pronounced stories but as with any game, when you sit down you are trying to reduce the game to its hidden abstractions and mechanics.

The objective is to use the least resources (whether those are turns/actions, physical resources, money, etc) to maximize the value of your decisions. Mapping those values to a strategy to satisfy the win conditions is similar to investing or building a successful business as an entrepreneur. You allocate constrained resources to generate the highest return, best-risk adjusted return, smallest loss…whatever your objective is.

Games have mine a variety of mechanics (awesome list here) just as there are many types of business models. Both game mechanics and business models ebb and flow in popularity. With games, it’s often just chasing the fashion of a recent hit that has captivated the nerds. With businesses, the popularity of models will oscillate (or be born) in the context of new technology or legal environments.

In both business and games, you are constructing mental accounting frameworks to understand how a dollar or point flows through the system. On the surface, Monopoly is about real estate, but un-skinned it’s a dice game with expected values that derive from probabilities of landing on certain spaces times the payoffs associated with the spaces. The highest value properties in this accounting system are the orange properties (ie Tennessee Ave) and red properties (ie Kentucky). Why? Because the jail space is a sink in an “attractor landscape” while the rents are high enough to kneecap opponents. Throw in cards like “advance to nearest utility”, “advance to St. Charles Place”, and “Illinois Ave” and the chance to land on those spaces over the course of a game more than offsets the Boardwalk haymaker even with the Boardwalk card in the deck.

In deck-building games like Dominion, you are reducing the problem to “create a high-velocity deck of synergistic combos”. Until you recognize this, the opponent who burns their single coin cards looks like a kamikaze pilot. But as the game progresses, the compounding effects of the short, efficient deck creates runaway value. You will give up before the game is over, eager to start again with X-ray vision to see through the theme and into the underlying greeks.

It would be a shame to approach financial theory narrowly because it’s both a useful and satisfying lens. It’s not for me to say where it bleeds from the instrumental to the appreciative but I will break the implications down as I see them.

“No risk no premium” does not imply the converse — that risk will earn you a premium. There are strong reasons to believe idiosyncratic risk will not earn you a proportional return.

Why?

Markets are evolutionary systems. There are invisible forces that stimulate survivors to adapt. Those adaptations are unrelenting pressures that push markets closer to theory. You might even think of efficiency as the removal of frictions (and sources of edge) such as opacity or communication costs. As these are removed, the system approaches a theoretical vacuum. It looks more like theory.

The theory of markets is deeper and more fundamental than object-level strategies. In fact, the meta-idea of a “strategy getting priced in” is an example of a deeper-level market phenomenon.

Adaptations that survivors internalize become part of the native intelligence of “risk absorption”. The efficient transfer of risk absorption amongst the willing and able is the very function markets and must be considered by any challengers.

Some of the deepest roots of that distributed intelligence are captured in these ideas:

The largest bankroll is able to absorb the most variance. This in turn allows them to be the best bid.

if they both yield 5%, being risk neutral means being indifferent between them. You might ask why would I be indifferent, one is a steady stream? Well, you might not be indifferent but if the prices got out of line, someone else would buy a basket of coins (they are uncorrelated) and short the govt bond and that would push the prices to parity (minus arbitrage costs such as financing/hassle hurdle

The portfolio that has the most to gain from diversification can afford to be the best bid.

In fact this is so well understood that you end up with the classic M&A perversion of companies “overpaying for synergies”. Despite this overcorrection, you should certainly wonder you can afford to match the bid of a buyer who derives strategic/diversifying value from the asset in your sights.