Straddles are one of the most common option positions. A long straddle consists of being long both a call and put on the same strike in the same expiration. You are hoping the stock moves somewhere far away from the strike.

The value of a straddle, being composed of options, is determined by the level of volatility.

Volatility is simply the standard deviation of returns.

The value of a straddle:

is determined by the level of volatility

inverting — it can also be used to imply the level of volatility

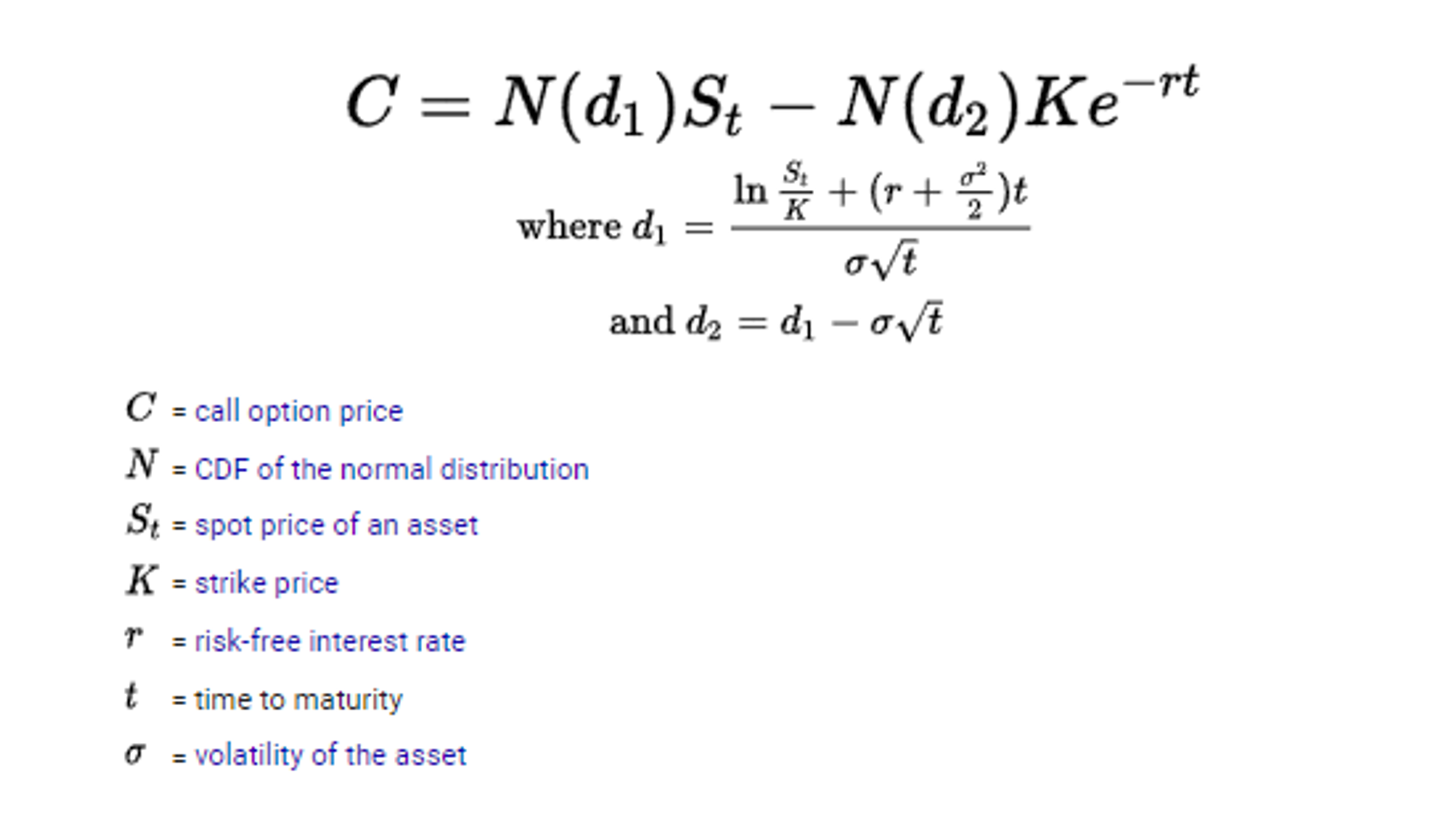

If compound returns for a stock conform to a normal distribution and we have a reasonable estimate of the volatility we can use Black-Scholes to compute option prices and of course straddles.

This is the Black-Scholes formula for a European-style option assuming no dividends:

Gross.

You know what’s more fun? Shortcuts.

You can get a very close approximation for a straddle price with the following formula:

🖖🏾

ATF Straddle Approximation

where:

S = forward price

σ = annualized volatility

t = fraction of a year until expiry

👀

I think you’ll find this visual derivation of this approximation highly satisfying