We want to estimate the straddle. The mean of the underlying stock distribution is centered around the forward price not the at-the-money price.

We will estimate the at-the-forward (ATF) straddle.

This means we are estimating the straddle struck at the ATF strike.

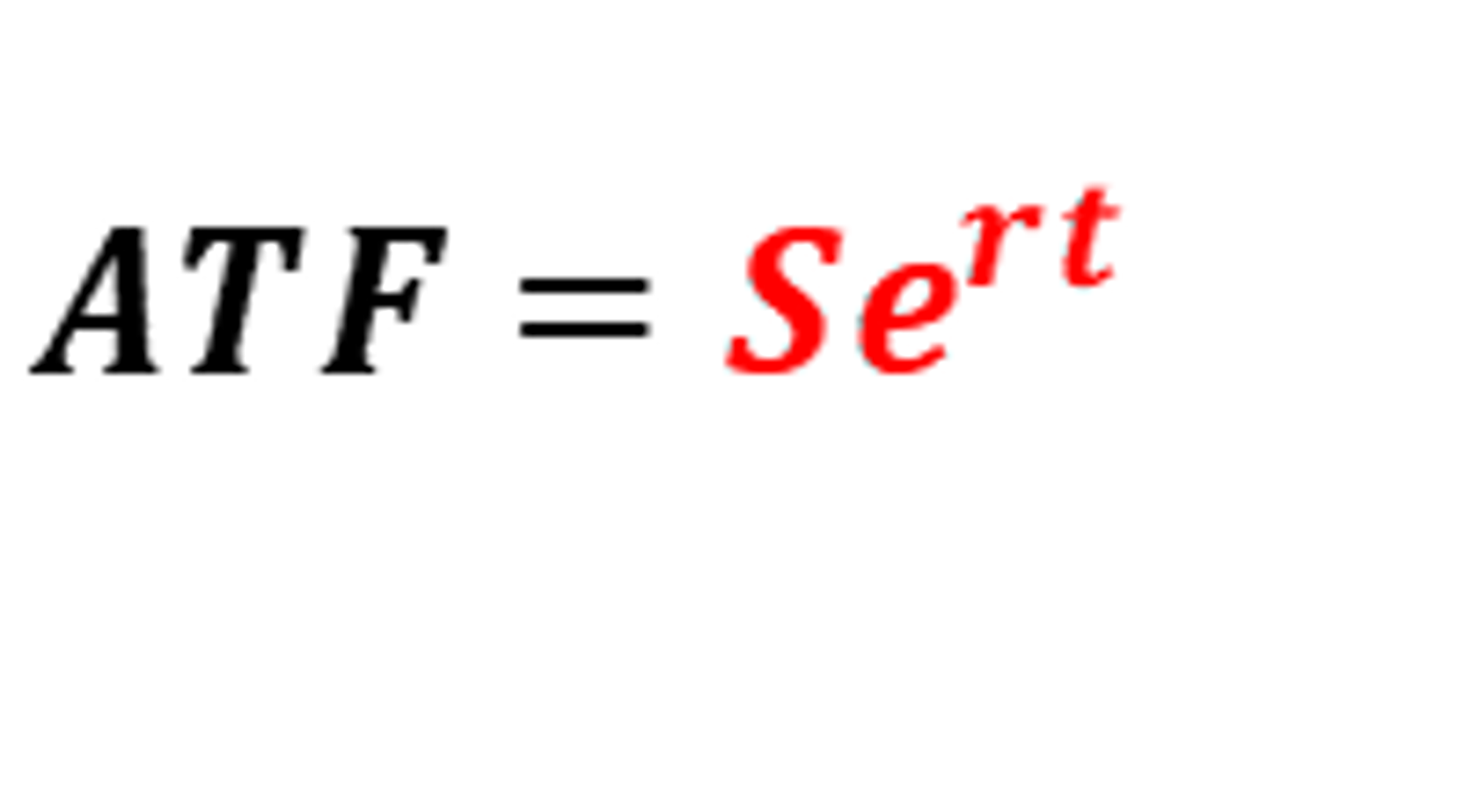

The ATF strike occurs at the ATF price:

Approximating the ATF call option

This is the meat of the work.

[It requires no more than pre-algebra. I know this because my 5th grader is taking the Art of Problem Solving online course in it now. I’m not proud to say I’m quite rusty.]

Let’s go.

While we want the straddle, let's start with the ATF call option.

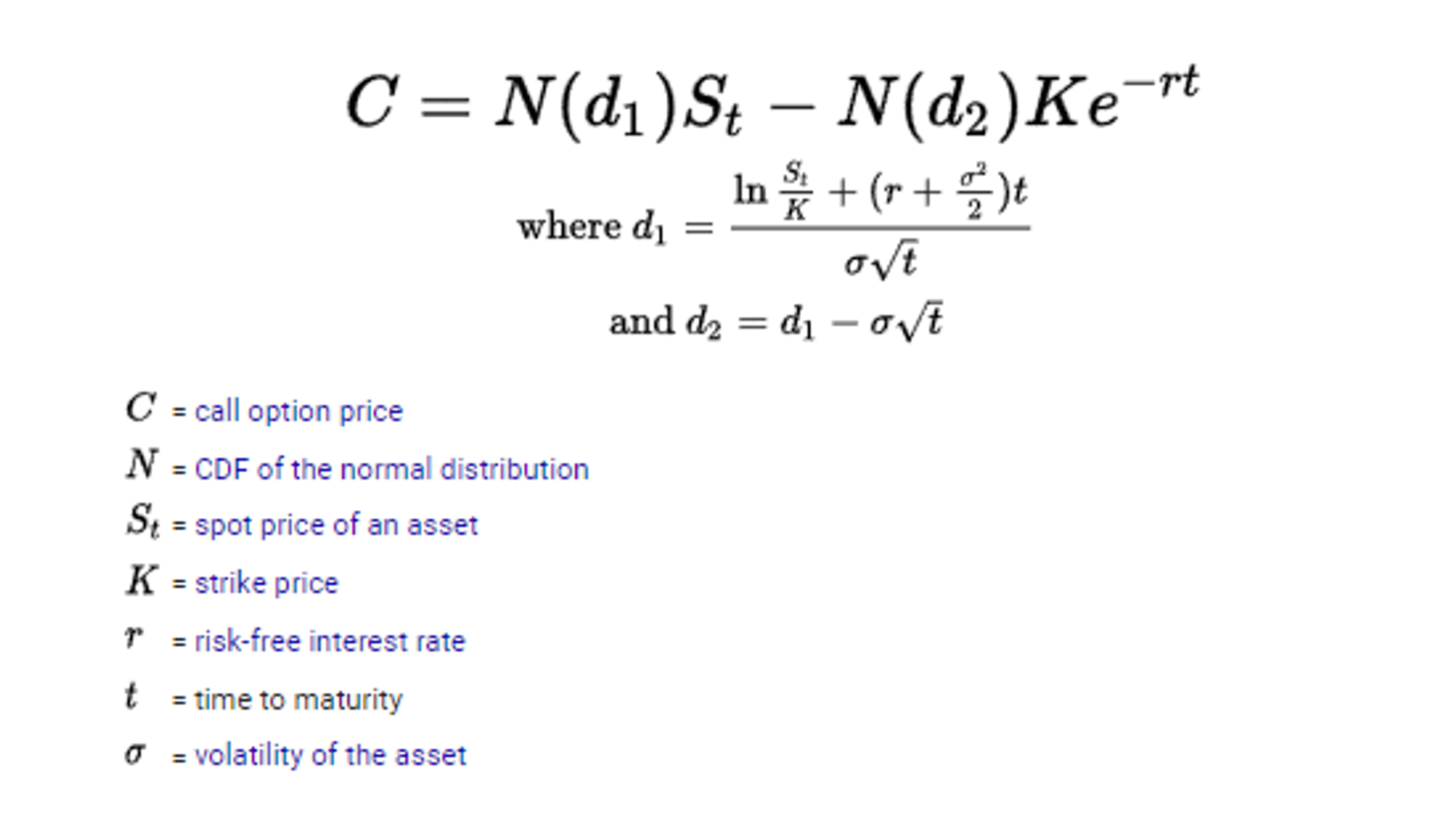

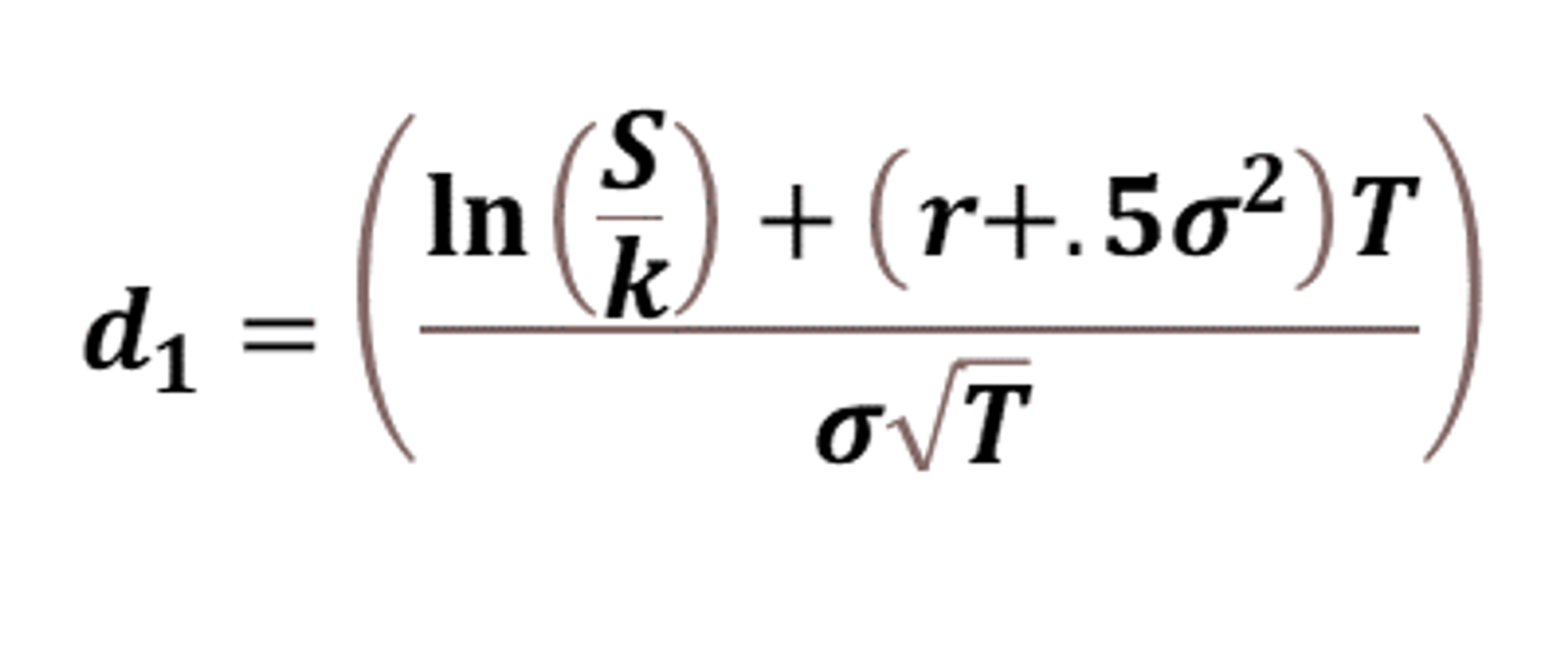

We invoke Black Scholes:

…specifically, we zoom in on d1:

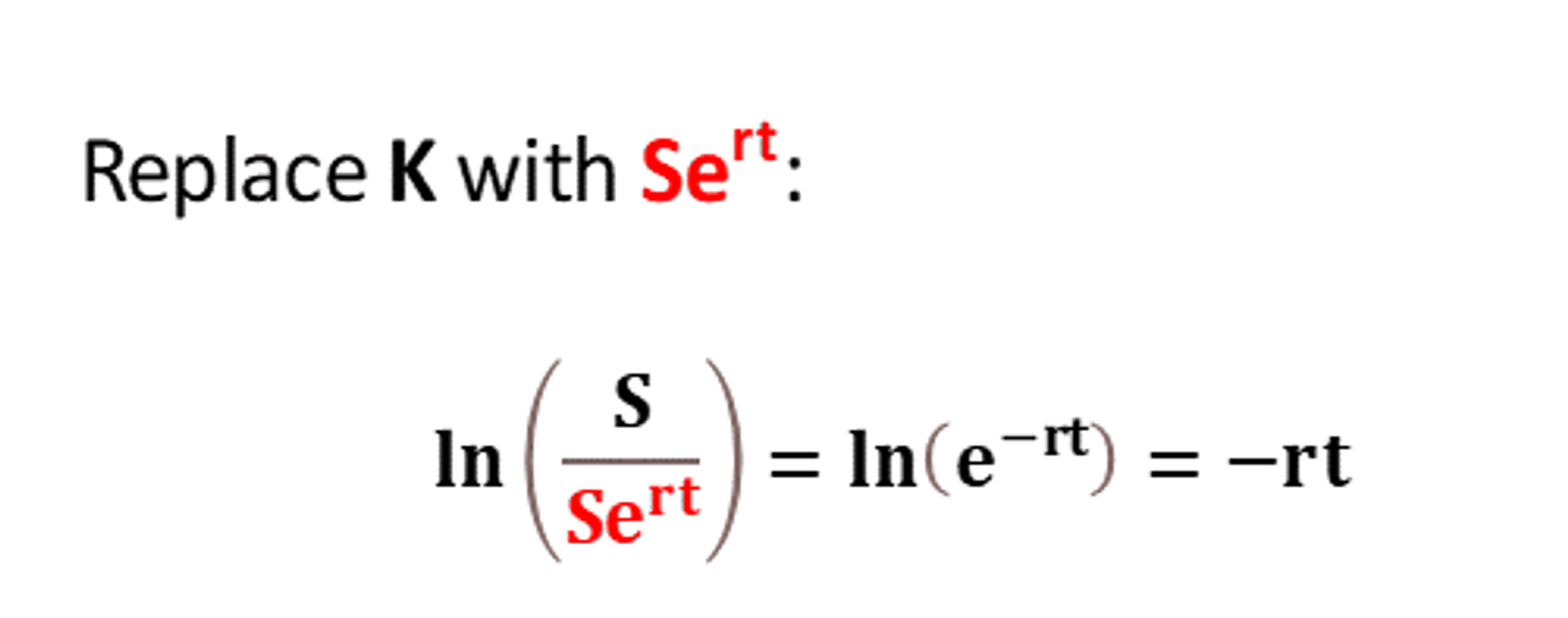

We are computing the call price for the strike K = ATF

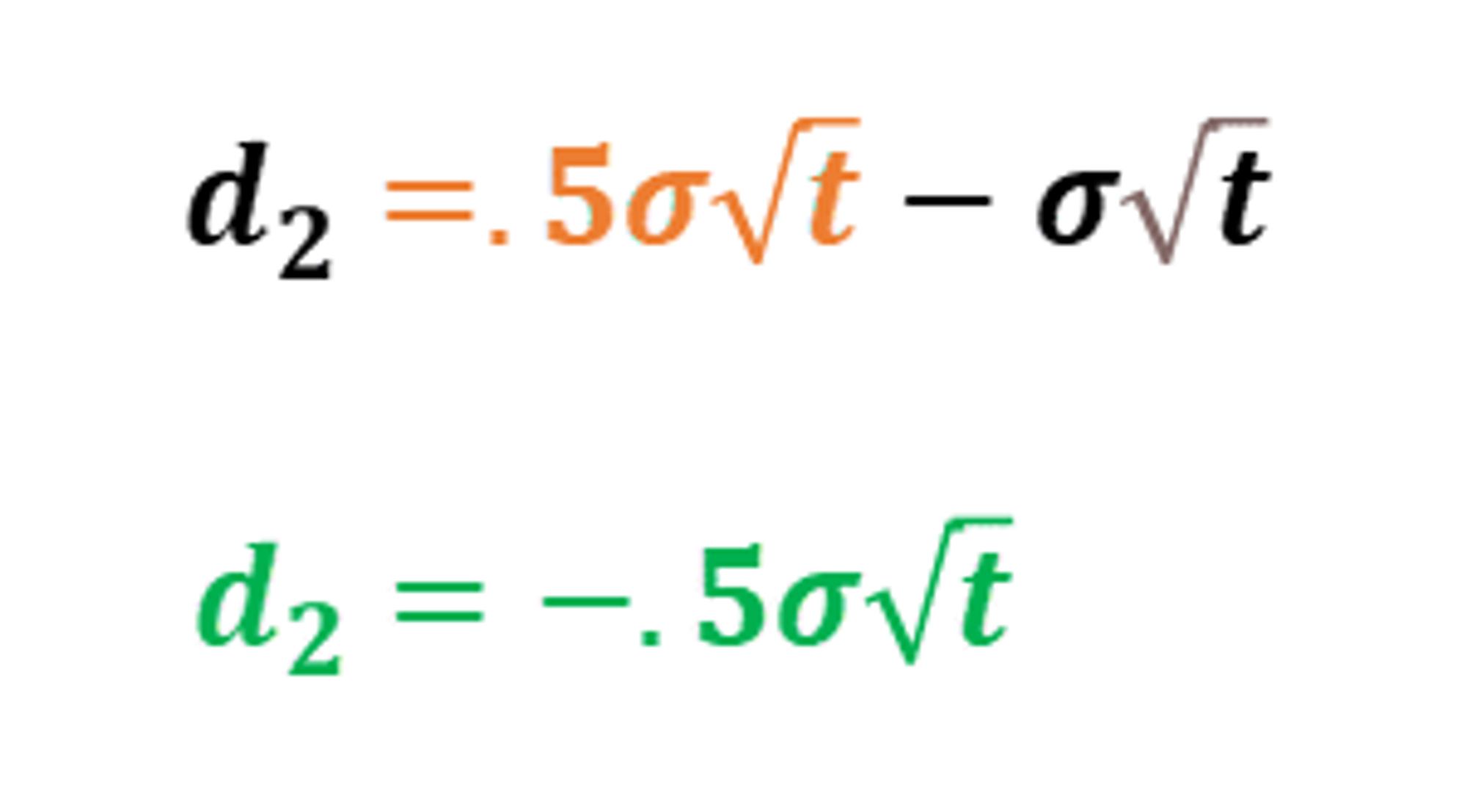

Plug back into d1:

Recall from the definition of B-S:

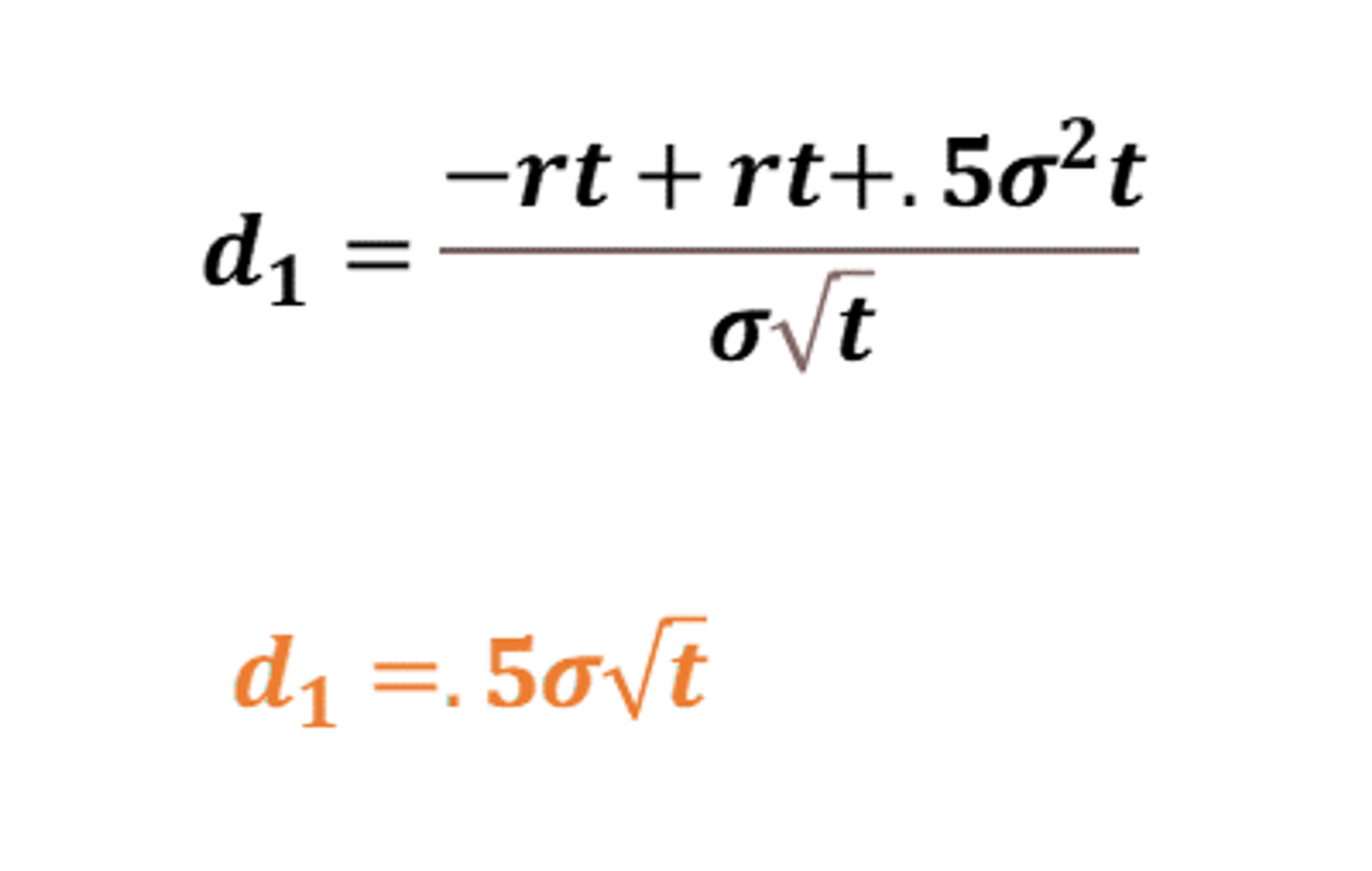

Plug and chug:

🏁

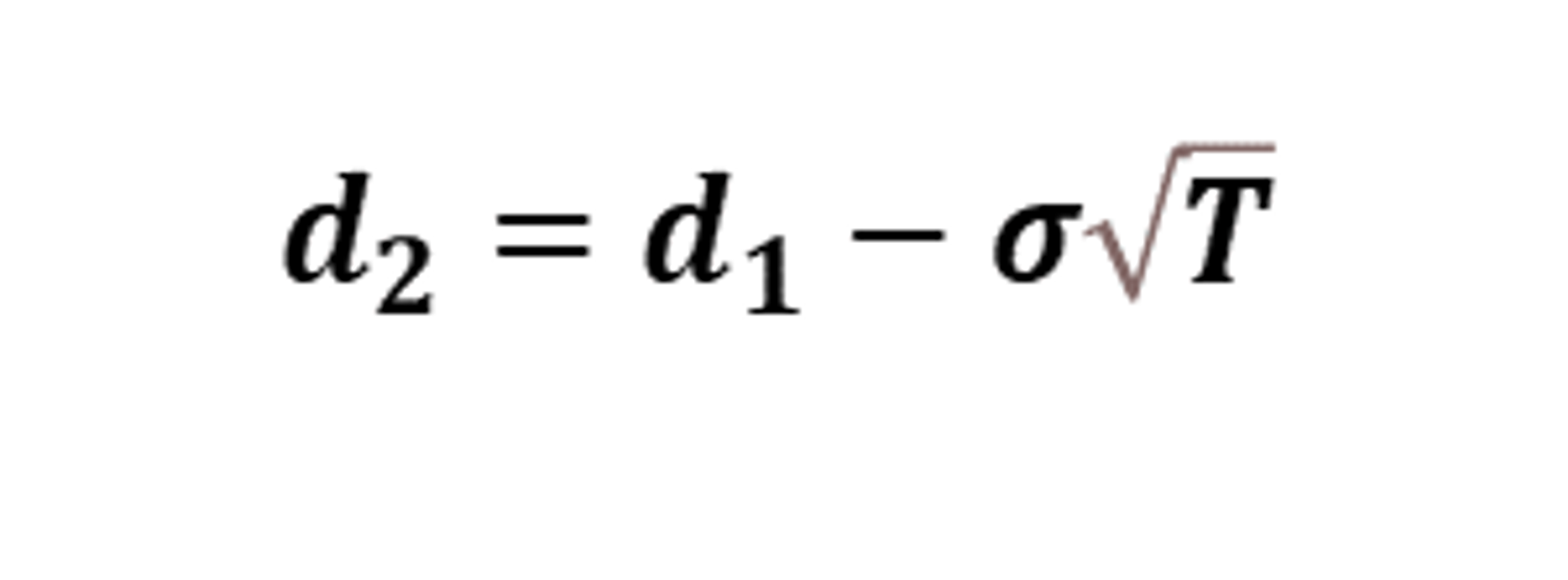

Checkpoint: We established 3 identities that occur at-the-forward

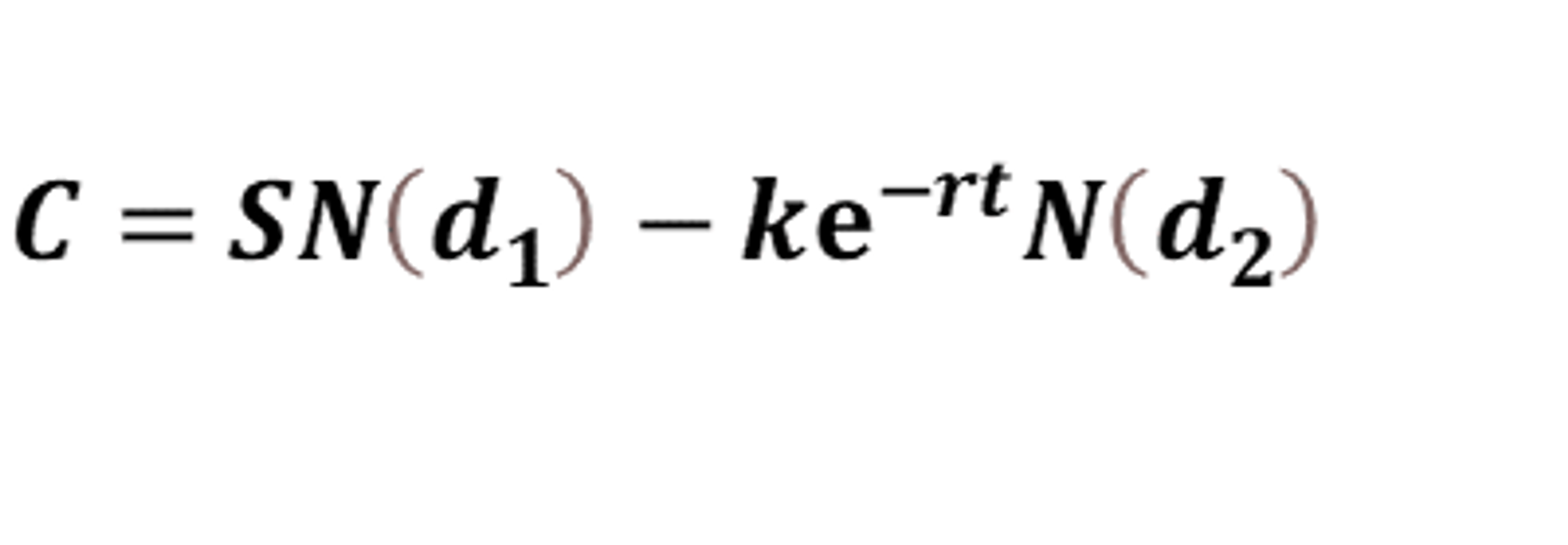

Let’s plug these identities back into the B-S equation for call struck ATF:

Hmm, this looks fairly docile. Stare at it hard. The next section will feel good.

Visualizing the call option

We established this so far:

The underlying distributions for B-S is that stock prices are lognormal. The prices are lognromal but logreturns are normally distributed.

This is handy because normal distributions are familiar to work with.

d1 and d2 are like Z-scores on a Gaussian (bell) curve of logreturns!

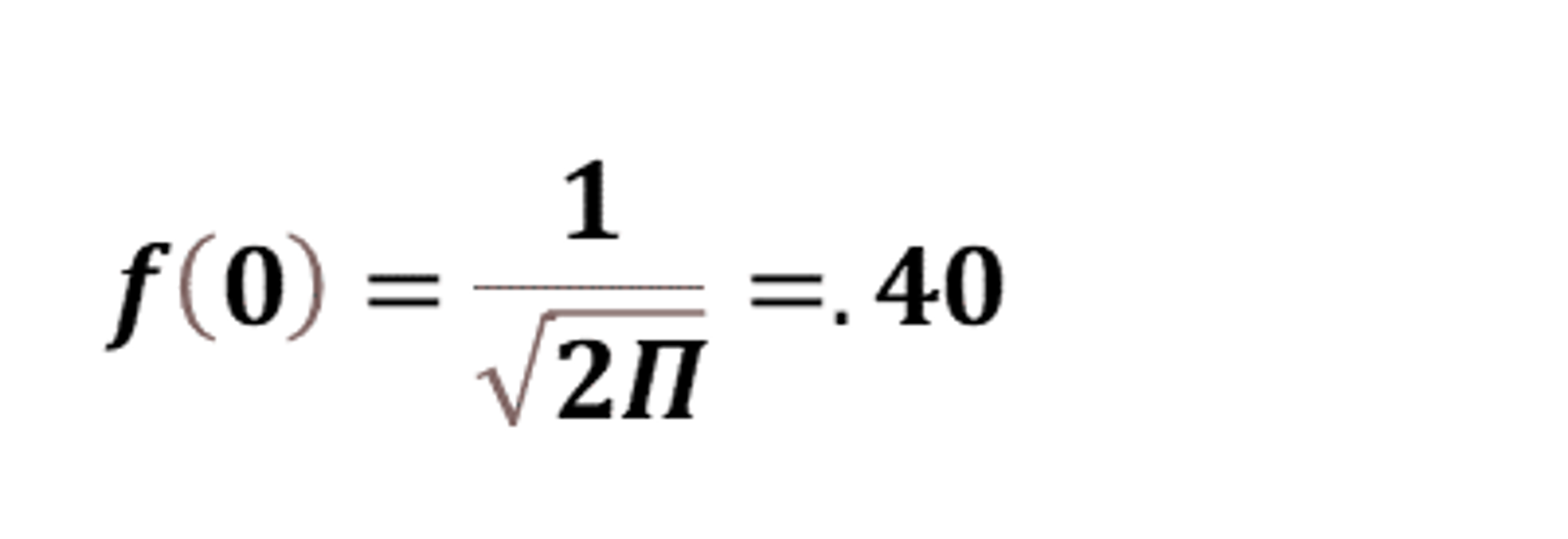

The probability density function (PDF) for a bell curve:

The center of our distribution is an expected logreturn of 0 corresponding to the forward Seʳᵗ

The peak of a bell-curve at that forward price corresponding to a logreturn of 0. For the standard normal curve we can assume σ = 1

Plug 0 into x of the PDF:

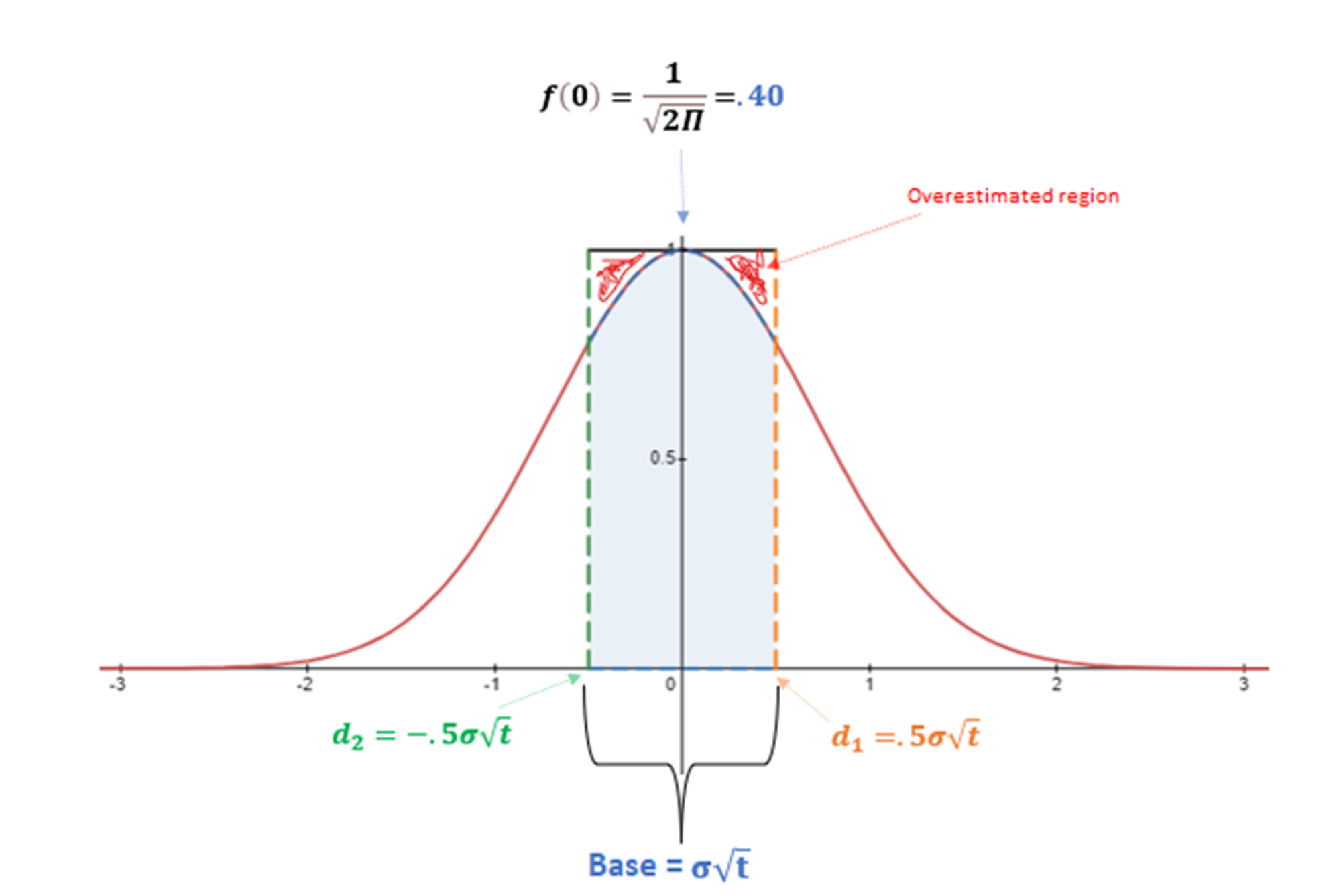

Let’s bring this all together into a picture:

Understanding the picture

The value of the ATF call is the integral of the PDF between d1 and d2 but we can estimate it!

height x base x forward price

Note: This will slightly overestimate the value of the call (see overestimated region in the picture)

From call price to the straddle

The call estimate is:

For the at-the-forward strike the call and put are equal because of put-call parity!