You could expect the ratio to differ for non-Gaussian distributions. When examining data, computing both statistics can give you a clue about its nature.

In the text example above, the MAD/SD ratio of only 27% is a clue:

Even though the MAD is more useful than SD for telling us what outcomes are typical, the ratio indicates that there are some highly skewed outliers.

Look at the key takeaways thus far. What do you see?

The mean absolute deviation is .80 of the standard deviation and the straddle is .80 of the volatility.

The straddle is the MAD!

The volatility, which is computed just like a standard deviation, gives large moves extra weight. But the straddle is a better reflection of what move size we typically see.

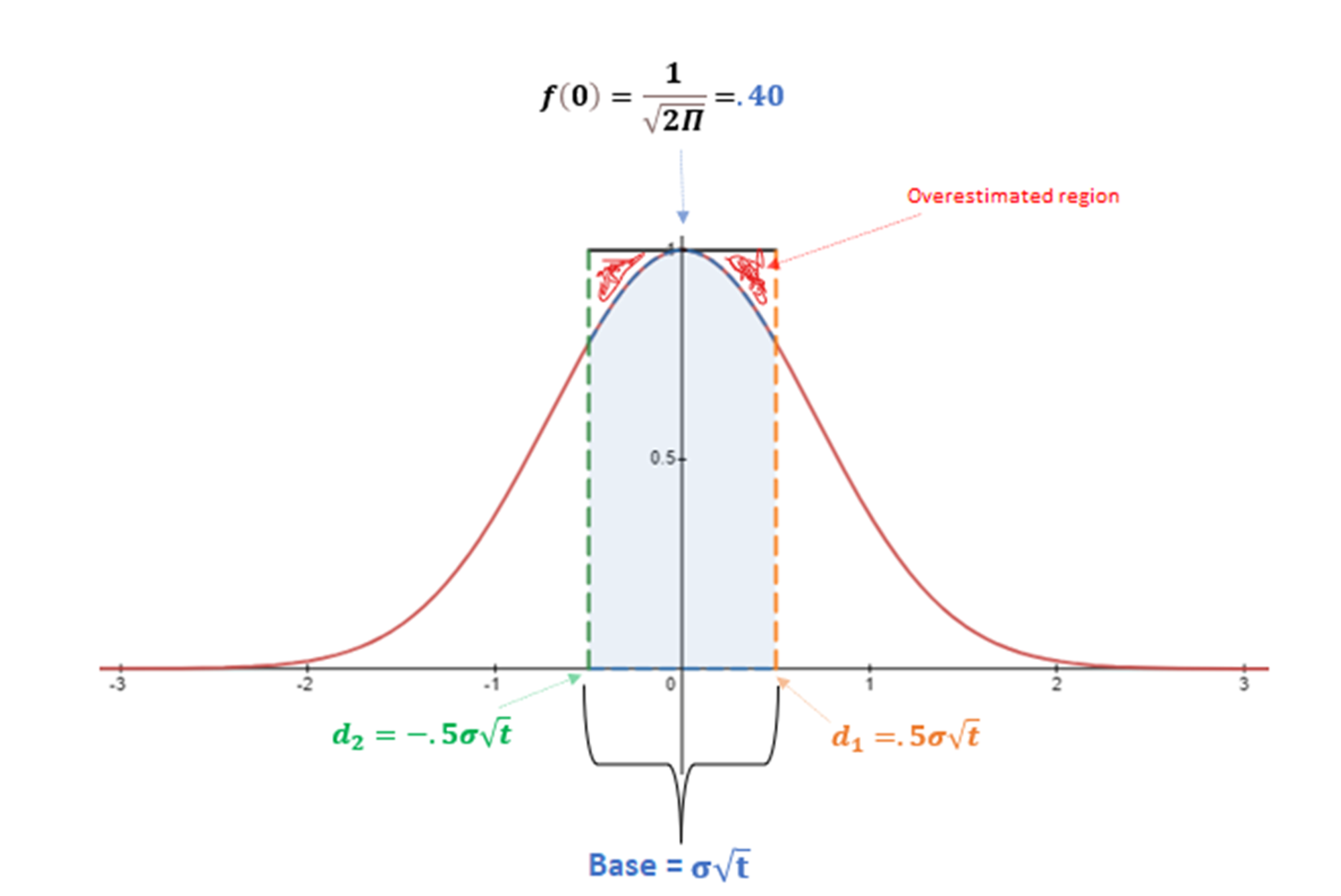

It will cost you .80 of the standard deviation to buy a fairly priced straddle. Let’s plug that into a normal curve’s cumulative distribution function:

despite the low “hit rate”, it’s fairly priced because the payoff on larger moves balances the expectancy

Part III: Distortions

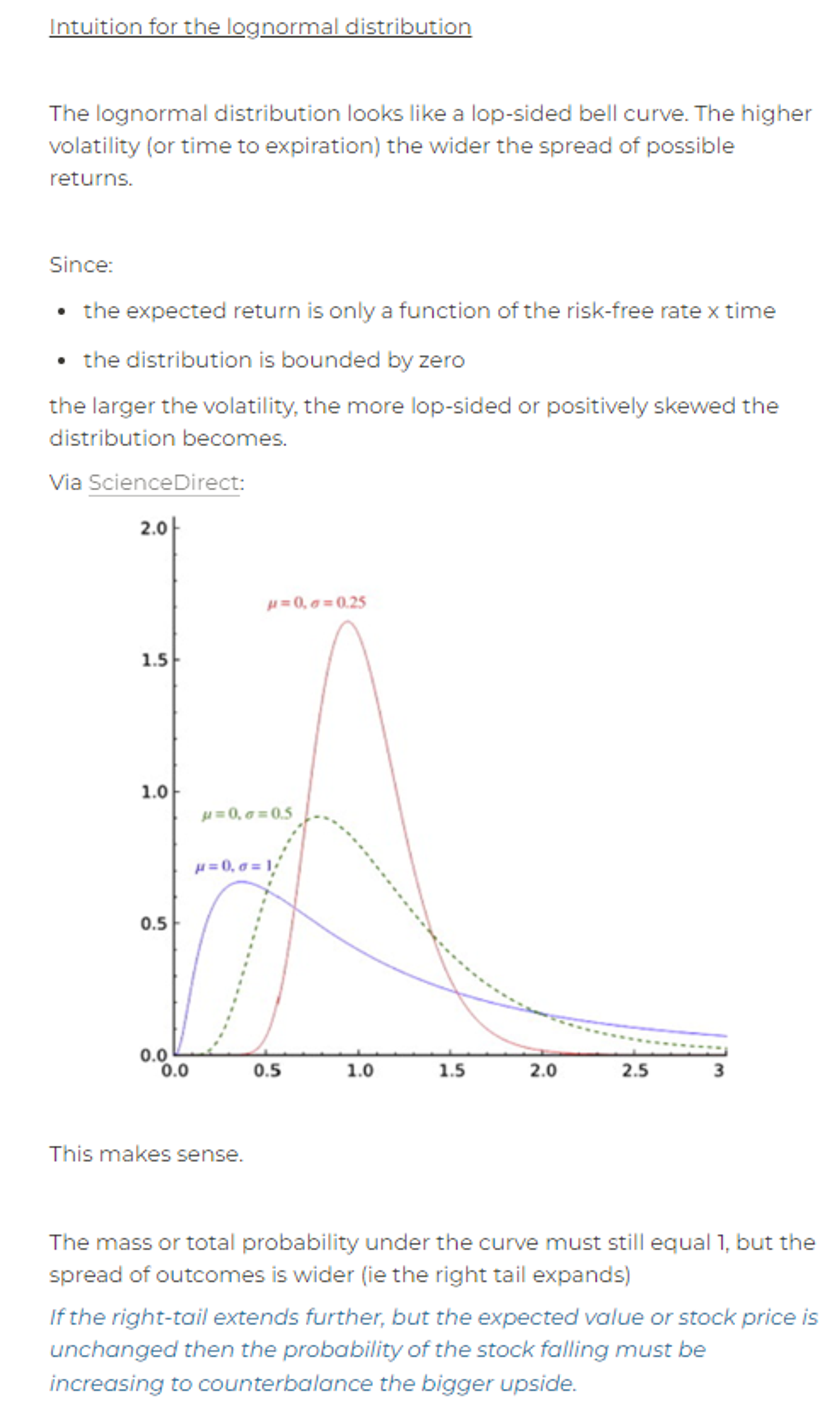

We saw earlier that the MAD can be higher or lower than .80 of a standard deviation if the distribution is a symmetrical bell curve. B-S assumes a lognormal distribution of prices and therefore normally distributed log or “compounded” returns.

Empirically we know that asset return distributions vary. Power law, bimodal, fat-tailed, and skewed distributions are regular enough to not be considered exceptions. Implied option skew is a fudge to accommodate reality. Volatility itself is not constant and varies with spot prices. These are deep topics warranting reams of academic and practitioner research.

However, we can tinker with simple examples to bootstrap intuition about the relationship between volatilities, option prices, and distributions.

Let’s examine a couple of distortions to see what we can learn.

In the straddle approximation, we raised the volatility making the distribution more positively skewed. A small chance of big upside buoys the value of a stock that is most likely going to zero.

A visual of how raising volatility increases the positive skew of the lognormal distribution

By studying how the straddle approximation behaves we found:

The higher the volatility, the smaller the ratio of straddle to volatility. In other words, the MAD/SD ratio shrinks.

In the skewed coin stock examples, we introduced negative skew while lowering the volatility.

Again, the more skewed the distribution the lowered the straddle/volatility ratio.

In the presence of skew, the price of a straddle (ie the MAD) becomes less representative of the risk as the typical outcomes diverge from the volatility.

Rental properties feel like strongly skewed investments. This means their observed volatility understates risk.

Properties that sit vacant. Delinquent tenants or even tenants that turn into squatters. These don’t feel like typical volatility events but skew events.

You might model 1-2 months vacant out of every 24 months (90-95% occupancy) but those events likely cluster. So things are really going great more like 98% of the time, but when they go bad it’s a parade of money and effort to recover.

It makes sense to keep a reserve if you know this especially since RE is usually a leveraged investment. In other words, the typical or MAD results shouldn’t lull you into underestimating the full distribution of possible outcomes. The risk is in the tail not the meat.

[I’m not a RE investor but this is my impression and I’m just mapping it to the principles in this lesson. Feel free to share your thoughts]

Trading and Options

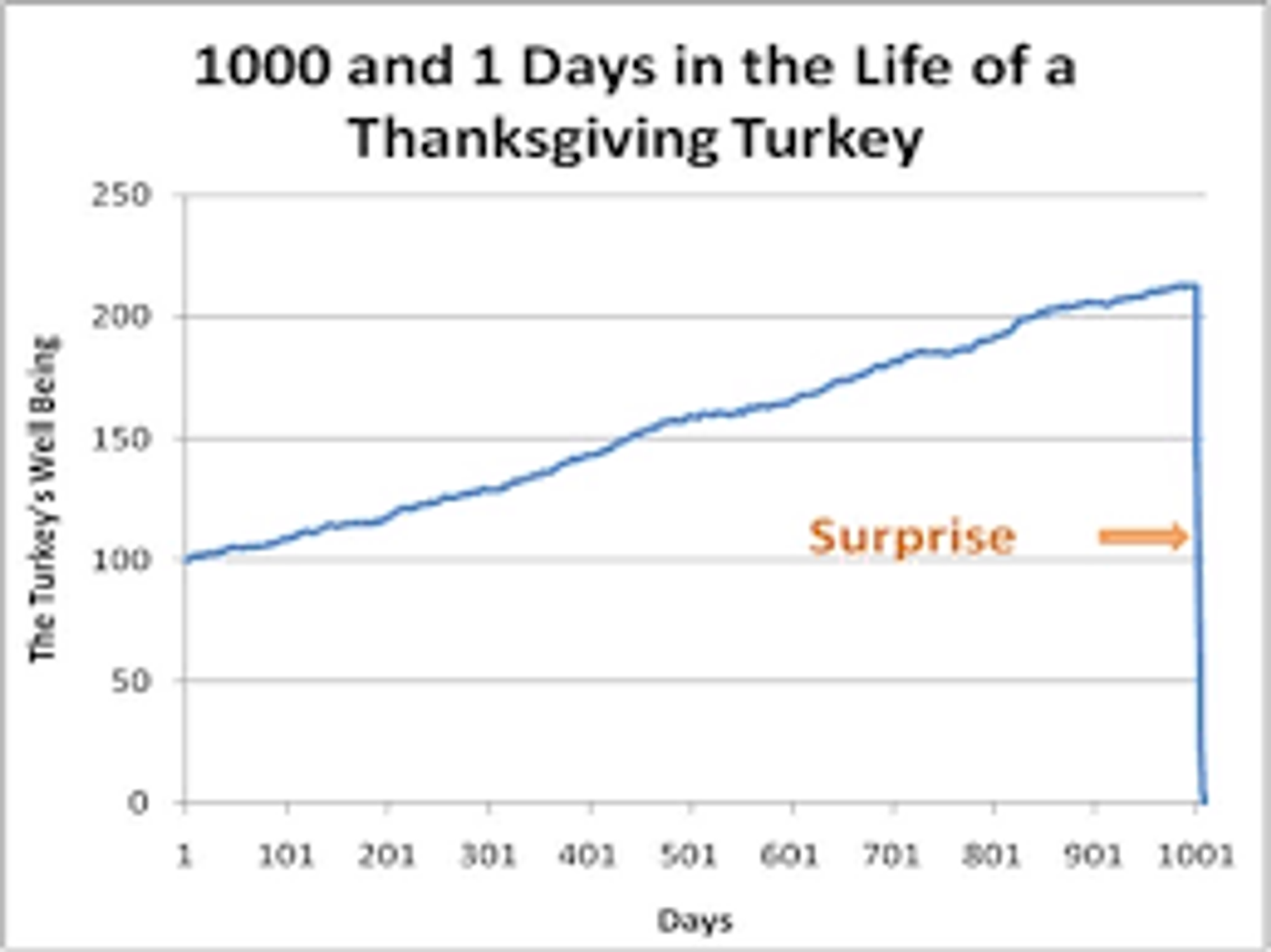

Skew hides. It is easy to focus on MAD and discount the full distribution. I always use the video poker analogy. Imagine finding a video poker machine that didn’t show its payoff table. Under the hood, it gives slightly worse payoffs on a pair of “Jacks or Better”, but offered a billion to one on the Royal Flush. You could play that machine for days or even weeks and never realize you had massively positive EV. The contribution to the overall expectancy of the game comes from a very rare outcome.

It’s the familiar Turkey problem that Taleb popularized:

💊

Tips

Don’t let your risk management simply rely on volatility-based measures.

Shock your book with absolutes that are independent of vol level.

How much do I lose if the stock goes bankrupt?

What if correlations invert?

What if stock and vol are both shocked upwards?

Use the option surface to tell you about skew and kurtosis (fat-tailedness).

Straddles tell you a lot more than just a flat stock price. But the whole surface contains yet even more information. I find this to be an underappreciated observation. Mostly by people who think they know more than markets.

In my own experience, I’d often get an idea that the skew should look a particular way in light of a recent event only to find the surface already shifted to how I’d expect.

One particularly frustrating example of this was the silver market in early 2021 when the WSB crowd aped into upside calls. Silver was up over 10% in about 2 trading days and I wanted to buy put spreads on a retracement knowing the apes were barking up the wrong tree. The problem was you could only get even money odds on 10% pullback. I wouldn’t expect to get typical odds after such a rip, but only even money? Come on.

Every single structure was pointing to silver going back to where it came and in fact, you could get odds for expecting silver to just settle down at this new price level or even going higher. In other words, the market was thinking just like me. And it turned out to be right.

My experience is commodity options market are annoyingly smart.

See: What The Widowmaker Can Teach Us About Trade Prospecting And Fool’s GoldTalk about a market where “the skew knows”

Examine the shape of the data for both offense and defense

Compute realized standard deviations and MAD. It's a quick check on whether typical observations are representative of the risk.

This would be a common first step if I was looking at a new market.

Like “how do future spreads behave”?

Based on some examination of realized behavior, ask yourself “Without looking at option screens how would I expect them to be priced?”

If the option surface doesn't conform to my expectations, “What am I missing?”

If I don't think I'm missing anything what kinds of structures exploit that surface?

ExampleIf the MAD/SD ratio <.80 there are either fat tails or a skewed underlying distribution. This could be a candidate for selling iron flys.

You want to be short the straddle and long the wings if the market is not pumping enough vol points into those OTM options. You may even want to put such a trade on vega neutral (this position is long vol of vol or “vol convexity”) by overweighting the wings.

More food for thought

I’ll throw the lob, but I won’t finish:

If a distribution has fat tails and a high peak and the term structure is flat, what position do you want (assuming no known events upcoming)?

Is there a relationship between between skew and term structure?

[These make for good interview questions btw]

Concluding remarks

In the presence of strong skew:

the MAD/SD or Straddle/Volatility ratio collapses. The straddle will understate the true risk.

Be careful using the 1.25x rule to turn the straddle into a volatility. If the straddle understates the risk, you need a larger ratio!

Deltas and therefore hedge ratios in the direction of the skew will be understated

A market that prices volatility according to what moves are typical, but you suspect the skew is hidden, will suppress straddle prices and, in turn, volatilities. Be careful in using volatility-based sizing when you have reason to believe the asset’s true return distribution is strongly skewed.

While these remarks have all been defensive-minded, you can use these principles to go on offense. Where is skew over or underappreciated and how should that affect pricing?

If you use options to hedge or invest, check out themoontower.ai option trading analytics platform